TODAY’S S&P 500 SET-UP – January 23, 2012

As we look at today’s set up for the S&P 500, the range is 23 points or -1.40% downside to 1297 and 0.35% upside to 1320.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

TREASURIES – the most important line left in our interconnected Global Macro model = the intermediate-term TREND line of 2.02% for 10yr US Treasury yields. The market closed right at that level on Friday and is holding it again this morning as Treasuries have their worst January start since 2003 (not Bullish on Growth period you wanted to be short in EM or US Equities).

- ADVANCE/DECLINE LINE: 489 (-433)

- VOLUME: NYSE 927.24 (+15.04%)

- VIX: 18.28 -8.00% YTD PERFORMANCE: -21.88%

- SPX PUT/CALL RATIO: 2.54 from 1.11 (128.83%)

CREDIT/ECONOMIC MARKET LOOK:

SPREADS – whether it’s the critical ones to counterparty risk (Euribor/OIS or TED) or the Yield Spread in Treasuries, the message is the same = bullish on the margin. And it’s what happens on the margin that matters to us most. Euribor/OIS down to 82bps wide this morn = 2.5 mth low. Yield Spread (10s minus 2s) +179bps wide; 3 month high (bullish for the Financials).

- TED SPREAD: 52.04

- 3-MONTH T-BILL YIELD: 0.04%

- 10-Year: 2.05 from 2.02

- YIELD CURVE: 1.81 from 1.78

MACRO DATA POINTS (Bloomberg Estimates):

- 11:30am: U.S. to sell $29b 3-month, $27b 6-month bills

GOVERNMENT/POLITICS:

- Newt Gingrich captured Republican primary in S.C. over the weekend

- Republican presidential candidates debate in Tampa, Fla.; Florida primary Jan. 31

- 9:30am: Energy Information Administration to release projections of U.S. energy supply, demand, prices through 2035

- Senate returns to Washington following winter recess

- NOTE: Obama State of the Union address Tuesday

WHAT TO WATCH:

- EU finance ministers meet in Brussels to discuss new budget rules, financial firewall to protect indebted states, Greek debt swap

- Thorsten Heins, to replace Jim Balsillie, Mike Lazaridis as RIM CEO; Barbara Stymiest to take over as Chairman

- Apache agreed to buy closely held Cordillera Energy for $2.85b in cash and stock

- EU foreign ministers may approve embargo on import of Iranian oil with phase-in period to July 1

- BAE plans to bid on contract to run Lake City Army Ammunition Plant in Independence, Missouri which Alliant has held since 2000

- “Underworld: Awakening” was top N.A. Film this weekend, taking in $25.4m

- No IPOs expected to price today: Bloomberg data

EARNINGS:

- Bank of Hawaii (BOH) 7am, $0.82

- Halliburton Co (HAL) 7:04am, $0.99

- VMware (VMW) 4pm, $0.60

- Woodward (WWD) 4pm, $0.45

- CSX (CSX) 4:01pm, $0.44

- FNB (FNB) 4:01pm, $0.19

- Polycom (PLCM) 4:04pm, $0.29

- Albemarle (ALB) 4:05pm, $1.10

- Kansas City Southern (KSU) 4:05pm, $0.79

- Zions Bancorp (ZION) 4:10pm, $0.33

- Western Digital (WDC) 4:15pm, $0.71

- Cathay General (CATY) 4:30pm, $0.29

- Texas Instruments (TXN) 4:30pm, $0.23

- STMicroelectronics (STM) 4:42pm, $(0.03)

- Crane (CR) 5pm, $0.90

- Packaging of America (PKG) 5pm, $0.37

- Equity Lifestyle Properties (ELS) 8pm, $0.87

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – wandering on up into no man’s land here (our intermediate-term TREND resistance = $1684). We have no short position, but we likely will again soon. All of the aforementioned will be very bearish for Gold (Growth + Rising 10yr rates). We need to get the Heli-Ben’s FOMC mtg out of the way Wednesday though…

- Speculators Raise Metals Wagers by Most Since July: Commodities

- Gold Climbs to Six-Week High on Europe Concern; Silver Advances

- Wheat, Corn Gain for Third Day as U.S. Export Sales Strengthen

- Copper Rises Before Finance Ministers Meet to Craft Crisis Plan

- Rubber May Drop ‘Sharply’ Through March, Goldman Sachs Says

- Iran Said to Seek Yen Oil Payments From India Amid Sanctions

- Sugar Climbs for a 12th Session in London Trading; Coffee Drops

- ICE Wheat-Market Bid Slowed by Canada Growers’ Fight With Harper

- ThyssenKrupp Advances on Stainless Merger Talks: Frankfurt Mover

- Rubber Retreats From 3-Month High on Oil’s Drop, Debt Concerns

- Fuel Glut Cuts Reliance’s Profit as Asia Adds Capacity: Energy

- Apache to Acquire Cordillera Energy Partners for $2.85 Billion

- Hedge Funds Oil Bets Drop on Iran Sanction Delay: Energy Markets

- COMMODITIES DAYBOOK: EU Diplomats Agree on Iran Oil Embargo

- Oil Climbs as European Union Agrees on Sanctions Against Iran

- WSI Says UK Weather to Be Colder Than Average Next Month

- U.S. Gasoline Rises to $3.39 a Gallon, Lundberg Survey Shows

CURRENCIES

EUROPEAN MARKETS

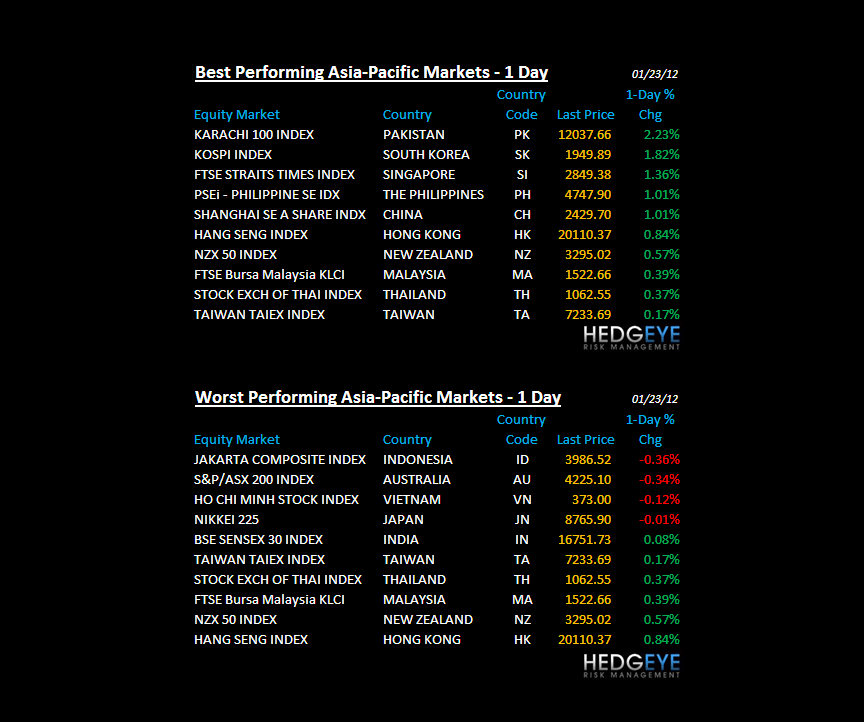

ASIAN MARKETS

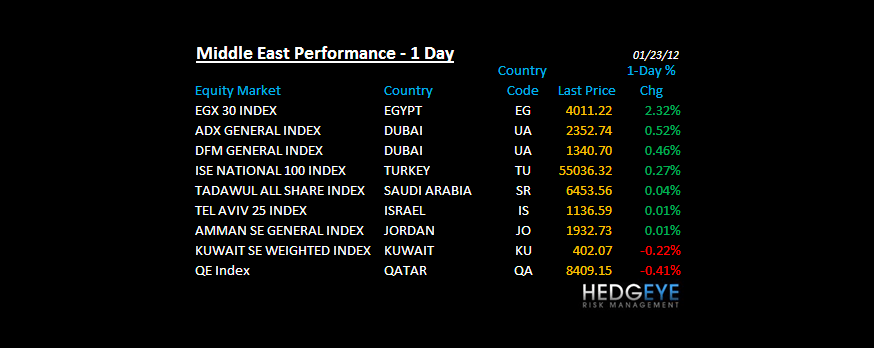

MIDDLE EAST

The Hedgeye Macro Team