This note was originally published at 8am on January 19, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The only thing that’s gone up for the last 12 years is my weight.”

-Keith McCullough

Two nights ago Keith and I hosted a dinner for a number of our subscribers at the beautiful Patroon restaurant in midtown Manhattan. Keith’s quote above was in reference to asset classes generally. Now, truth be told, Keith and I snuck away to play noon hour hockey earlier this week and he’s actually staying in pretty good shape. Nonetheless, his analogy was an apt one. Asset class returns are not perpetual, nor are global macro investment views.

On the latter point, the big surprise we heard at the dinner and feedback from our Q1 Themes call last week is the shock that we are getting more constructive on equities and the U.S. economy. Yes, we are less bearish. Not raging bulls, per se, but on the margin less bearish. As a result we’ve upped the equity allocation in our asset allocation model to its highest level since mid-September ’11. So, what’s driving our more constructive outlook?

First, we believe the rally in the U.S. dollar will continue to gain momentum. The strength in the dollar is likely to be driven by a fiscal outlook in the United States that is improving, on the margin, due to automatic budget cuts via sequestration and the winding down of the Iraq war. In addition, both political parties have signaled, at least rhetorically, the importance of getting government spending under control, an issue that will be front and center in the 2012 election, and will likely lead to further budget cuts, or the perception of such.

The other key tailwind for the U.S. dollar is monetary policy. Since the financial crisis in 2008, the United States has led the world in accommodative monetary policy. This is changing and will continue to change. We believe the Fed is in a box related to its ability to implement additional quantitative easing due to an improving employment and economic growth situation. Conversely, central banks globally have plenty of room to ease, which naturally narrows the differential between U.S. interest rates and global rates. The most recent example of this is from China, where this morning reports suggest Chinese officials are weighing plans to relax capital requirements for the major Chinese banks. Add to this Brazil, which cut interest rates by 50 basis points overnight and the Philippines, which cut rates for the first time since 2009.

The primary benefit of a strong dollar is that it boosts the purchasing power of the U.S. consumer by deflating those commodities that are priced in U.S. dollars and by making global goods cheaper on a relative basis. This is important when considering the outlook for GDP since 71% of U.S. GDP is driven by consumption. Conversely, Eurozone government spending is almost 50% of GDP, which makes the outlook for European growth relatively bleak in comparison given the dramatic austerity being implemented in 2012. (Incidentally, a weak European economy and euro are also positive for the U.S. dollar.)

Last year at this time, consensus U.S. GDP estimates for 2011 were at 3.2% and came down steadily all year. It is likely that full year 2011 U.S. GDP comes in at, or under, 2%, which implies an almost 38% miss by the consensus Wall Street prognosticators. Call it process or luck, but we started last year with a much more pessimistic view of economic growth. Thus, for most of last year we were underweight equities and overweight fixed income, with a focus on FLAT and TLT.

This year the scenario is basically reversed. U.S. GDP consensus growth estimates are now just above 2% for 2012. Our models suggest a reasonable high end range of GDP growth in the U.S. could be 2.8%. This is almost 40% above the consensus number and an economic scenario in which growth is accelerating versus last year. Not surprisingly then, we have exited our fixed-income positions and have a much higher allocation to equities, both U.S. and global.

Currently, one of our key global equity positions is long Chinese equities via the closed end fund CAF. As of this morning, the position has already returned more than 15% for us in the Virtual Portfolio. Are we surprised? Well, perhaps by the rapid price appreciation, but it was a game of expectations in China. The Chinese bears have been perpetuating an end of the world scenario for China and the Chinese benchmark equity index was down more than -20% last year. Thus, when economic growth from China came in better than bad a couple of days ago at +8.9%, Chinese equities reacted favorably. This is not dissimilar to the economic setup we see in the United States.

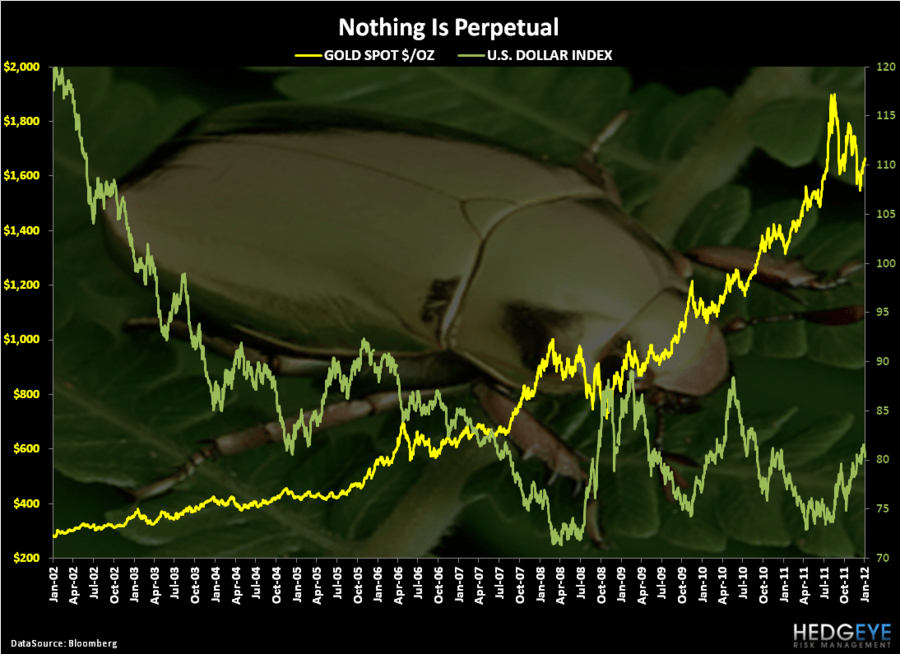

In the Chart of the Day today we’ve highlighted gold versus the U.S. dollar going back twelve years. The key take away from the chart is that bull markets in gold have been perpetuated by bear markets in the U.S. dollar. After gold has gone straight up for the last decade plus, it might not seem to be a contrarian call to suggest there is bubble in gold and it is potentially primed for a potential major correction, but there is major complacency related to gold. Unfortunately for the gold bugs, nothing goes up forever, not even gold. But if you don’t believe us, ask India, the world’s largest consumer of gold, who is set to import 54% less gold in Q4 2011 on a year-over-year basis.

If there is one truism of investing, it is that prices revert to the mean. As Jeremy Grantham once said:

“I got wiped out personally in 1968, which was the last really crazy, silly stock market before the Internet era….After 1968, I became a great reader of history books. I was shocked and horrified to discover that I had just learned a lesson that was freely available all the way back to the South Sea Bubble.”

No asset class goes up, or down, in perpetuity.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, US Dollar Index, Shanghai Composite, and the SP500 are now $1636-1675, $109.02-111.91, $1.26-1.29, $80.31-81.61, 2220-2354, and 1290-1310, respectively.

Keep your head up and your stick on the ice,

Daryl G. Jones

Director of Research