We continue to hold a positive view of YUM on all three durations (trade, trend and tail). The earnings call tomorrow at 9:15am will offer a chance for analysts and investors to hear further details about 2011 and trends in 2012 to-date.

With both MCD and SBUX seeing their stocks decline on 4Q11 earnings results that were strong but not strong enough, the pressure was on YUM to print an exceptional quarter and, on the surface, it looks like they delivered.

Yum! Brands’ stock had a tremendous 4thquarter, outperforming the S&P 500 by 8.3%. At first take, there does not seem to be many holes we can poke in the results such that we can say that the momentum is going to slow in the near term. The top-line momentum in YUM’s China division is strong although food and labor inflation continue to pressure margins.

We’ll be waiting for additional color from management tomorrow on the call. The US division might be turning as the compares get easier from here and the worst for Taco Bell appears to be over.

CHINA:

- The China division reported $5.56 billion in revenues in 2011, up 35% versus 2010

- System sales grew 40% year-over-year in the fourth quarter (33% excluding FX), while comparable restaurant sales came in at 21% versus 17% consensus

- By concept, KFC comps were 22% in the fourth quarter while Pizza Hut delivery and casual dining comps gained 25% and 15%, respectively, during the fourth quarter

- Restaurant margin decreased 240 basis points to 15.8% in 4Q11 due to 11% commodity inflation and 18% wage rate inflation. FY11 commodity inflation was 8% and labor inflation 20%

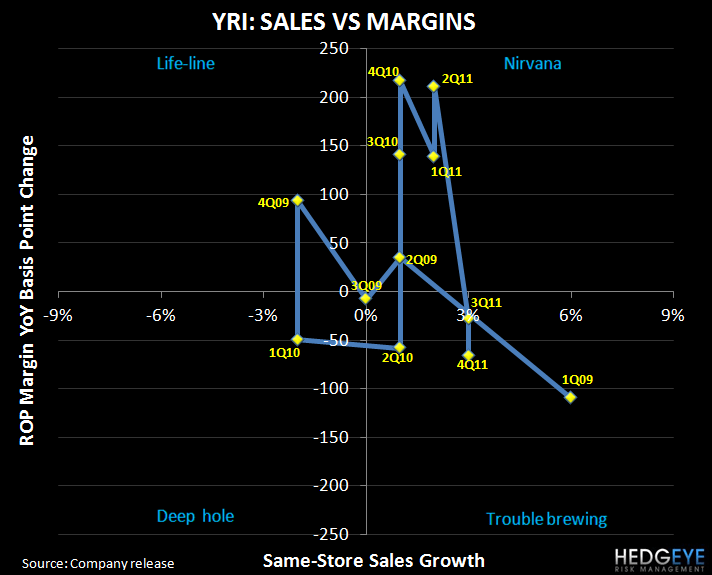

INTERNATIONAL

- YRI reported system-sales up 11% (up 10% excluding FX) with same-store sales of 3%, slightly above consensus

- Comparable restaurant sales of 3% implied two-year average trends flat with 3Q11

- Restaurant operating margin decreased by 67 basis points to 11.6% in 4Q11

UNITED STATES

- The most significant 4Q11 upside surprise came from the US division

- 4Q comparable restaurant sales were up 1% versus consensus of -2.5%. KFC comps decline -1%, Taco Bell comps declined -2% and Pizza Hut comps were up 6% versus 4Q10. “The Box” promotion drove high single-digit comps in the latter stages of 4Q11

- 4Q restaurant operating margin declined by roughly almost 75 basis points driven by commodity inflation of 7%

Howard Penney

Managing Director

Rory Green

Analyst