*Interbank risk has been one of the most important gauges YTD for the outperformance in the big cap Financials. We've quantified what the improvement in Euribor/OIS means for each of the Moneycenter banks along with GS and MS. It's worth noting that Euribor/OIS ticked down again last week vs. the week prior, but it's also important to note that the amount of improvement was very small, falling less than one basis point. The TED Spread, however, showed sharp improvement week over week.

* Tightening Bank CDS in both American and European financials mirror what we're seeing in the equity market.

* All Downside from Here - In spite of the generally receding risk environment, our firm's Macro quantitative model indicates that in the short term there is 3.5% downside in the XLF vs. 0.0% upside. This is part of the reason we shorted PNC on Friday.

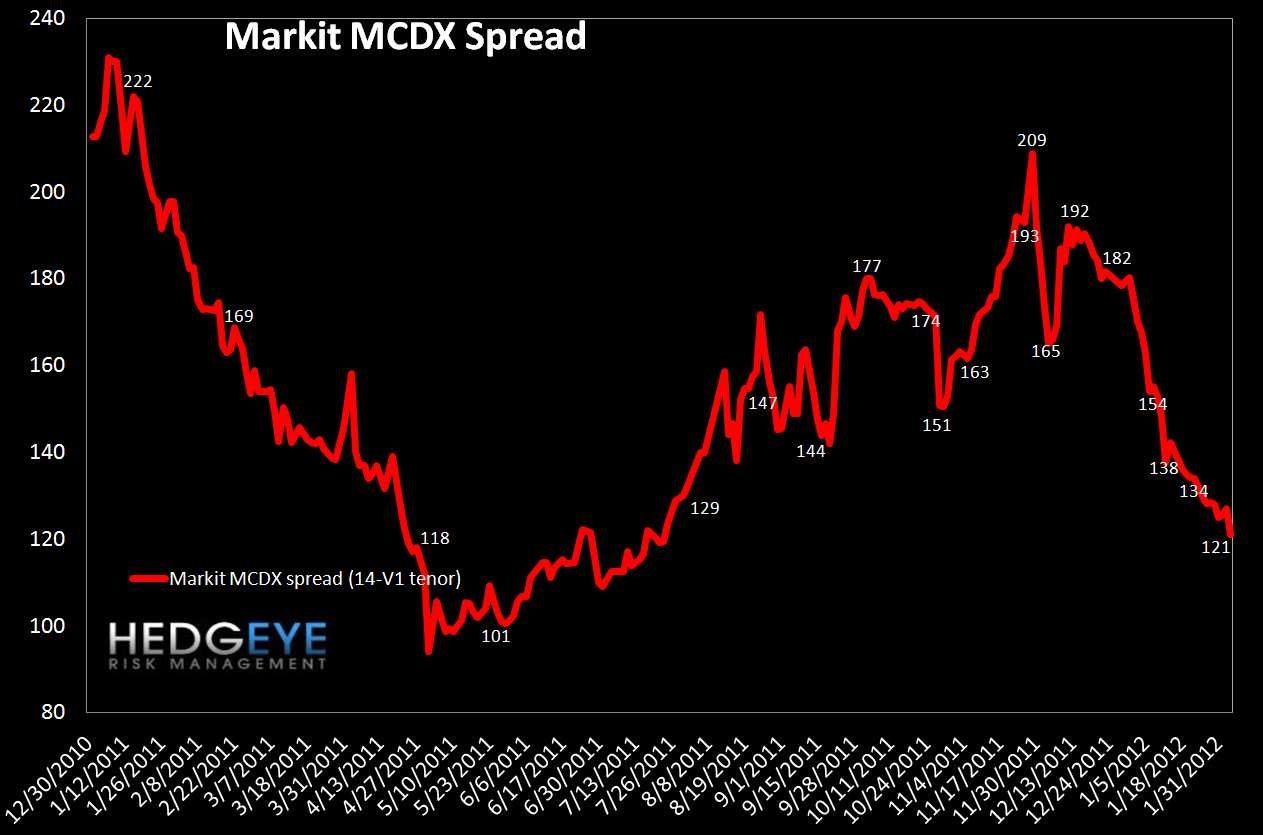

* The MCDX measure of municipal default risk continued to fall sharply week over week.

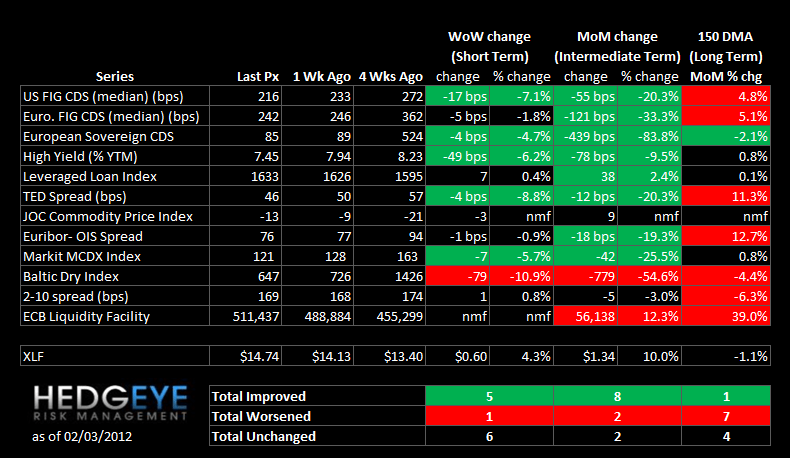

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 5 of 12 improved / 1 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Positive / 8 of 12 improved / 2 out of 12 worsened / 2 of 12 unchanged

• Long-term(WoW): Negative / 1 of 12 improved / 7 out of 12 worsened / 4 of 12 unchanged

1. US Financials CDS Monitor – Swaps tightened for 27 of 27 major domestic financial company reference entities last week.

Tightened the most WoW: GNW, AIG, XL

Tightened the least WoW: COF, AON, MBI

Tightened the most MoM: AIG, BAC, MS

Widened the most/ tightened the least MoM: MTG, CB, MMC

2. European Financials CDS Monitor – Bank swaps were tighter in Europe last week for 31 of the 40 reference entities. The median tightening was 1.8%.

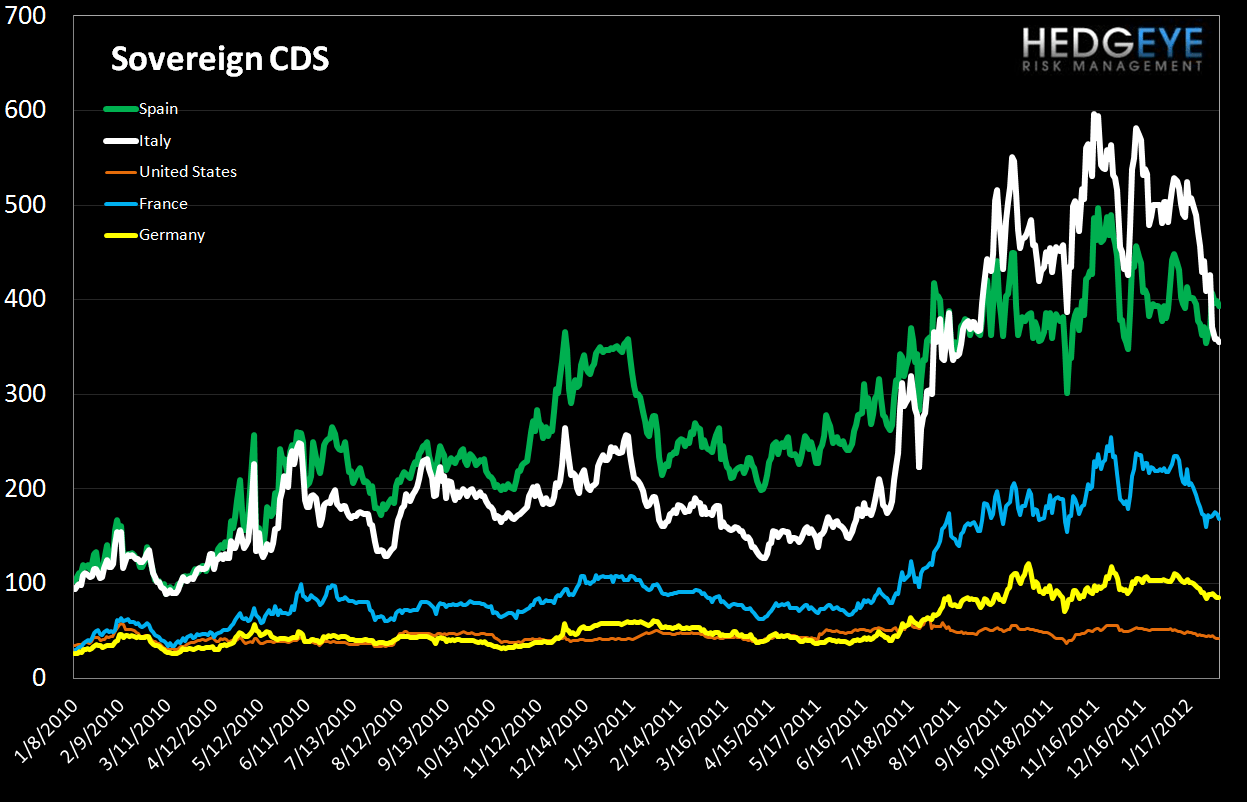

3. European Sovereign CDS – European Sovereign Swaps mostly tightened over last week. Italian sovereign swaps tightened by 17.0% (-73 bps to 354 ) and Spanish sovereign swaps widened by 5.8% (22 bps to 390).

4. High Yield (YTM) Monitor – High Yield rates fell 49 bps last week, ending the week at 7.45 versus 7.94 the prior week.

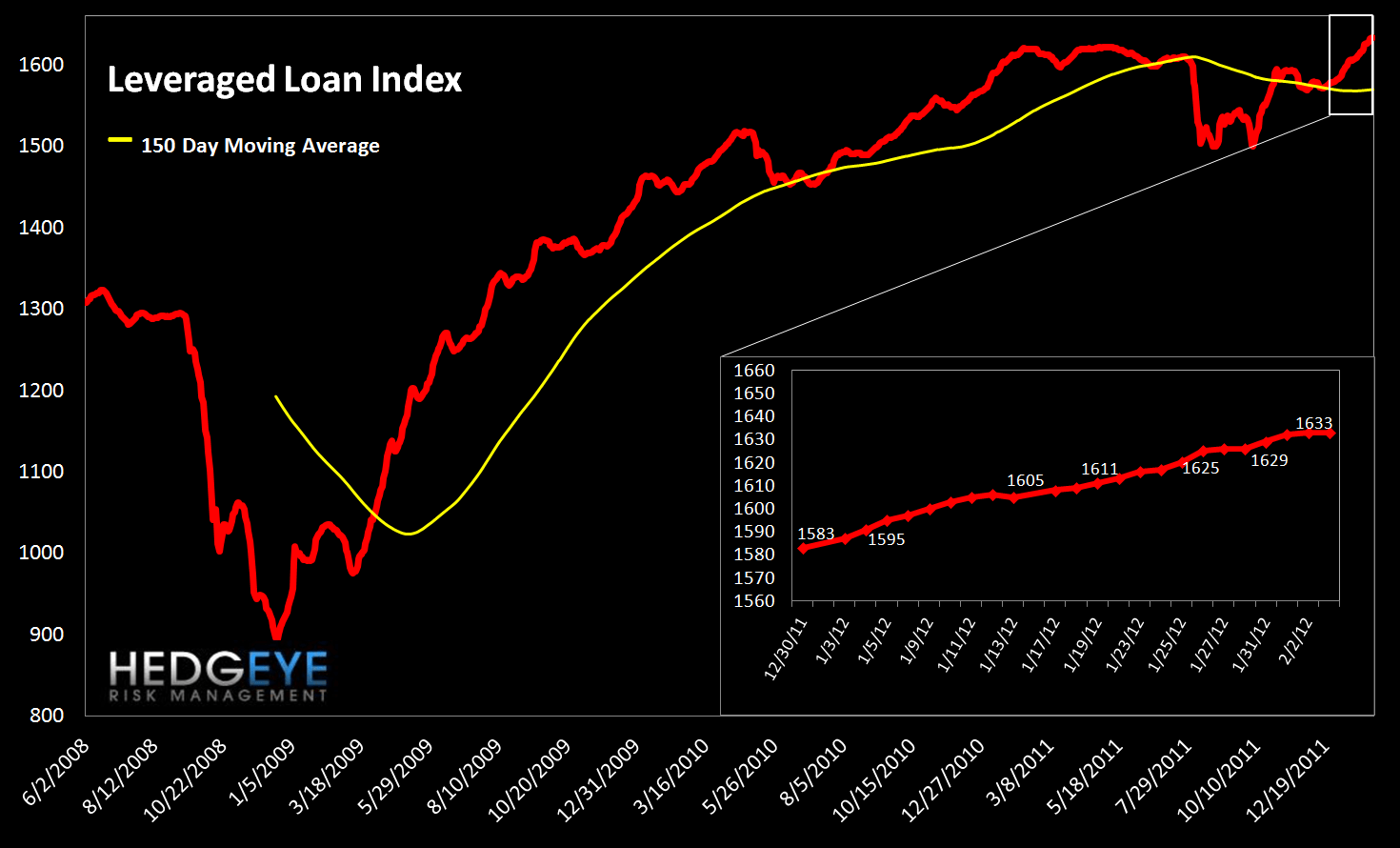

5. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 7 points last week, ending at 1633.

6. TED Spread Monitor – The TED spread fell 4 points last week, ending the week at 45.6 this week versus last week’s print of 50.

7. Journal of Commerce Commodity Price Index – The JOC index fell 3.1 points, ending the week at -12.5 versus -9.4 the prior week.

8. Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by less than 1 bps to 76 bps.

9. ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

10. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 14-V1. Last week spreads tightened, ending the week at 121 bps versus 128 bps the prior week.

11. Baltic Dry Index – The Baltic Dry Index measures international shipping rates of dry bulk cargo, mostly commodities used for industrial production. Higher demand for such goods, as manifested in higher shipping rates, indicates economic expansion. Last week the index fell 79 points, ending the week at 647 versus 726 the prior week.

12. 2-10 Spread – We track the 2-10 spread as an indicator of bank margin pressure. Last week the 2-10 spread widened to 169 bps, 1 bps wider than a week ago.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.0% upside to TRADE resistance and 3.5% downside to TRADE support.

NYSE Margin Debt - December

We publish NYSE Margin Debt every month when it’s released. NYSE Margin debt hit its post-2007 peak in April of 2011 at $320.7 billion. The chart below shows the S&P 500 overlaid against NYSE margin debt going back to 1997. In this chart both the S&P 500 and margin debt have been inflation adjusted (back to 1990 dollar levels), and we’re showing margin debt levels in standard deviations relative to the mean covering the period 1. While this may sound complicated, the message is really quite simple. First, when margin debt gets to 1.5 standard deviations or greater, as it did last April, that has historically been a signal of extreme risk in the equity market - the last two times it did this the equity market lost half its value in the ensuing period. We flagged this for the first time back in May 2011. The second point is that margin debt trends tend to exhibit high degrees of autocorrelation. In other words, the last few months’ change in margin debt is the best predictor of the change we’ll see in the next few months. This is important because it means that margin debt, which retraced back to +0.53 standard deviations in November, still has a long way to go. We would need to see it approach -0.5 to -1.0 standard deviations before the trend runs its course. There’s plenty of room for short/intermediate term reversals within this broader secular move, as we saw in November and December's print of +0.55 and +0.53 standard deviations. Overall, however, this setup represents a headwind for the market. One limitation of this series is that it is reported on a lag. The chart shows data through December.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link below.