He Won’t Be Retiring In Florida

Conclusion: Romney is going to win Florida, but it is increasingly looking like Gingrich will battle Romney all the way to the Republican convention. We believe this puts a Democrat sweep very much on the table.

In the second half of October and early November last year, the Republican nominating process looked like all but a coronation for former Massachusetts Governor Mitt Romney. The contract on InTrade that calculated whether he would become the next nominee was trading at over a 70% probability after never trading above 40% prior to October 2011. By mid-November both Rick Perry and Herman Cain, who for short period of times led national polls, had completely flamed out. Then, of course, along came Newt Gingrich with his benefactor Sheldon Adelson.

The chart below from Real Clear Politics highlights the poll averages over the last year from the Republican field. Specific to Gingrich, the chart shows that for much of the race he was a non-factor, running as far back as sixth place. Slowly on the back of solid debate performances and the failures of Cain and Perry, Gingrich gained momentum as the right wing of the Republican Party coalesced around him. On December 13, 2011, Gingrich had the most commanding lead of the race with 35.0% of those polled supporting him versus only 22.3% for Romney. Since then, Gingrich’s polling has fluctuated dramatically. In the course of six weeks since December 13th, Gingrich’s polls have been characterized by volatility, reaching as low as 16.2% on January 16th and as high as 31.3% on January 27th.

Romney, on the other hand, has been the embodiment of controlled stability in the polls. Although he peaked at 31.2% in early January, his poll numbers have largely ranged between 20% and 25% since late July. It seems the Republican Party likes him, but not enough to enable him to land the knock-out blow and clinch the nomination, despite his superior organization and fundraising. The fundraising point has been critical to Romney turning the tide in Florida. As of Friday, Romney and his super PAC had spent $15.3 million in Florida buying media spots versus $3.4 million for Gingrich.

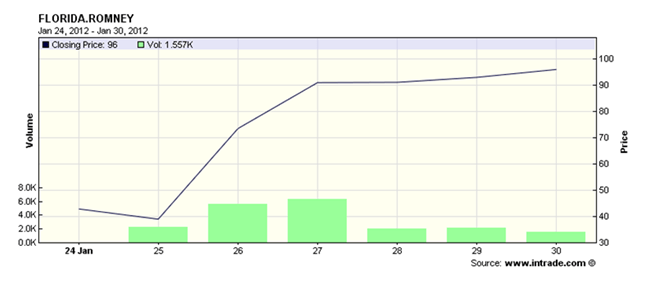

This spending, most of which has come in the last couple of weeks, has had a meaningful impact. In the chart below, we show the last seven days of the InTrade contract on whether Romney will win Florida. It has gone from ~40% to just under 95% in that period. This is also reflected in Florida-specific polls, as Romney has won in the last 14 Florida polls going back to January 22nd and currently holds an 11.5 point lead over Gingrich on the Real Clear Politics poll aggregate. Given the Florida primary is tomorrow, it is unlikely that anything will shake Romney’s sizeable lead.

Despite a likely loss by a wide margin in Florida, Gingrich has made one point very clear: he won’t be retiring his candidacy in Florida. In fact he stated to Politico this weekend, “I will go all the way to the convention. I expect to win the nomination.”

On some level, Gingrich appears to be adopting the Reagan strategy of 1976 when Reagan lost a number of early primaries, but won North Carolina, which shifted the momentum. In the end, Reagan lost by a handful of votes at the convention to Gerald Ford despite limited cash and a lack of establishment support. Following this tight loss, Reagan was lauded by conservatives for his efforts to push the Republican Party to the right.

The Gingrich camp is clearly trying to establish themselves as the conservative and right wing alternative to, as they call Romney, the “Massachusetts Moderate.” On some level, this position is working as Gingrich has repeatedly associated himself with Reagan and has seen his standing in national polls increase as more conservative candidates, like Cain and Perry, have exited the race. In fact, this weekend Gingrich actually received the tacit endorsement of conservative and Tea Party standard bearer Sarah Palin who said the following on Fox this weekend:

“We need somebody who is engaged in sudden and relentless reform and is not afraid to shake up the establishment. So, if for no other reason, rage against the machine, vote for Newt, annoy a liberal, vote Newt, keep this vetting process going, keep the debate going.”

In South Carolina, the exit polls showed very clearly that Gingrich is attracting the more conservative vote in the Republican primaries. In the ideology category of the South Carolina exit polls, Gingrich received 48% of the very conservative vote (which was 36% of the entire vote) versus 19% for Romney. In the same category, Santorum received 23% of the vote. Assuming that Santorum’s very conservative voters were split between Gingrich and Romney based on the 48% to 19% split it would have widened Gingrich’s victory by roughly 3.6%.

In the more broadly defined ideology breakdown of conservative versus liberal, which is represented by 68% and 32%, respectively, of those exit polled in Florida, Gingrich received 45% of the vote versus 23% for Romney and 19% for Santorum. Doing the same math as above, assuming a Gingrich and Romney split of Santorum’s votes, equates to an additional 2.7% margin for Gingrich based on those that define themselves as conservative.

Clearly, the combination of support from the Tea Party right and the actually internals from recent exit polls support Gingrich staying in this race, even if he loses by a wide margin in Florida. As well, a key strategic distinction that Gingrich has versus Reagan in 1976 may be money. Or at least the money of casino mogul Sheldon Adelson, who has an estimated net worth north of $20 billion and has already donated $10 million to Gingrich’s Super Pac. To the extent he wants to do so, Adelson certainly has the ability to keep Gingrich in the race.

So, what does the likelihood of an extended and bloody battle for the Republican nomination for the Presidency mean for the Republicans? Well, it seems to be conventional wisdom that it is not a good thing, and we tend to agree. Assuming Gingrich stays in the race to the bitter end, this could be an epic battle between the right wing and the moderate wing of the Republican Party, with the two candidates both likely to suffer ongoing and negative attacks from the other. This constant and negative barrage won’t be good for the candidates, or the Republican Party itself.

On the first point, President Obama has started to poll better compared to both Gingrich and Romney than he has in the last six months. In the most recent Rasmussen poll, Obama is up on Romney by +6 points and up on Gingrich by an astounding +17 points. Moreover, in the generic congressional polls, the Democrats for the first time in over a year are widening the gap from the Republicans, which we’ve highlighted in the chart below. Currently, the Democrats have an advantage of 44.0 to 42.2 versus the Republicans, for an advantage of +1.8. This is a stark contrast to their shellacking in the 2010 mid-terms.

The one election alternative that few pundits are considering currently is a Democratic sweep of the Presidency and both Houses of Congress. In an extended war between Gingrich and Romney, this scenario could be squarely on the table.

Daryl G. Jones

Director of Research