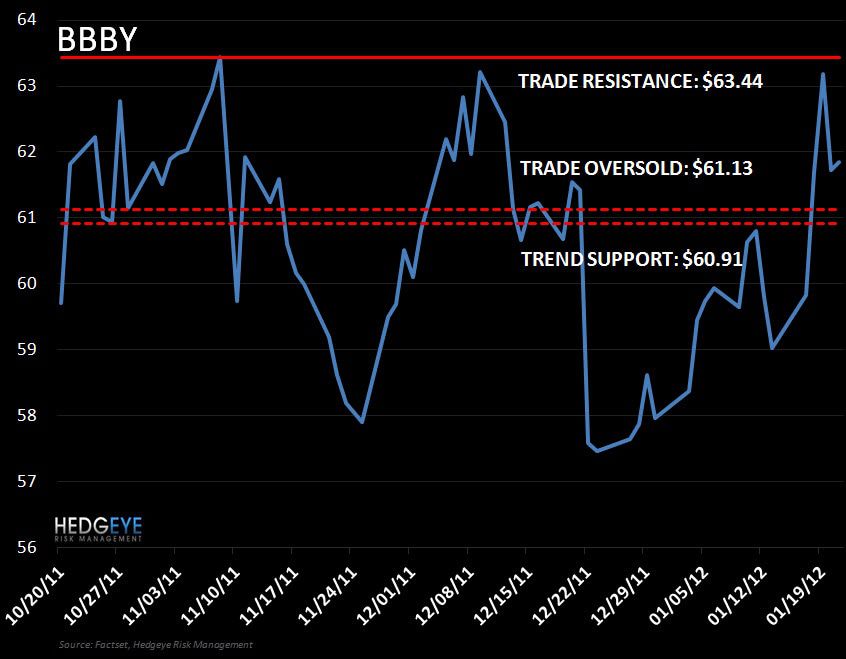

Keith is managing the immediate-term TRADE risk around one of our favorite shorts across all three durations covering BBBY in the Hedgeye Virtual Portfolio.

There is no change to our fundamental outlook.

Keith is managing the immediate-term TRADE risk around one of our favorite shorts across all three durations covering BBBY in the Hedgeye Virtual Portfolio.

There is no change to our fundamental outlook.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.