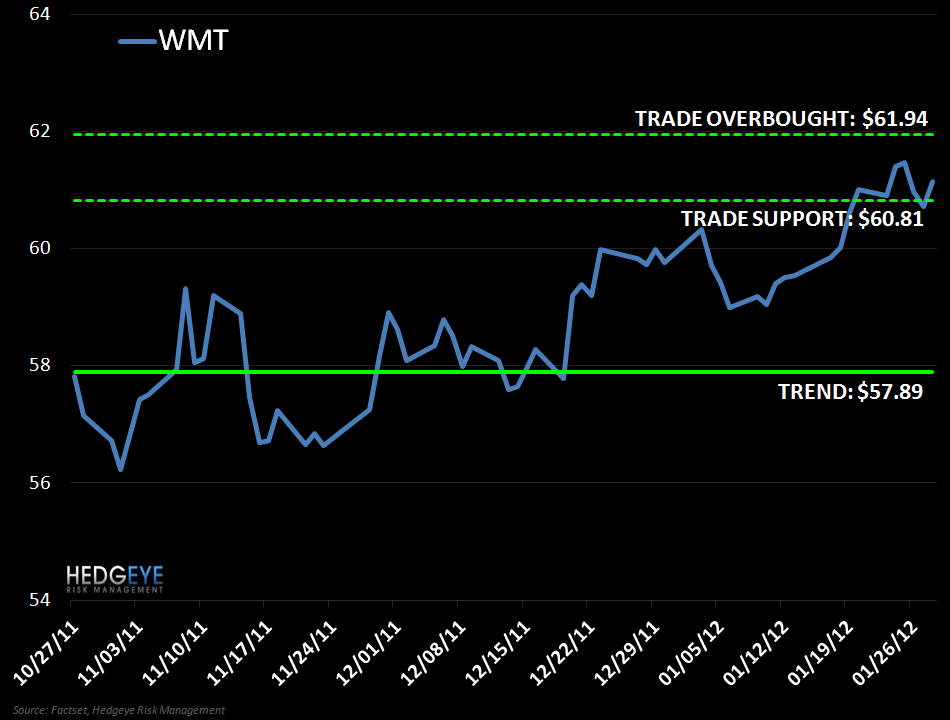

Keith back into WMT, one of the few retailers that will remain unscathed through the upcoming JCP-fueled apparel retail mele, to the Hedgeye Virtual Portfolio.

Keith back into WMT, one of the few retailers that will remain unscathed through the upcoming JCP-fueled apparel retail mele, to the Hedgeye Virtual Portfolio.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.