We remain positive on Brinker on all three durations (TRADE, TREND, TAIL). We view yesterday’s sell-off as offering a buying opportunity as current trends suggest that the company may comparable store sales targets for the full year. From a tail perspective, the long-term improvement to the operating platform at Chili’s, and the benefits that generates remains intact. From here, we see $5 of upside and $2 of downside.

We understand the stocks reaction to yesterday’s disappointing and decelerating sales trends at Chili’s. The 240% spike in volume versus the thirty-day average is significant. The Chili’s and/or Bar & Grill naysayers certainly enjoyed yesterday. The ride to $27 was painful for them and even with the stock at $25.66 many remain aggrieved. The Chili’s/ bar and grill naysayers are having a field day. Prior to that the run to $27 was a painful ride and with the stock settling in at $25 is still inflicts a certain about of pain.

Knowing we get marked to market every day, what do we do with the stock right here and now. Is it over or not? EAT’s balance sheet, free cash flow and margins are some of the strongest in the industry, so the investment case boils down to an income statement issue. More specifically, have the changes the company has made to the way Chili’s operates going to allow the positive momentum on traffic to continue for the balance of the fiscal year?

I’m not going to raise the white flag yet. We are staying positive on all three durations. Our thinking is focuses on four key points:

- The core competitors have responded to the Chili’s $6 lunch promotion but traffic trends early in the current quarter are remaining strong

- EPS revisions following the quarter just reported continue to be revised up. A trend that has been in place for the past 6 months

- Sentiment is overly negative

- Internally they continue to see positive momentum and the improvement in the macro environment is a net positive

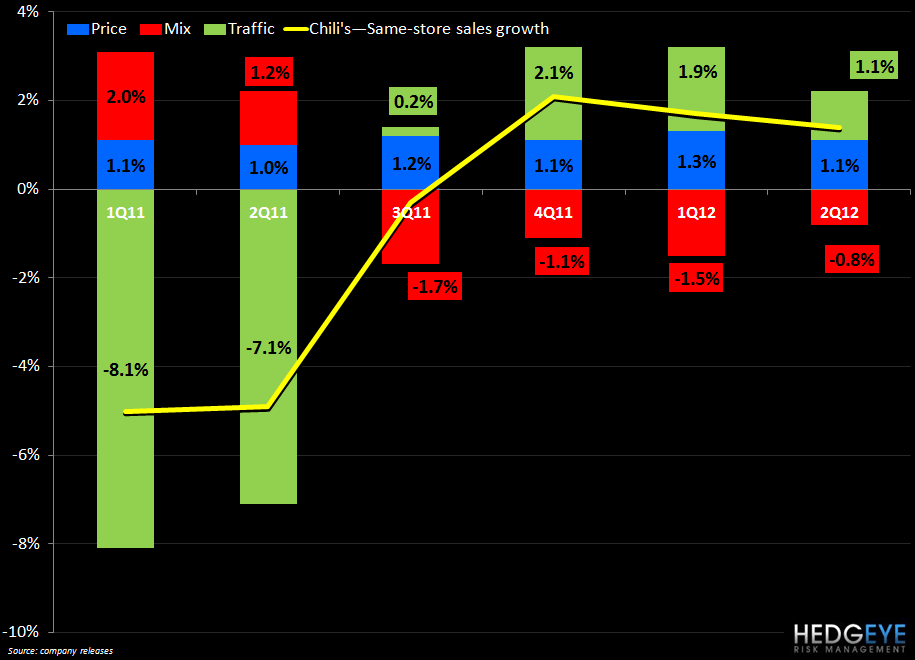

Yes the easy money in EAT has been made, but there is still more to come. The next quarter is where the rubber meets the road. I can see a plan that can get Chili’s same-store sales to 3-4% for the quarter (2% price, 1% mix and positive traffic), which will get the company back on track to the 2% guidance for the year. The wild card is what happens to traffic?

Traffic trends are helped by the fact that the macro trend is more positive on the margin, with the employment outlook and confidence improving. In addition, industry hiring trends continue to suggest that the demand picture in improving.

If you are bearish on the Bar & Grill space in general and don’t believe that the internal changes that management has made to the Chili’s concept are real you will not see our side of the story. Since announcing their version of the “plan to win” in 2010, management has delivered on what was laid out. The changes that have been made to the kitchen and the restaurant itself will boost the top line over time.

At 7.1x, we view the EV/EBITDA valuation as favorable based on current trends. From here, we see $5 of upside and $2 of downside.

Howard Penney

Managing Director

Rory Green

Analyst