CMG is one of a long list of the companies we follow that is priced for perfection. Others include MCD, SBUX, YUM, DPZ, PNRA and BWLD. Given the early read in this earnings season, companies that are priced for perfection need to put up an exceptional quarter to keep the momentum going. We believe CMG will post some of the best numbers in the industry but whether or not it is going to be enough to keep the stock going higher is difficult to say.

Looking out to 2012, we see two important metrics that will help to determine how the rest of the year is going to shape up.

Chipotle is trading near its all-time highs and at 21x EV/EBITDA NTM, making it the most expensive stock in the space. We’re not making any call into the quarter; this business model has clearly surprised to the upside over the last few years. Here are two key points we will be watching for any sign of weakness. It should be noted that two other companies that the Street loves, MCD and SBUX, printed strong numbers last week but traded down because they missed expectations.

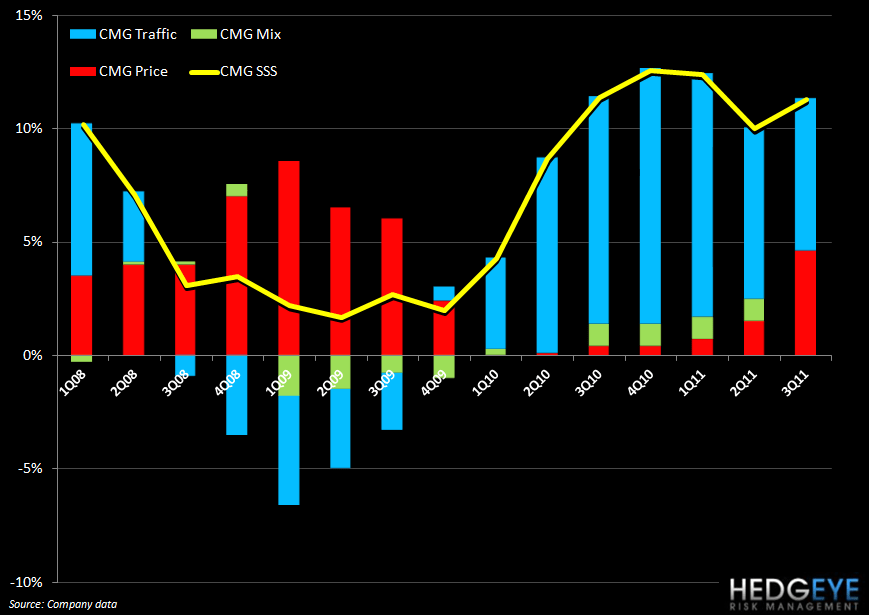

Is the company taking further price and did pricing impact traffic in 4Q11? The company suffered in early ’09 from a drop off in traffic after pricing was taken up to protect margins. While food inflation has subsided, we expect a continuation of margin pressure from those items that CMG relies on. CMG took significant pricing in 2009 and traffic did fall off precipitously. One could argue that the brand is stronger now, but we will be watching to see if the divergence between Food Away from Home CPI and CMG pricing grows any larger in 4Q. If, on the margin, other companys' offerings are perceived to be better value than Chipotle's, we would expect that to negatively impact traffic (second chart).

Is the company continuing to drive strong returns on incremental investment as it grows? This is a key metric we follow for restaurant companies that are growing. If the ROIIC were, any time soon, to come down from the best-in-class level it is currently at, we would expect the stock to trade at a much lower multiple. While we could see a dip in the stock price if the street’s expectations - particularly the anticipated 10.4% comp - are not met, we do not expect any larger correction until the ROIIC comes down much, much further.

Howard Penney

Managing Director

Rory Green

Analyst