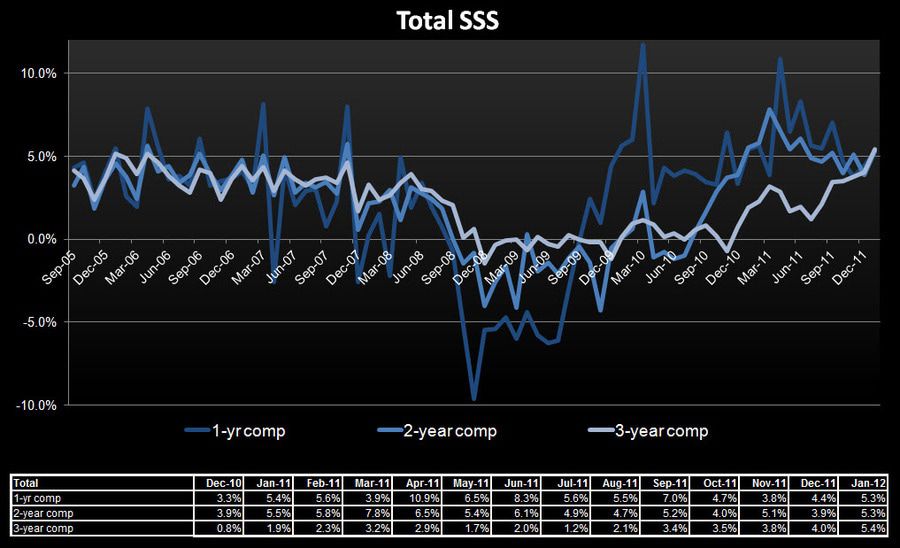

January sales appear to have improved on the margin, but let’s take a step back and keep the quarter in context. November kicked off the quarter with sales coming in lighter than expected following Black Friday bullishness. Then December disappointed with more companies guiding down than up. Then we have today’s results with the ratio of beats-to-misses coming in net negative (11 companies missed to 8 beats), but six companies guided Q4 higher while only one (SSI) guided lower. Dizzy yet? Quite simply, from start to finish Q4 has been weaker than originally expected especially in the mid-tier. The negative setup headed into 1H remains unchanged.

In taking a look back through not only the companies reporting monthly comps (an increasingly less relevant sample), but also the broader group over the last three months, we’ve seen 11 of companies lower expectations for the quarter compared to only 4 taking numbers higher. That’s not good. In addition, KSS taking Q4 EPS up by $0.09 after cutting it by $0.30 last month is hardly net positive. Also, let’s not forget JCP taking numbers down by 35% before officially bowing out of the monthly sales game. Take a look at the table below. It tracks company guidance throughout the quarter and the net change versus original expectations, not simply the most recent data point. Among the most notable negative callouts TGT, KSS, and JCP.

Volatility is clearly on the rise and continues to expand the bifurcation between upward and downward revisions. We fully expect this bifurcation to remain present through the 1H at a minimum in an increasingly more competitive pricing environment.

A few additional callouts in January:

- The High/Low-end performance spread remains divergent though higher-end sales slowing on the margin. Within department stores, JWN +5%, M +2.4%, SKS +10.5% and Neimans +9% remain positive despite both JWN and M comping below expectations in January compared to KSS +0.6%, SSI -0.1%, and BONT -3.5%.

- Not surprisingly, off-price retailers TJX & ROST were the most positive standouts in January coming +7% and +5% respectively and ahead of expectations. The off-price channel is beginning to emerge as an early beneficiary as the higher-end starts to decelerate and competition at the mid-tier heats up. Both increased their outlook for the quarter as well. Interestingly, ROST was the first retailer to offer up its view of F13 at $3.12-$3.27 vs. $3.21E.

- Following a very strong December, M missed expectations in January, but raised guidance for the second quarter in a row. Online remains a key driver up +39% in Jan and +40% for the quarter and year.

- Food/Grocery continues to outperform driving results at discounters. Both COST and TGT reported the food/grocery up HSD and low-teens respectively outpacing all other categories with inflation still up LSD. While both came in better than expected, TGT is the notable callout given the sequential reacceleration in the monthly comp for the first time in four months. Improvements in the Apparel and Home categories were key incremental improvements – especially Home up LSD, positive for the first time since September.

- January marks the first month ex-JCP. There goes another $18Bn of sales relevance out of the SSS sample.

- GPS posted negative comps again -4.0%, but more importantly above expectations (-5.3%E). Despite missing comps in the first two months of the quarter, the company is either getting less promotional or more aggressively cutting expenses as the company took Q4 EPS up to $0.41-$0.42 vs. $0.35E. This is more positive for GPS on the margin given just how low expectations are, but our bet is that it's the later and stress amongst its competitors in the mid-tier remains a major overhang.

- The only commentary on inventory levels came from TGT, TJX, and GPS all of which were positively skewed.

- At the category level:

- Handbags and accessories were strong particularly at the high end with JWN, SKS, M, and Neimans all highlighting the category. Good for COH, KORS, and LIZ.

- Home was another positive callout by TGT, KSS and DDS.

Longs: LIZ, WMT, NKE, RL

Shorts: JCP, SHLD, HBI, CRI, HIBB

![]()

Casey Flavin

Director