Positions in Europe: Short EUR/USD (FXE)

Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor".

If you'd like to receive the work of the Financials team or request a trial please email .

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 5 bps from last Monday to 77 bps today.

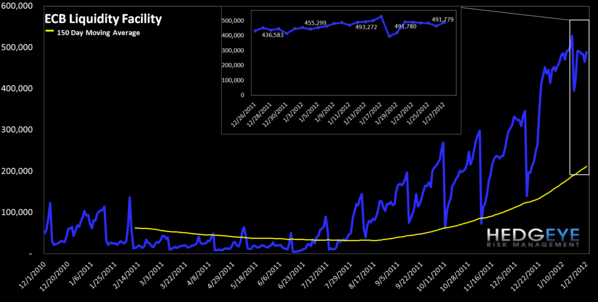

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

European Financials CDS Monitor – Bank swaps were tighter in Europe last week for 34 of the 40 reference entities. The average tightening was 2.3% and the median tightening was 9.4%.

Security Market Program – The ECB has still yet to publish its secondary sovereign bond purchases for the week ended 1/27 (normally due out by 10am EST on Mondays). It bought €2.243 Billion in the week ended 1/20 to take the total program to €219.0 Billion. We’ll post on the 1/27 amount as soon as it’s released.

A note on our short EUR/USD position and Europe’s Fiscal Compact illusions:

We remain short the EUR/USD via the etf FXE in the Hedgeye Virtual Portfolio. This is a position that has worked against us since last week’s announcements from President Obama (State of the Union Address) and Federal Reserve Chief Bernanke (FOMC Press Conference), both of which fundamentally changed our previously bullish outlook on the USD.

However, there’s been no resolutions out of Greece on PSI and increasingly Portugal is looking like the next Greece, which suggests we may see a chess fight between the EUR/USD for the weaker link of the pair. Also to note is that Germany has called to establishing a budget overseer in Greece to have strict control and veto power over Greece’s fiscal policy decisions going forward in return for bailout funds. Greece’s Finance Minister Venizelos adamantly rejected this plan and warned that “anyone who puts a nation before the dilemma of economic assistance or national dignity ignores some key historical lessons,” which signals to us that the Fiscal Compact being pushed in Europe has little hope of success as countries refuse to give up their sovereignty to Brussels (or Berlin). In short, we expect cultural difference to trump, and the union of uneven countries to struggle to resolve deep seeded sovereign disparities. In this light, we see a higher probability of intermediate term weakness in the EUR/USD.

Below is a heat map we use, courtesy of The Economist, which clearly shows the great difference in sovereign debt (as a % of GDP) across southern versus northern Europe. We expect this unevenness to have a long tail, and ultimately, and even if levels can be reduced through fiscal consolidation, to come at the expense of growth.

Matthew Hedrick

Senior Analyst