This week’s commodity chartbook shows significant gains in grains and chicken wing prices along with declines in beef, coffee, and chicken breast prices. Below is some commentary pertaining to select commodities and the companies that have exposure to them. Further on, we show the latest price charts of select commodities.

SUPPLY & DEMAND DYNAMICS

Beef – WEN, JACK, CMG, TXRH

Beef prices impact the prices of most restaurant companies but WEN (20% of food and paper spend), JACK (20% of commodity basket), TXRH, and CMG are especially exposed. Even companies that do not buy beef on the spot market are expecting significant margin pressure due to beef costs in 2012. The chart of live cattle prices, in the “charts” section of this post, below, shows just how far prices have run. Grain prices gaining over the past couple of weeks do not bode well for investors hoping for a rapid snap-back.

SUPPLY

Last Friday, the biannual cattle inventory report on Friday offered no surprise; short supplies and higher prices look likely over the next few months, at least. The impact of the 2011 drought is obvious in the numbers: cattle numbers in Texas are down by 11% from a year ago, and numbers in Oklahoma are down by 12%. Cattle and calf numbers in Florida, Mississippi, Nebraska and Wyoming were up by 5%, 6%, 4% and 5% respectively.

One point worth noting is that beef replacement heifers were up by 1% year-over-year. A replacement heifer is a young, female bovine that is raised for the purpose of replacing and improving the cow herd. This could suggest that producers in certain areas have begun to react to attractive prices by starting the process of expanding their herds.

DEMAND

Beef shipments strengthened for the week ended January 21st by 1,956 metric tons versus the week prior’s 13,128 as Mexico, Japan, and Canada purchased 5,100 MT, 3,000 MT, and 3,000 MT, respectively.

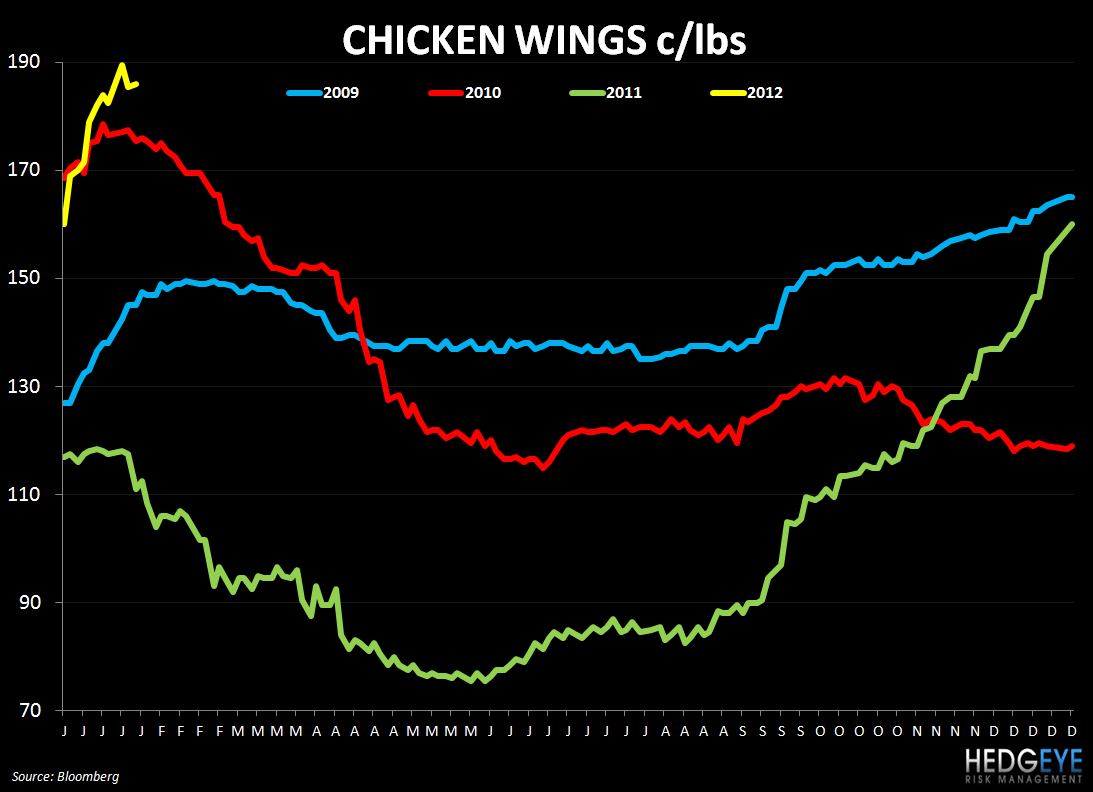

Chicken Wings – BWLD

Traditional chicken wing prices comprise 20% of sales, from a COGS perspective, for BWLD and we expect that the elevated level of wing prices will pressure EPS and bring estimates lower. FY12 estimates have not moved materially over the last few months, despite a steep gain in wing prices. 4Q11 estimates have gained, and the stock price has traded well over the last few days. Our thesis on the stock remains intact; we do not think the strong 4Q results which we and the market, obviously, are anticipating detract from our view. FY12 estimates need to come down, management guidance and tone needs to be revised from prior discussion on FY12 outlook, and the company still does not have the right to grow (fully capitalized sales to investment ratio of 0.91).

SUPPLY

Egg sets are still down ~5% versus a year ago as the food processor industry continues to search for profit. At the same time, wing prices continue to move higher.

DEMAND

We believe that the food service industry will continue to focus on chicken to offset the elevated levels of beef prices in 2012.

Wheat/Corn – WEN, TXRH, CMG, PNRA, DPZ

Grain prices have been climbing for the past two weeks. Bernanke’s sustaining of dollar-bearish monetary policy does not bode well for investors looking for substantially lower feed costs.

SUPPLY

Wheat is trading higher today as cold temperatures in Europe and Russia may damage the winter crop.

According to the Congressional Budget Office, improving yields in the U.S. over the next ten years should lead prices lower from current levels. In the near-term, however, lower yields in Argentina continue to support corn prices. Adversely dry and hot weather conditions are being blamed for the reduction in the Argentine crop.

DEMAND

Demand for grains should remain strong as demand for proteins, globally, remains strong. In terms of news flow, the supply side of the grains set up has been garnering more attention over the past week.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst