Thinking Through the Implications of Where We Are on Jobless Claims

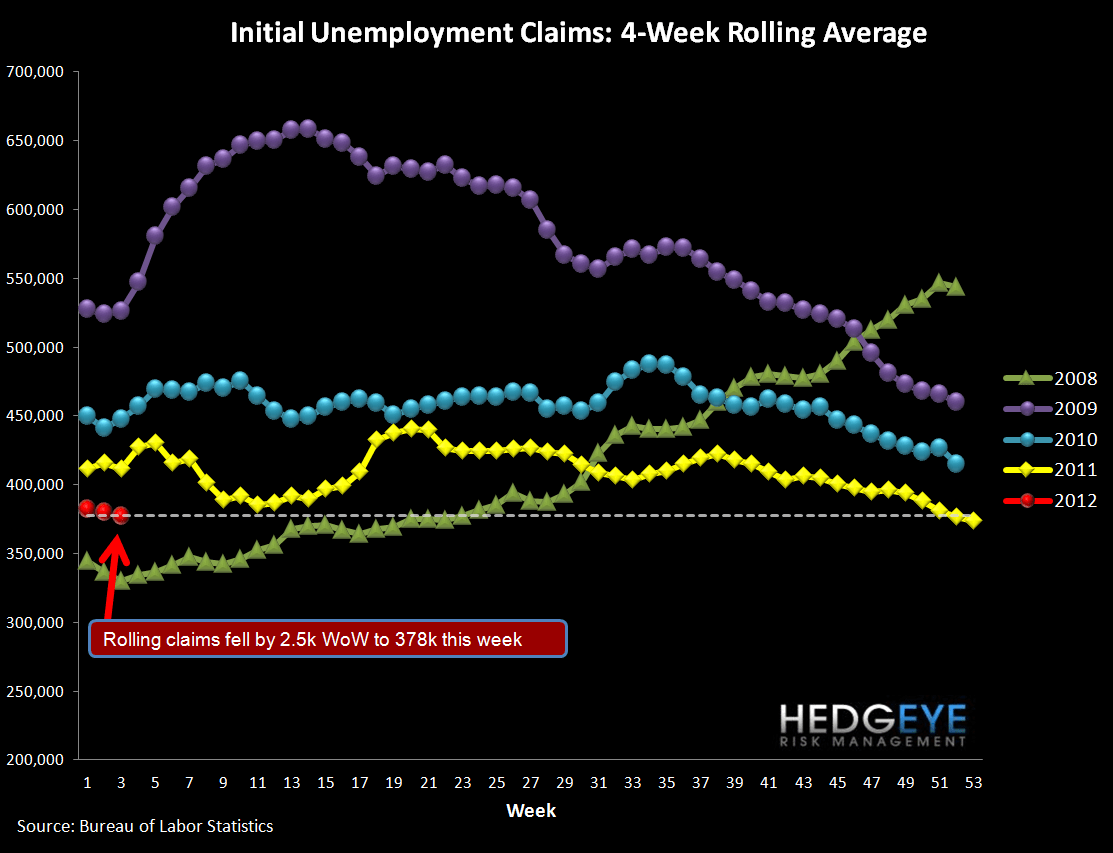

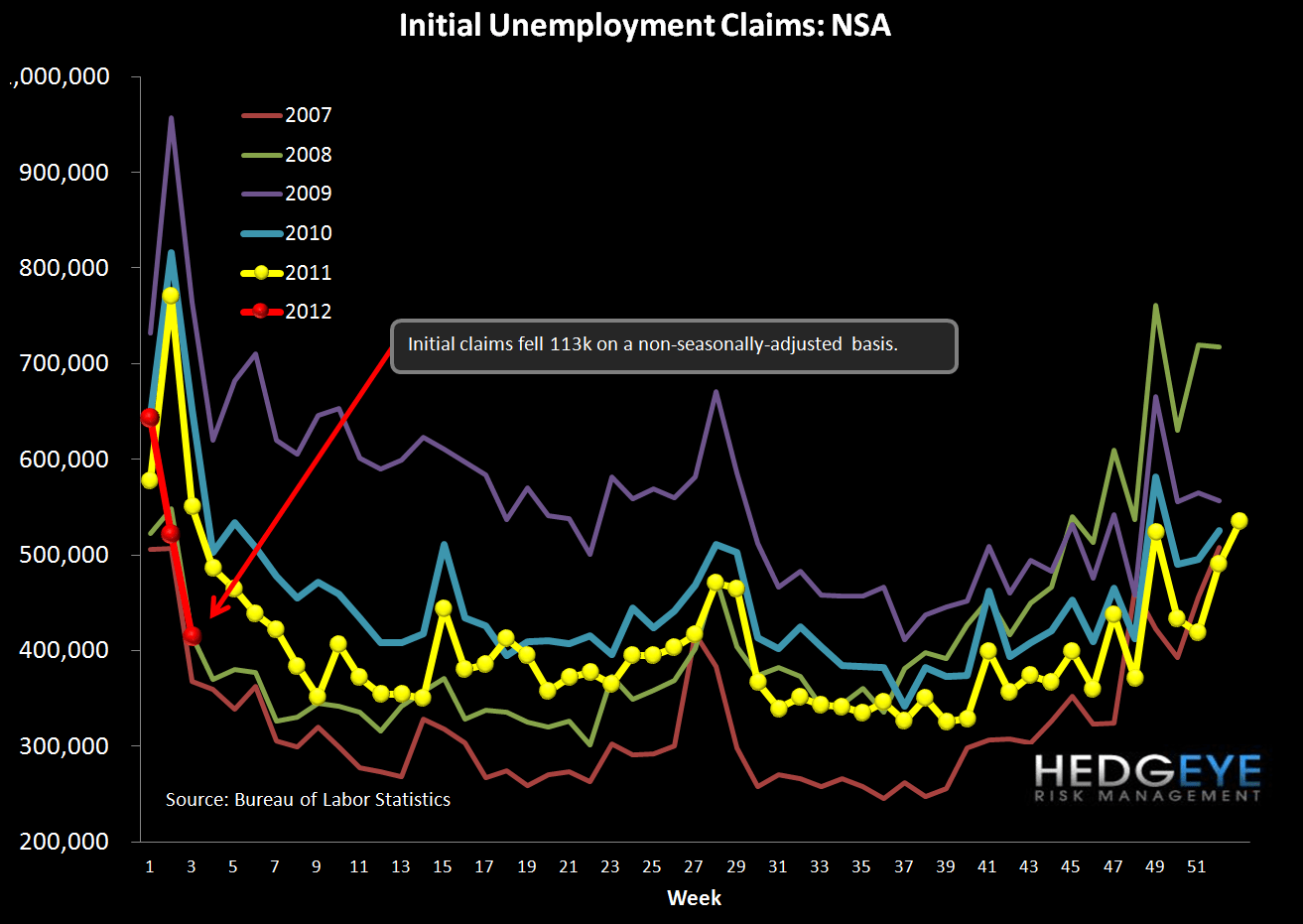

The headline initial claims number rose 25k WoW to 377k (up 21k after a 4k upward revision to last week’s data). Rolling claims fell 2.5k to 378k. On a non-seasonally-adjusted basis, reported claims fell 113k WoW to 414k.

Claims have been making solid progress YTD in spite of what is a seasonal-adjustment headwind tracing to the 2008/2009 move. This suggests that once we move beyond the early months of 2012, we could see claims continue to move lower as that seasonal-adjustment headwind changes to tailwind. This should happen around the end of February. It's also important to understand the ramifications of what's happening. We've noted in the past that 375-400k on initial jobless claims is a Rubicon of sorts. As you cross below that threshold, the unemployment rate starts to show steady, ongoing improvement. Why does the unemployment rate matter when it is (a) a lagging indicator and (b) a made up number (i.e. labor force participation rates)? We think it matters to the average American as a sign of confidence in the economy. If Americans hear that the unemployment rate is falling, month in, month out, we think that resonates in greater confidence. All this puts the economy on a virtuous path. Remember that the economy is very autocorrelated, so once you get the jobs engine below the 375-400k level on claims the economy will gain a level of momentum on its own. This is what seems like a growing probability at this point, based on the trend in jobless claims.

If there's a wrinkle, it's that our Macro team has, just this morning, reversed its call on the US dollar from bullish to bearish. The thinking had been that the dollar was poised to rise as the strengthening economy alleviated the need for further monetary or fiscal stimulus. However, in light of the FOMC decision to extend zero rates through YE14 and President Obama's State of the Union Address, their view has shifted towards bearish dollar. On the margin, this is negative to our call and thoughts around jobless claims, as a weak dollar stokes inflation at the pump and the grocery store, among other places - effectively, a tax on the middle class and the poor. Beyond this, there is clearly new pressure placed at the long end of the yield curve, an additional negative for the sector. It's a balancing act weighing the prospects of job improvement against the tax created by weak dollar-induced inflation.

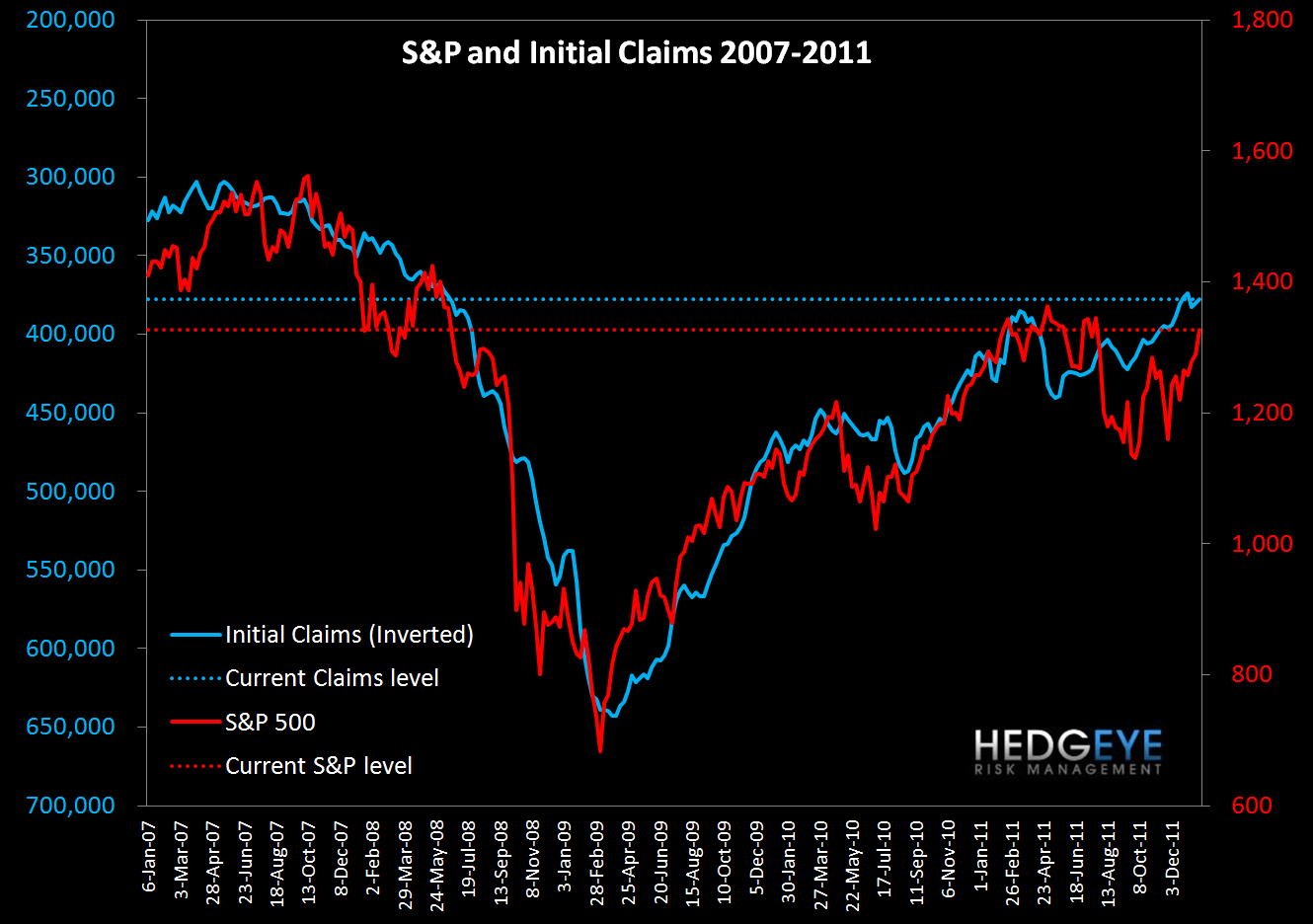

Another thing we are calling out is the large divergence between jobless claims and the market has narrowed considerably in recent weeks with the straight-up move in the market, and today the implications of full mean reversion are a much more modest S&P index level around ~1370. Alternatively, claims would need to rise to ~397k to meet the market where the market is. Neither of these are excessively removed from where they are relative to the magnitude of the dislocation we saw roughly a month ago.

2-10 Spread

The 2-10 spread widened 10 bps versus last week to 178 bps as of yesterday. The ten-year bond yield increased 10 bps to 200 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky