THE HEDGEYE BREAKFAST MONITOR

EARNINGS

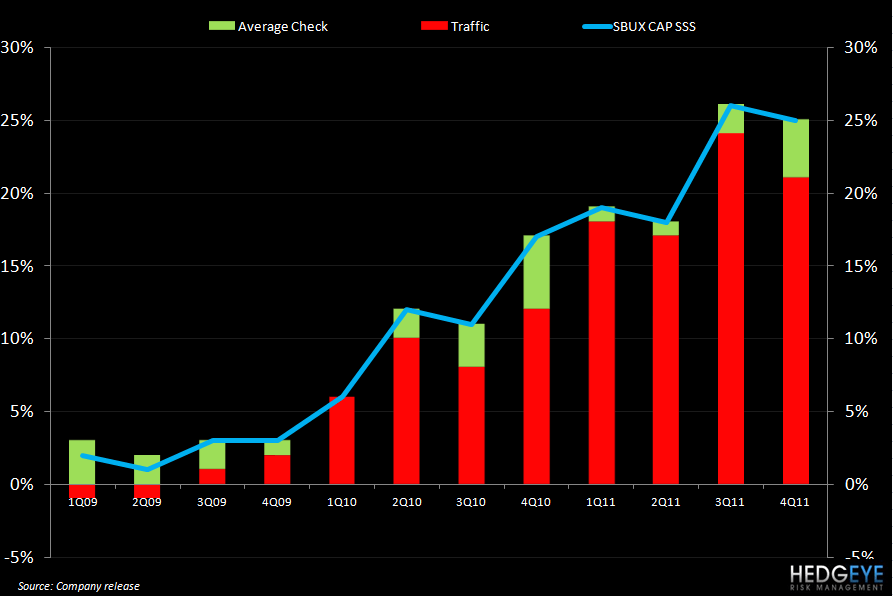

SBUX: Starbucks reported a solid quarter after the close but failed to reach expectations. The stock is trading down -1.7% in pre-market trading despite having reported EPS of $0.50 versus consensus of $0.49. U.S. comps came in at 9%, which represented a sequential deceleration in two-year average trends. With coffee costs locked through 1HFY13 (March), the top-line is the key variable from here. Management raised the lower end of the FY12 EPS guidance range by $0.03 to $1.78-$1.82 but consensus is looking for $1.84. Despite the impressive statistics around consumer loyalty, K-Cup pack shipments, and progress in China, the Street’s expectations being ahead of the company is dictating price action this morning.

MACRO NOTES

Comments from CEO Keith McCullough

The #BernankTax will be trending on a Twitter handle near you - that’s what a policy to inflate is:

- The Bernank Tax – Good morning America; you’re still seeing zero on the rate of return on your savings accounts and everything you put in your mouth or car is going up in price – try not to chomp on too many shiny rocks. Copper is up +14% for the YTD! Brent Oil prices are pushing for $112 and US Consumption stocks did not act well either yesterday or on good news (MCD and SBUX eps).

- GERMANY – these guys have to be smiling from ear-to-ear; they effectively gave the world’s Keynesian central planners the bird for 6 months and now the German DAX is up +11.1% YTD, busting a move above my long-term TAIL line of 6503 (DAX). Import Prices in Germany dropped in DEC to 3.9% y/y vs +6.0% NOV, so look for that price pressure to come back in Jan/Feb (BernankTax)

- JAPAN – how’s that 20yr Keynesian experiment treating you? We’ll have an in depth research note out on Japan again today; JGBs and Yens are not acting like we should be ignoring this risk like the Old Wall has – may be a bigger risk than Europe’s sov debt within 6 months. Shorting both Japanese Yen and the Nikkei on green days (FXY and EWJ).

Immediate-term TRADE range for the SP500 is now 1. I’m looking for a GDP miss vs heightened expectations at 830AM.

SUBSECTOR PERFORMANCE

QUICK SERVICE

COSI: Cosi reported company-owned comparable restaurant sales of +0.9%.

YUM: Yum’s Taco Bell is starting a new breakfast menu in 10 western states and will begin to offer the menu in the east of the U.S. in 2013.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

AFCE – up nicely following the preannouncement

KKD – up 8.5% in the past month and 9.8% YTD

CBOU – Hard to fight momentum with this stock in now up 23% YTD

CMG – 2/1 EPS date

WEN – Caught a downgrade this am 2/1 by UBS – good call ahead of the analyst day. We remain negative on TRADE

GMCR – The competition is heating up! Up 10% YTD

CASUAL DINING

BJRI – nothing new

CAKE – surprise move here but should trade in line with the market into the 2/10 EPS

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

Howard Penney

Managing Director

Rory Green

Analyst