TODAY’S S&P 500 SET-UP – February 3, 2012

As we look at today’s set up for the S&P 500, the range is 10 points or -0.57% downside to 1318 and 0.19% upside to 1328.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 410 (-1563)

- VOLUME: NYSE 810.39 (-9.21%)

- VIX: 17.98 -3.07% YTD PERFORMANCE: -23.16%

- SPX PUT/CALL RATIO: 1.99 from 1.68 (18.45%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 45.43

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 1.82 from 1.82

- YIELD CURVE: 1.60 from 1.60

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Change in Nonfarm Payrolls, Jan., est. 140k (prior 200k)

- 8:30am: Unemployment Rate, Jan., est. 8.5% (prior 8.5%)

- 8:30am: Establishment Employment Survey Annual Revisions

- 10am: ISM Non-Manf. Comp, Jan., est. 53.2 (prior revised 53.0)

- 10am: Factory Orders, Dec., est. 1.5% (prior 1.8%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- President Obama delivers remarks on economy in Arlington, Va.

- House, Senate in session:

- House Ways and Means Cmte. marks up H.R.3865, the American Energy and Infrastructure Jobs Financing Act of 2012, 9am

- Joint Economic Committee holds hearing on unemployment report, with John Galvin of Bureau of Labor Statistics, 9:30am

- House Rules Committee meets to formulate rule on H.R.1734, the Civilian Property Realignment Act, 9:30am

- House Science, Space and Technology subcommittee holds hearing on science quality at EPA, 10am

- House Energy and Commerce panel holds hearing on Keystone XL Pipeline project, with testimony from U.S. Army Corps of Engineers, Bureau of Land Management officials, 10am

WHAT TO WATCH:

- Employers probably added 140k jobs in Jan. after a 200k-plus gain in Dec., economists est.; jobless rate may have held at almost 3-yr low of 8.5%

- Blackstone Group said to be studying leveraged buyout of Brocade Communications

- Panasonic widened annual loss forecast to record $10.2b

- Wall Street’s biggest lobbying group is split over a proposed settlement of state and federal foreclosure probes

- Greece’s rescue plan includes a loss of more than 70% for bondholders in voluntary exchange and loans likely to exceed EU130b now on the table

- European retail sales unexpectedly fell in December, led by Germany and France

- Hutchison Whampoa agreed to buy Orange Austria from France Telecom and Mid Europa Partners; deal valued at EU1.3b

- Nevada holds Republican presidential caucuses tomorrow

- No IPOs expected to price today

EARNINGS:

- Spectrum Brands Holdings (SPB) 6 a.m., $0.67

- Macerich (MAC) 6 a.m., $0.87

- Aon (AON) 6:30 a.m., $0.96

- Simon Property Group (SPG) 7 a.m., $1.90

- Beam (BEAM) 7:06 a.m., $0.67

- Tyson Foods (TSN) 7:30 a.m., $0.34

- Health Net (HNT) 7:30 a.m., $0.89

- Domtar (UFS) 7:30 a.m., $2.24

- Estee Lauder Cos (EL) 7:30 a.m., $1.01

- Spectra Energy (SEP) 8 a.m., $0.38

- Clorox (CLX) 8:30 a.m., $0.69

- Brown & Brown (BRO) Post-Mkt, $0.22

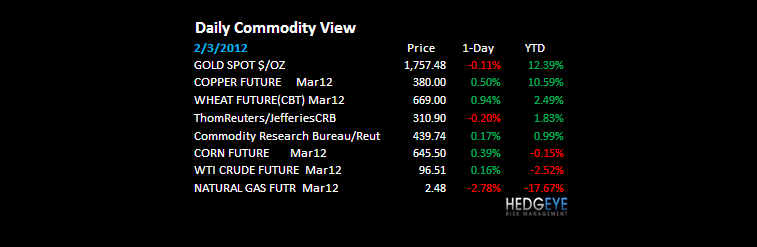

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Bets on Raw Materials Expanding Fastest Since 2006: Commodities

- Gold May Extend Gains From Two-Month High on Europe Debt Concern

- Brazil Sugar Crop Seen Failing to Compensate for Indian Drop

- Coffee Exports From Vietnam May Climb in February on Weather

- India May Make Enough Sugar to Meet Demand, Averting Imports

- Oil Near Six-Week Low Before Jobs Report; Brent Premium Widens

- Copper May Gain Before Figures Showing U.S. Employment Advanced

- Wheat Gains as Lack of Snow Cover Puts European Plants at Risk

- Rubber Gains, Paring First Loss in Five Weeks, as Oil Recovers

- Contango Widest Since October in Cushing Deluge: Energy Markets

- Glencore-Xstrata Bankers May Reap Up to $140 Million for Advice

- Saudis Set to Price Arab Heavy to Tap Fuel Oil Boom, Survey Says

- Ship Rates’ 63% Collapse Will Snap Share Rally: Chart of the Day

- Gold May Extend Gains From Two-Month High

- Copper Stockpiles in Shanghai Surge to 21-Month High

- Soybean Traders Most Bullish This Year on South American Weather

- Coffee Rebounds as Vietnam Sales May Slow in March; Cocoa Gains

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

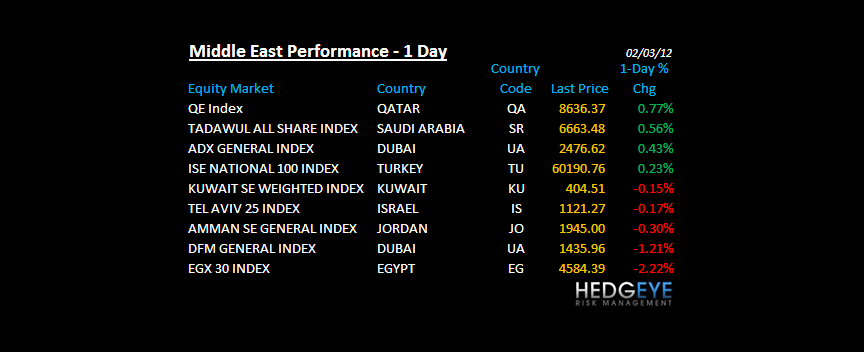

MIDDLE EAST

The Hedgeye Macro Team