Positions in Europe: Short EUR-USD (FXE)

Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor".

If you'd like to receive the work of the Financials team or request a trial please email .

* The Euribor/OIS Spread, our preferred measure of systemic risk in the banking industry, tightened 5 bps last week. This is a strong bullish signal in our model. A similar trend has emerged in the TED spread, which fell by 3 basis points to 52 bps last week. Upward momentum in the TED spread is now definitively reversing. These trends are strongly positive for banking stocks as they reflate the existing European crisis discount.

* Bank CDS in Europe saw CDS fall 20% or more. The ECB Liquidity Recourse to the Deposit Facility made a cycle low on Wednesday at a much higher level than typical cycle lows before beginning to rise again. And the Securities Market Program bought €2.243 Billion in the week ended 1/20.

----------

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 5 bps to 82 bps.

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. The ECB pays lower rates than the market, so an increase in this metric demonstrates increased perceived counterparty risk and liquidity hoarding. The series made a higher low on Wednesday of last week but rose again to end the week at €492 Billion.

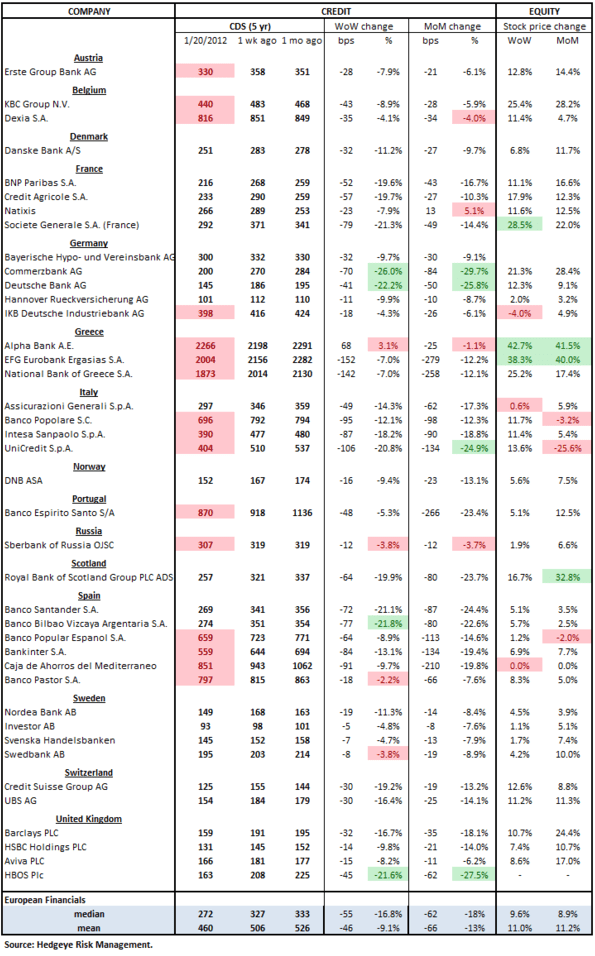

European Financials CDS Monitor – Bank swaps were tighter in Europe last week for 39 of the 40 reference entities. The average tightening was 9.1% and the median tightening was 16.8%.

Securities Market Program – The ECB's secondary sovereign bond purchasing program bought €2.243 Billion in the week ended 1/20 versus €3.766 Billion in the week ended 1/12 to take the total program to €219.0 Billion.

Matthew Hedrick

Senior Analyst