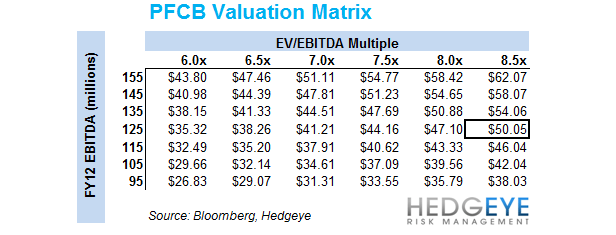

Looking at the past two transactions in the restaurant space, the implied range for the PFCB is $38-$50. We are not saying that PFCB is going to get bought any time soon, nor are we saying that the stock is set to trade to $50, but applying the 8.7x EV/EBITDA multiple FNF paid for O’Charley’s implies a price of $50 for P.F. Chang’s.

This biggest issue facing PFCB coming into the 2/16 earnings release on is guidance for 2012. While we hold a positive view of the direction the company is being taken by management, there are difficulties ahead that may bring guidance lower for 2012.

In our view, we are likely seeing a bottoming process in PFCB earnings. The timing or duration of this bottoming process largely depends on where guidance comes in. However, even if management does guide down and EBITDA goes to $115 million from the current expected $125 million, the valuation range based on recent restaurant transactions is $35-46. PFCB’s current EV/EBITDA NTM multiple is 6.4x having bounced from as low as 5x in 4Q11. With the stock trading at $34, we do not see significant downside in this name, even in the event of a guide down.

If we wanted to recommend a stock that goes sideways, we would save ourselves the work and just direct you to WEN. For upside to PFCB, management has to build credibility with the investment community that is has a plan to fix the business and expand the multiple further. Part of that creditability will come from having a strategic direction that will help arrest the decline in the operating performance of the company. Where we differ from most of the investment community as it relates to PFCB is that we believe management’s plan makes sense and that investors and analysts will get on board over the course of 2012.

This stock is being valued lower than Ruby Tuesdays at current multiples which, we can only assume, means that consensus believes management is not improving the business. As we wrote yesterday, we are buyers of PFCB on down days.

Howard Penney

Managing Director

Rory Green

Analyst