TODAY’S S&P 500 SET-UP – January 24, 2012

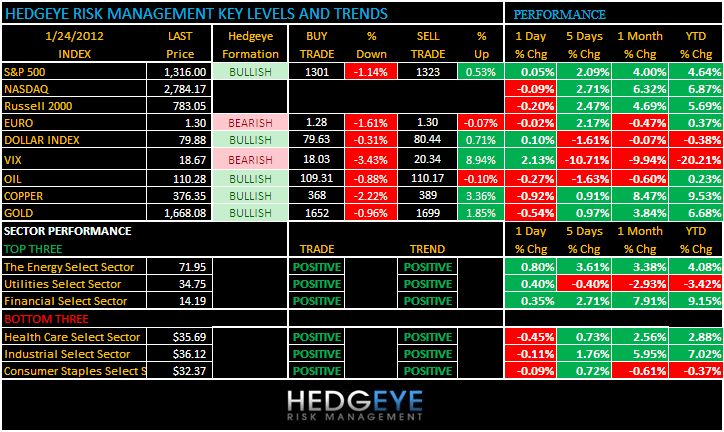

As we look at today’s set up for the S&P 500, the range is 22 points or -1.14% downside to 1301 and 0.53% upside to 1323.

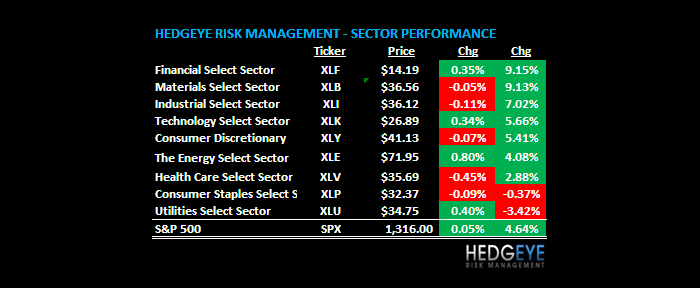

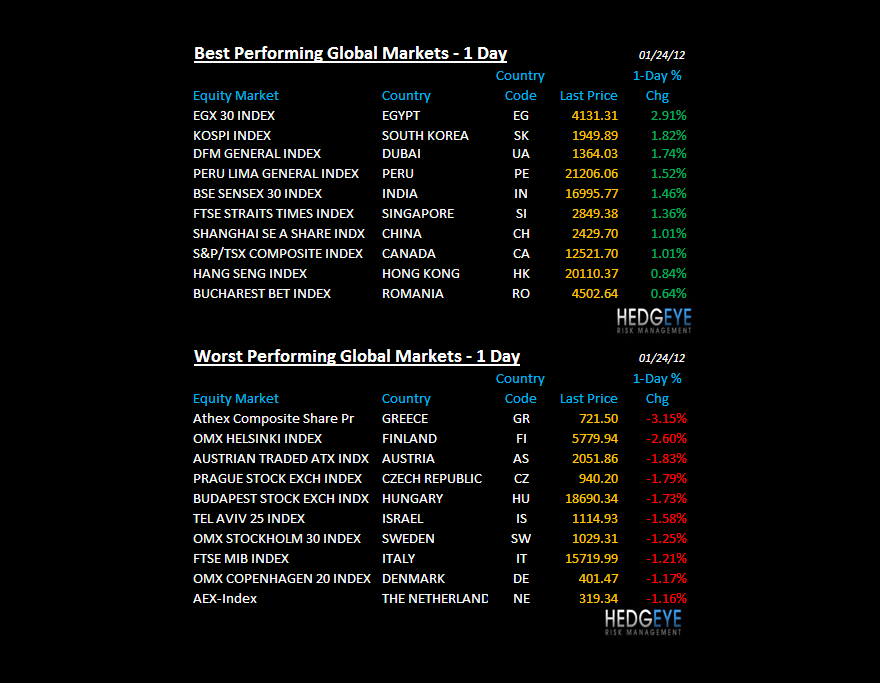

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 498 (9)

- VOLUME: NYSE 722.90 (-22.04%)

- VIX: 18.67 2.13% YTD PERFORMANCE: -20.21%

- SPX PUT/CALL RATIO: 2.35 from 2.54 (-7.48)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 52.45

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 2.04 from 2.05

- YIELD CURVE: 1.81 from 1.82

MACRO DATA POINTS (Bloomberg Estimates):

- 9am: FOMC begins 2-day meeting on interest rates

- 10:00am: Richmond Fed, Jan., est. 6 (prior 3)

- 11:30am: U.S. to sell 4-week bills

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 1:00pm: U.S. to sell $35b 2-yr notes

GOVERNMENT:

- State of the Union speech

- Romney attacked Newt Gingrich as an “influence peddler in Washington” and a failed leader whose party ousted him as U.S. House speaker in Florida debate

- Mitt Romney paid effective tax rate of 13.9% on income of $21.6m in 2010, according to a tax return his campaign showed reporters last night and will release today

- House, Senate in session:

- 1:30pm: Republicans on House Oversight panel to question Consumer Financial Protection Bureau Director Richard Cordray

- 10am: House Judiciary Committee marks up H.R. 1433, the “Private Property Rights Protection Act of 2011”

- 10am: Congressional Services Caucus holds discussion on Census employment data, broken down by congressional district

- 2:30pm: House-Senate Conference Committee meets on H.R.3630, the “Temporary Payroll Tax Cut Continuation Act of 2011”

WHAT TO WATCH:

- President Obama to give 3rd State of the Union Speech, focusing on economic concerns

- Oil traded near $100/barrel in New York on concern that Iran may respond to European crude-export embargo by disrupting shipping in Persian Gulf

- FOMC begins two-day meeting

- Apple reports earnings

- William Ackman says he will shield his choice to run Canadian Pacific Railway against possible loss of benefits after the retired executive’s former employer suspended pension and other payments

- Blackstone Group said to secure more than $6b of pledged capital for a new real estate fund that will buy mainly distressed-property assets

- The Earth will be bombarded today by strongest solar radiation storm in six years, with limited potential to affect satellites and power grids

- Oscar nominations to be announced ~8.30am

EARNINGS

- Ashland (ASH) 6am, $1.00

- EI du Pont de Nemours & Co (DD) 6am, $0.33

- Baker Hughes (BHI) 6am, $1.32

- Air Products & Chemicals (APD) 6am, $1.36

- Key (KEY) 6:20am, $0.21

- Travelers Cos (TRV) 6:30am, $1.52

- Quest Diagnostics (DGX) 6:45am, $1.06

- EMC (EMC) 7am, $0.46

- Coach (COH) 7am, $1.15

- MGIC (MTG) 7am, $(0.89)

- Regions Financial (RF) 7am, $0.06

- Waters (WAT) 7am, $1.50

- Harley-Davidson (HOG) 7am, $0.22

- Kimberly-Clark (KMB) 7:30am, $1.30

- Verizon Communications (VZ) 7:30am, $0.52

- Johnson & Johnson (JNJ) 7:45am, $1.09

- Brinker International (EAT) 7:45am, $0.45

- McDonald’s (MCD) 7:58am, $1.30

- Rayonier (RYN) 8am, $0.49

- Peabody Energy (BTU) 8am, $1.30

- Cooper Industries PLC (CBE) 8am, $0.95

- AK Steel Holding (AKS) 8:30am, $(0.39)

- Commerce Bancshares (CBSH) 9am, $0.70

- RF Micro Devices (RFMD) 4pm, $0.03

- Stryker (SYK) 4pm, $1.02

- Total System Services (TSS) 4pm, $0.31

- Norfolk Southern (NSC) 4:01pm, $1.40

- Canadian National Railway Co (CNR CN) 4:01pm, $1.25

- CA (CA) 4:02pm, $0.54

- Fusion-io (FIO) 4:05pm, $0.04

- Yahoo! (YHOO) 4:05pm, $0.24

- Altera (ALTR) 4:15pm, $0.42

- Advanced Micro Devices (AMD) 4:15pm, $0.16

- International Game Technology (IGT) 4:15pm, $0.22

- Apple (AAPL) 4:30pm, $10.12

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

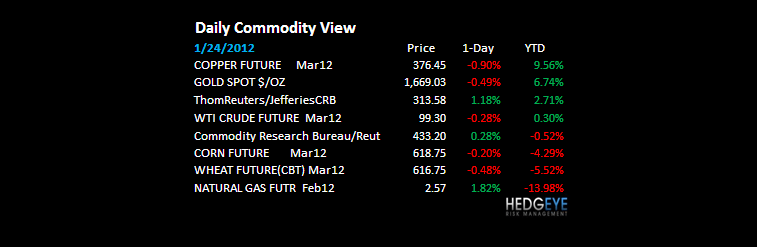

GOLD – both Gold and Silver backing off at their intermediate-term TREND lines of $1688 and $32.69 resistance this morning. We’re short Silver as of Friday’s rip and looking to get back on the short side of Gold (and Gold related stocks). The critical signal in our model is a breakout in 10yr UST yield > 2.03% (TREND line). Gold has to compete w/ absolute levels of “risk-free” yield.

- Record U.S. Beef Sales Seen as Japan Reviews Curbs: Commodities

- Oil Fluctuates as Iran Responds to European Crude Import Embargo

- Gold Declines as Rally to Six-Week High Spurs Investor Sales

- Copper Declines as Prices Near Four-Month High Prompt Selling

- Sugar Climbs a 13th Session as Mexico Output Falls; Cocoa Falls

- Soybeans Decline as Biggest Gain in Two Weeks Prompts Selling

- India Cuts Cotton Production Estimate as Disease Hurts Crop

- Natural Gas Rises a Third Day on Chesapeake Plans to Cut Output

- Oil-Embargo Rally Muted by Saudi Pledge, Libya: Energy Markets

- JBS Sale Shows Rising Demand for High-Yield Debt: Brazil Credit

- Sieminski to Leave Deutsche Bank to Head U.S. Energy Agency

- Cabot Production Growth Seen Cut as Gas Hits 10-Year-Low: Energy

- Detroit Aluminum Use Means New Muscle for Cars: Chart of the Day

- COMMODITIES DAYBOOK: Record U.S. Beef Sales Seen on Japan Review

- LME Copper Stockpiles at Two-Year Low Signal Falling Supplies

- West Europe Aluminum Output May Fall 500,000 Tons, Goldman Says

CURRENCIES

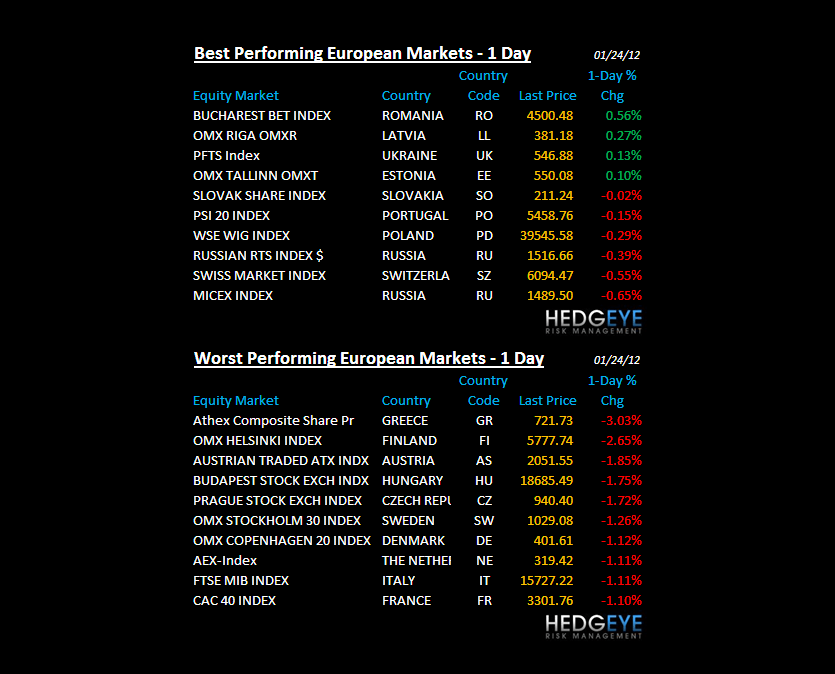

EUROPEAN MARKETS

GREECE – the Athex Index is down -2.6% to 724 after going parabolic to the upside for the YTD. What’s next? News-flow is setting this up for central planners to come say they saved the day again – we’re all saved if this thing just goes away – funny how the dudes in Davos said Greece was a “one-off” just about now at this time LY. Greece’s TREND line = 709 on the Athex, watching that.

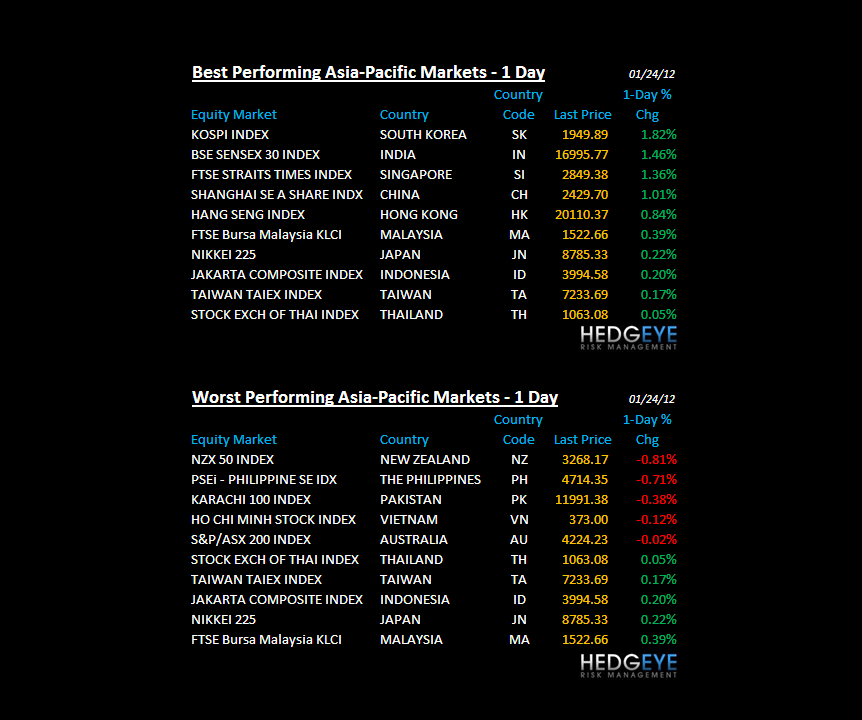

ASIAN MARKETS

JAPAN – been a while since Japan was #1 in our morning macro grind, but this country’s failed Keynesian Experiment doesn’t cease to exist – the Yen getting spanked this morning after the Japanese announced they’ll miss both their topline (growth) and bottom line (budget) goals, again. Don’t forget Japan has to roll over 31.2% of its sovereign debt in 2012. That’s a lot of yens (231T).

MIDDLE EAST

The Hedgeye Macro Team