“You know far less about yourself than you feel you do.”

-Daniel Kahneman (Thinking, Fast and Slow)

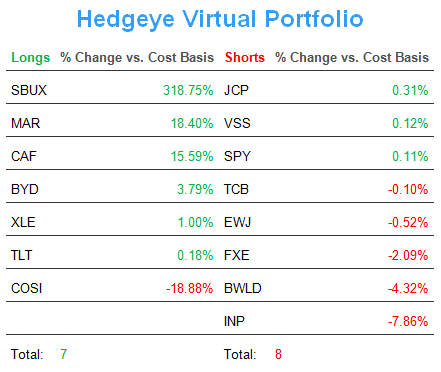

Since last Thursday, when I made the call to go to 91% Cash (selling my US Dollar and US Equity positions down to 0%), I’ve re-invested 12% of that Cash (on red) in the Hedgeye Asset Allocation Model, dropping my Cash position back down to 79%.

After I write something like that, you should feel something. ‘Who is this guy? That’s not what I do? I love this guy. He can’t do that. I think he played hockey, etc.’

I don’t know what you are feeling right now. All I know is that the more I think I know about risk management, the less I know. As a result, the best path forward is to Embrace Uncertainty, keep moving, and banging out the early morning reps.

Back to the Global Macro Grind…

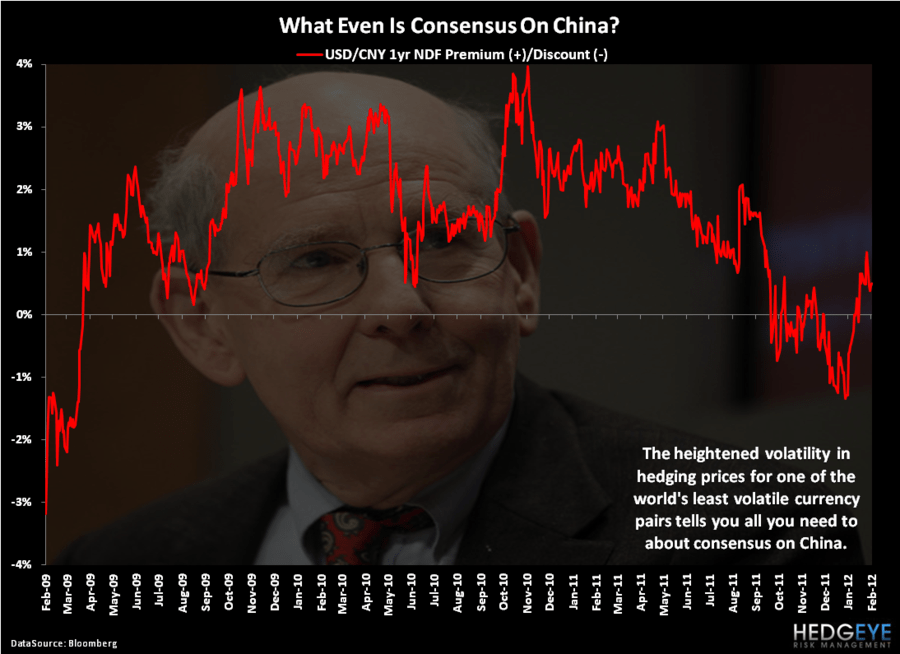

People on Old Wall Street are funny. Yesterday, at Bloomberg’s China Conference, our rising star Asia analyst, Darius Dale, commented “this is really weird – I just spent the whole day listening to American investors tell me everything that they know about China.”

Where were the people from China?

I don’t know. What I do know is that there are highly intelligent people in this business that tend to think they know a lot more about what they don’t know than they actually do.

This, of course, isn’t new. In Chapter 4 of “Thinking, Fast and Slow”, The Associative Machine, Kahneman takes a step back to remind us that David Hume boiled this down to 3 principles of associative thinking in 1748: “resemblance, contiguity in time and place, and causality.” (page 52)

In other words, since most Perma-Bulls have been blown up by bubbles in the last 4 years, China must be a bubble. It resembles a bubble, right? We’re all here at the China Conference telling one another it’s a bubble, right? And notwithstanding any correlation math, we can all agree that credit bubbles cause bubbles, right?

Right, right.

So, after Gary Shilling’s consensus headline coming out of the Bloomberg Conference was “China Headed for Hard Landing”, Chinese stocks closed up another +2% last night (we’re up +16% on our CAF position since buying it on December 29th, 2011) and the Hang Seng moved to +12.5% YTD!

I’m Feeling Certain now that something hard landed somewhere last night, on a Chinese short sellers head.

Does that mean we run out and buy more China this morning? Of course not. It’s just a simple reminder that if some US centric investors don’t know what they don’t know about their own Macro market moves, how on God’s good earth do investors trust that they can pin the tail on the donkey on a 12 hour plane ride from Newark?

Back to our positioning in the Hedgeye Asset Allocation Model – here it is as of last night’s US market close:

- Cash = 79%

- International Equities = 9% (China – CAF)

- Fixed Income = 6% (Long-term Treasuries – TLT)

- US Equities = 6% (Energy – XLE)

- Commodities = 0%

- International FX = 0%

Feeling Certain about any of these asset allocations or Hedgeye Porfolio LONG/SHORT positions we take is very hard to do. Feeling Certain that you can flip a switch from expecting Global Growth Acceleration to Deceleration in February is even harder to do.

With hindsight being crystal clear, the only thing I am certain about is how my model has worked over the last 4 years:

- When Inflation Expectations start to rise, people confuse commodity and stock market inflations with real-growth

- As real Growth Expectations start to fall, Gold, Treasuries, and Volatility start to rise

- As inflation expectations rise and growth expectations fall, confusion in markets starts to breed contempt

Confusion is as confusion does. The US stock market went down for 4 straight days after we made the move to 91% Cash last Thursday. After 1 up day in the last 5, the Perma-Bulls are back. But are they? How can you be perma bullish or bearish about anything after the last decade of getting paid to feel certain about everything?

My immediate-term support and resistance ranges for Gold, Oil (Brent), Copper, EUR/USD, Shanghai Composite, and the SP500 are now $1, $110.68-111.89, $3.75-3.83, $1.30-1.32, 2, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer