Conclusion: We have reversed course on gold and added a long position in the Virtual Portfolio. The key factors driving this shift are monetary policy and price movement in the long term Treasury market.

Position: Long Gold via the etf GLD.

James Bond: What do you know about gold, Moneypenny?

Miss Moneypenny: Oh, the only gold I know about is the kind you wear... you know, on the third finger of your left hand?

Similar to Miss Moneypenny, who has a strong affinity for all things gold in the well known James Bond film “Golden Finger”, we acquired gold in the Virtual Portfolio earlier today. This is definitely a shift from our previous research note that discussed gold on January 23rd in which both value and demand factors were driving our cautions outlook on gold, specifically we wrote:

“From a relative price perspective, we also took a look at the gold / copper ratio going back more than twenty years. Based on this ratio, and as the chart below shows, copper is near its cheapest level as priced in gold. Currently, one ounce of gold can buy 440 pounds of copper.”

And,

“It is also noteworthy to highlight that the world’s largest importer of gold is India, who is expected to import 54% less gold in Q4 2011 than in Q4 2010.”

So, what’s changed in the last three weeks? Well simply, monetary policy has become incrementally loose, inflation expectations have heightened, and, as noted in the chart directly below, gold is now in bullish price formation.

In terms of monetary policy, Chairman Bernanke and the FOMC were very explicit in the January 25thstatement:

“To support a stronger economic recovery and to help ensure that inflation, over time, is at levels consistent with the dual mandate, the Committee expects to maintain a highly accommodative stance for monetary policy. In particular, the Committee decided today to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through late 2014.”

Setting aside our amusement at the irony of the FOMC thinking they can predict economic conditions almost three years out when they have a proven track record of not being able to project out a couple of quarters, this verbiage, if taken at face value, does imply monetary policy will remain at Depression like levels until late 2014.

The key shift for us is that we had an expectation that the next move by the FOMC would be to become, even if on the margin, more hawkish. In fact, the opposite occurred and the FOMC extended their current “exceptionally low levels for federal funds rates” by a year from the prior statement on December 13th, 2011. This is inherently inflationary and, thus, a positive tailwind for gold.

In the chart below, we compare TIPS to Treasuries over the course of the past three weeks. This chart emphasizes that inflation expectations have increased in conjunction with the FOMC’s shift in monetary policy. Since January 17th, the TIP / IEF ratio has expanded almost consistently every day, signaling the market’s increasing view of inflation.

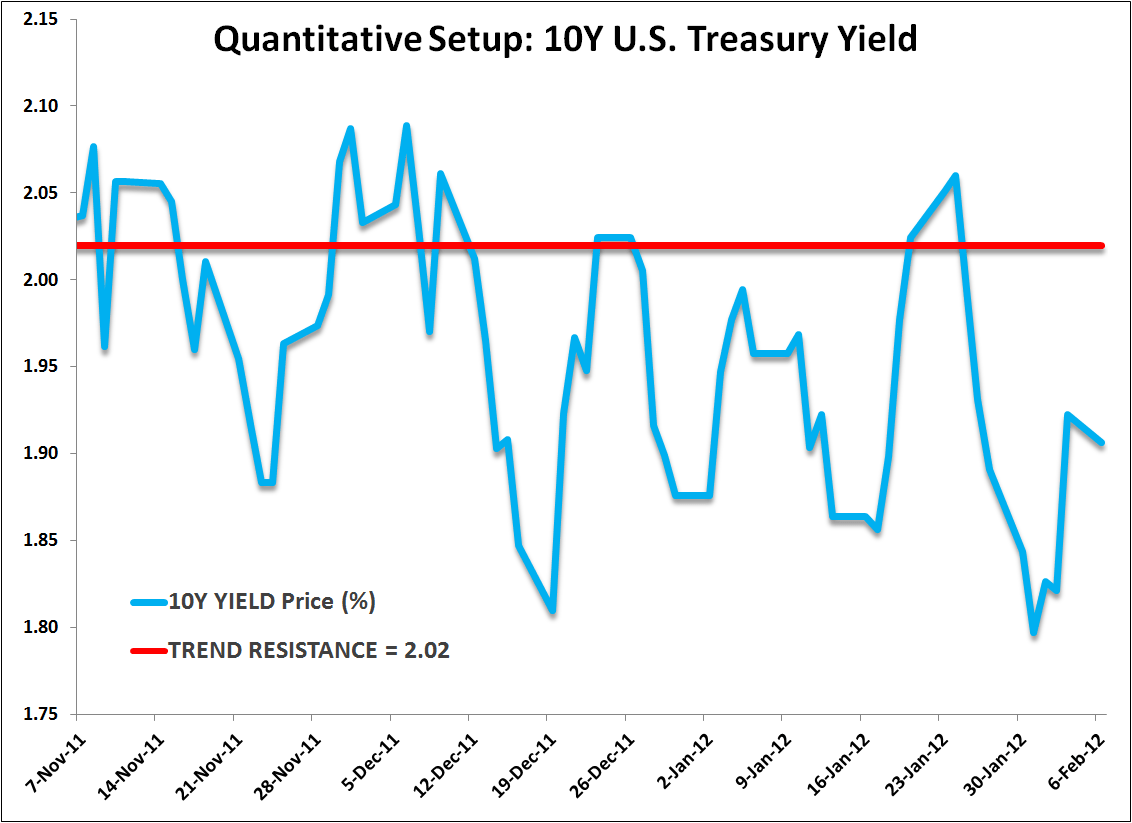

Coincident with this has been the bearish formation in long term treasury rates. As the chart below shows, the 10-year yield on Treasuries broke through the TREND line of resistance of 2.02% right about the time of the FOMC’s January 25th announcement and remains solidly broken. Obviously a declining yield on Treasuries is consistent with decline rates of return for fixed income.

Golden Finger is first and foremost a well known James Bond movie, but it is secondarily what Chairman Bernanke appears to be giving the nation’s saving class in providing them no return on their savings accounts or fixed income investments. When a savings account earns literally zero, gold is and will remain a reasonable alternative to capture absolute value.

Daryl G. Jones

Director of Research