THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

Chasing fire engines in Europe is over. Back to capitalizing on a process that absorbs globally interconnected risk:

- JAPAN – been a while since Japan was #1 in my morning macro grind, but this country’s failed Keynesian Experiment doesn’t cease to exist – the Yen getting spanked this morning after the Japanese announced they’ll miss both their topline (growth) and bottom line (budget) goals, again. Don’t forget Japan has to roll over 31.2% of its sov debt in 2012. That’s a lot of yens (231T).

- GREECE – the Athex Index is down -2.6% to 724 after going parabolic to the upside for the YTD. What’s next? News-flow is setting this up for central planners to come say they saved the day again – we’re all saved if this thing just goes away – funny how the dudes in Davos said Greece was a “one-off” just about now at this time LY. Greece’s TREND line = 709 on the Athex, watching that.

- GOLD – both Gold and Silver backing off at their intermediate-term TREND lines of $1688 and $32.69 resistance this morning. We’re short Silver as of Friday’s rip and looking to get back on the short side of Gold (and Gold related stocks). The critical signal in our model is a breakout in 10yr UST yield > 2.03% (TREND line). Gold has to compete w/ absolute levels of “risk-free” yield.

SP500’s immediate-term range = 1. Managing gross and net exposure to Global Equities w/ that in mind.

SUBSECTOR PERFORMANCE

QUICK SERVICE

MCD: McDonald’s reported 4Q11 EPS of $1.33 versus consensus of $1.29. December comps came in strong, at +9.8%, +10.8%, and +6.5% for the U.S., Europe, and APMEA, respectively.

CASUAL DINING

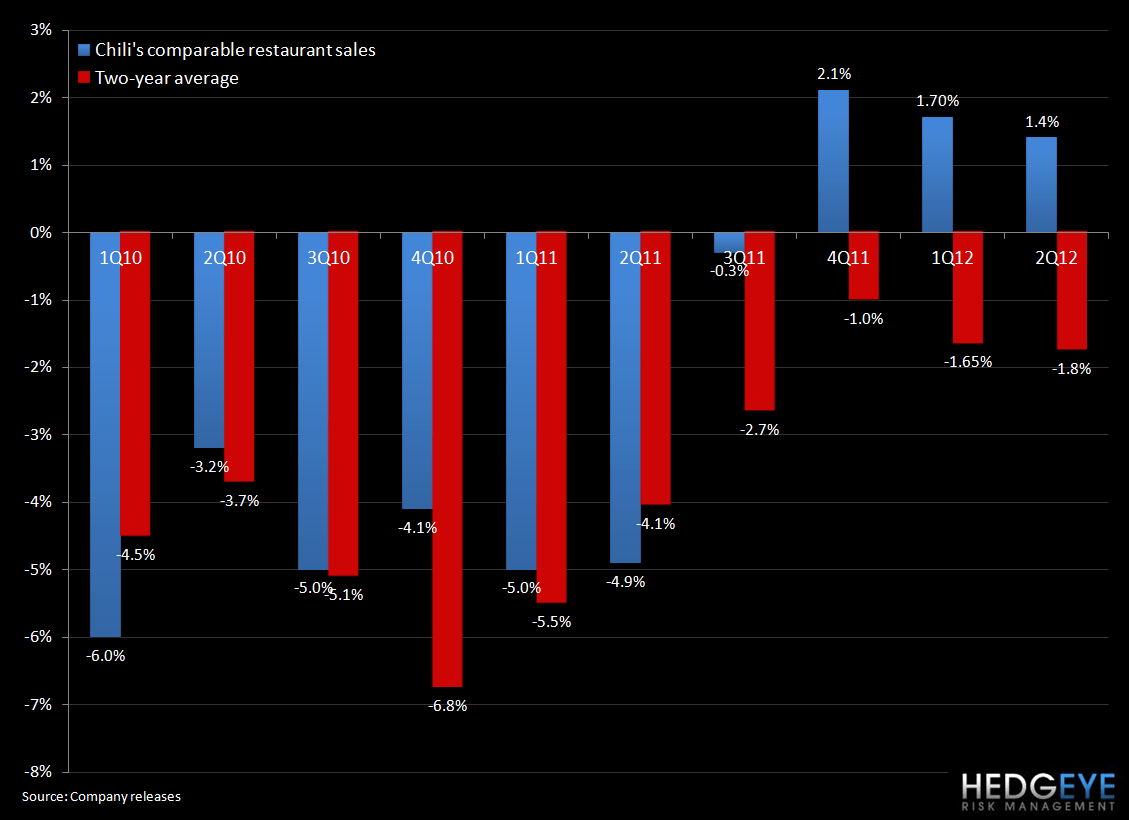

EAT: Brinker reported 2QFY12 EPS of $0.47 versus consensus $0.45. Margins came in at +17.9% versus consensus +16.9%. Despite this beat, Chili’s comps came in lighter than we or the Street had expected and the stock is trading down on that data point.

Chili’s sales are losing momentum. The $6 price point at lunch is no longer new news to most consumers. We are on the conference call listening for any clues as to what could bring around a pickup in same-store sales trends.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

CAKE: The Cheesecake Factory traded down -2.1% on accelerating volume. The company reports February 2010.

Howard Penney

Managing Director

Rory Green

Analyst