Chipotle put up an impressive top line but missed 4Q11 EPS. As we wrote last night, the stock needed perfection to keep the upward momentum going.

Chipotle posted comparable restaurant sales of +11.1% for the fourth quarter along with EPS of $1.81 or 23.1% above 4Q10. The Street was looking for $1.89 and the stock traded down immediately after the numbers hit the tape.

Below we go through some of our thoughts on the quarter.

Revenue

Chipotle’s top-line remains impressive although it is worth noting that January comps were approximated to be running at 10.1% by management. A 10.1% 1Q comparable restaurant sales number would represent the first slow down, on a two-year average basis, in comps since 4Q09.

What impressed us about the 11.1% number, albeit helped by 1% from favorable weather versus 4Q10, was that price accounted for 4.9% and traffic made up the remainder. Despite taking price well in excess of Food Away from Home CPI, traffic still contributed more than price to the comp.

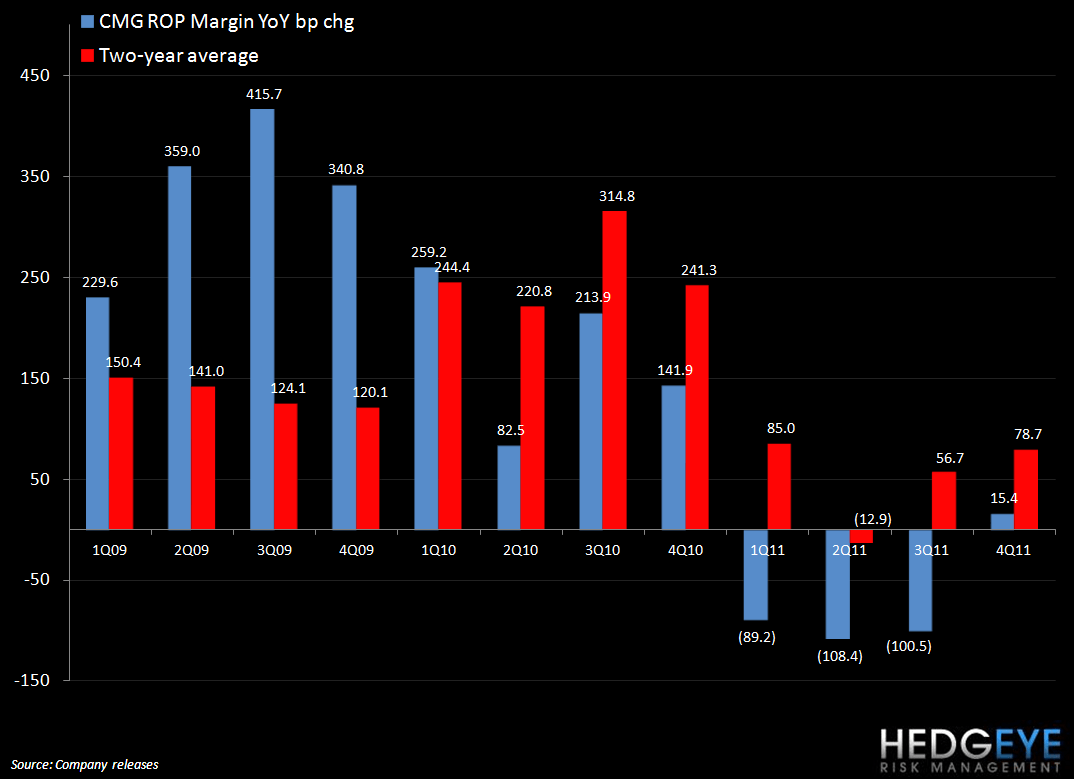

Margins

Restaurant operating margins grew year-over-year in the fourth quarter as a result of positive sales leverage. This was offset primarily by food inflation of 9% for the quarter. As a percentage of sales, food costs did improve sequentially from the third quarter by 90 basis points to 32%. This was aided by the company shifting from expensive California avocados to avocados harvested from Chile and Mexico. Food inflation in 2012 is expected to be in the mid-single digit range thanks to some more reasonable avocado, dairy and produce costs. Beef, chicken, and beans will offset that impact, however, with beef prices in particular expected to gain significantly.

Store Growth, Outlook, and Returns

With profit margins still strong and the company generating plenty of cash, we are not sounding any alarms for CMG here. The market is a discounting mechanism and, if results continue to disappoint it would mean continued price losses, we are going to remain neutral on this name until we gain conviction around a catalyst. The company grew its unit base 13% year-over-year in 2011.

Some comments on outlook:

- Unit openings in 2012 are expected to be between 155-165, which would imply 13% total unit base growth

- This growth is being sustained by strong real estate pipeline and increase mix of A-model locations (roughly 30% ’12 openings to be A-model format)

- Planning on opening a second ShopHouse restaurant in Washington D.C. later in ’12

- In London, two restaurants (in addition to the two currently open there) are under construction. The first Paris restaurant is opening in the spring

- The company is raising price roughly 1% in the Pacific region

- The board authorized $100m additional share repurchase program

As long as the company is growing successfully, and it has earned the right to grow, we do not expect an abrupt downturn in the stock price. The chart below, illustrating the Return On Incremental Invested Capital, shows how the CMG growth engine has driven the stock higher over the last few years. While less-than-perfect results will lead to declines of the order we saw in after-hours trading following earnings, the rich multiple is likely safe as long as the company can continue to drive strong margins and returns.

Howard Penney

Managing Director

Rory Green

Analyst