Positions in Europe: Short EUR/USD (FXE)

Asset Class Performance:

- Equities: European indices were up across the board around +100-400bps week-over-week. Top performers: Greece 9.8%; Hungary 8.6%; Finland 5.7%; Czech Republic and Austria 5.0%; Germany 4.3%. Bottom performers: Slovakia -10bps; Norway +20bps

- FX: The EUR/USD $1.2924 or +2.0% week-over-week. Divergences: PLN/EUR +2.3%, HUF/EUR +2.2%; Iceland Krona/EUR -88bps

- Fixed Income: 10YR sovereign yields broadly increased w/w, led by Portugal +216bps to 14.62%; Spain +27bps to 5.49%. Italian yields declined -41bps to 6.23% and remained under the 7% level for the entire week. Greek yields came down -20bps but only to the lofty 34.16%.

Call Outs:

- EFSF cut to AA+ from AAA by S&P on Monday. Eurocrats attempt to downplay the event.

- IIF was in Athens this week to resume PSI talks however no deal was reached.

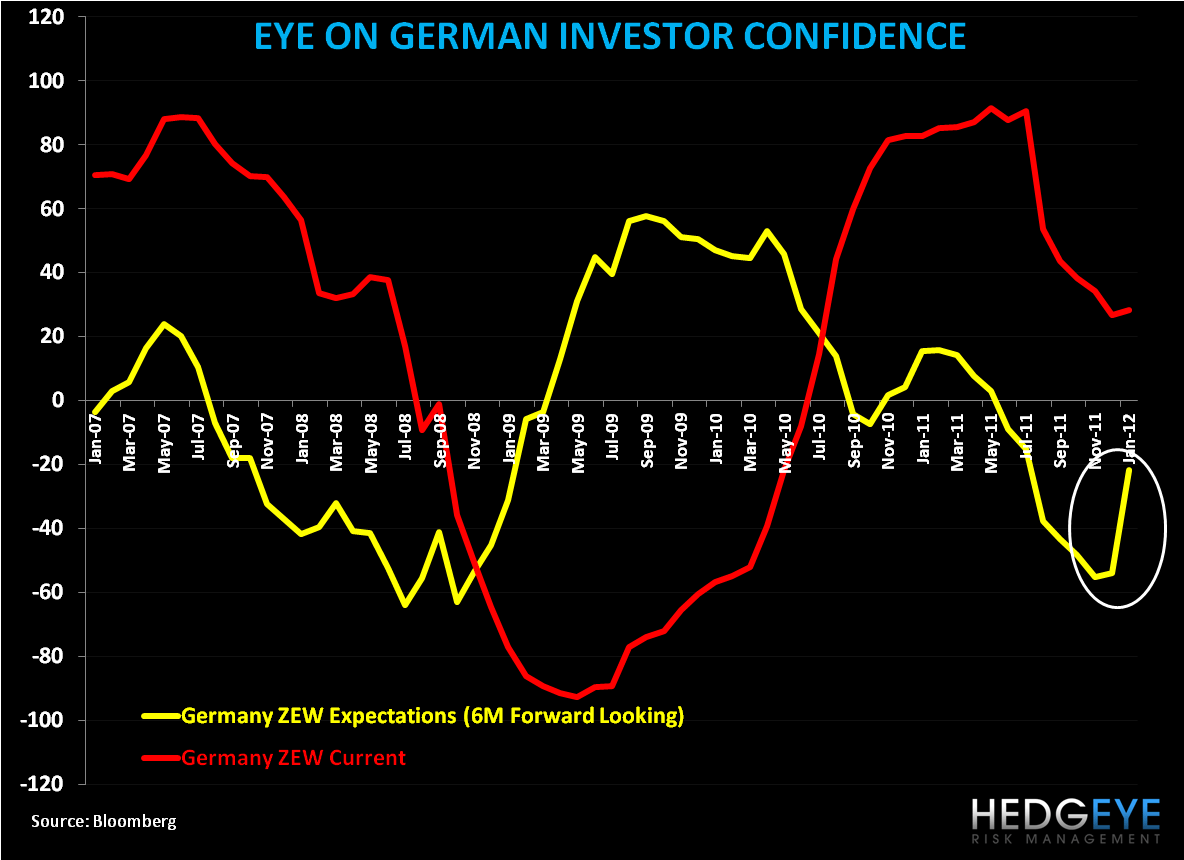

- Germany’s ZEW Confidence figures bounce (see chart of the week below).

- Strong Bond Auctions From Key Countries:

- Spain sold €4.88 billion of 12-18 month bills (on 1/17) with average yield of 2.049% vs 4.05% prior.

- France sold €7.97 billion of 2-3-4YR notes on 1/19, just short of its maximum target, with the average yield on the benchmark two-year notes sliding to 1.05% from 1.58%.

- Fitch Ratings Managing Director Edward Parker said "Greece is insolvent and will default on its debts. The euro area’s most indebted country is unlikely to be able to honor a March 20 bond payment of 14.5 Billion EUR ($18 Billion).

- IMF sees Eurozone GDP down 0.5% in 2012.

- Germany cuts its 2012 growth forecast to 0.7% from 1.0%.

In Review:

For a second consecutive week it has been a relatively quiet “news” week in Europe, however mania returned on Tuesday morning in the form of a “rumored” announcement that the IMF was asking for nations across the globe to contribute $1trillion to the IMF to aid Europe (the figure was then downgraded to $500 billion within an hour). In any case, the numbers don’t shake out and here’s why:

- Few countries across the globe have the extra cash (think bloated debts) to meet this sum.

- Most countries, like the U.S., which is the largest contributor to the IMF at 17%, don’t have the political support to lend as they turn to domestic fiscal consolidation.

- There’s still no confirmation that the €200 billion proposed to be raised by European Central Banks and a select few non-European CBs in early December last year has been committed.

- It is highly unlikely that an institution such as the IMF, which currently has $385 billion in assets to lend, would place its entire war chest on one region, Europe.

The IMF is looking for an agreement to be struck at the G20 FinMin meeting in Mexico City on February 25-26. We’d position that it’s highly unlikely this deal is met at its current value, and caution on the opinion that such a proposal could be included as evidence of a “Bazooka” to spur upshot in intermediate term European capital market performance.

This week the EU said it has toughened the language of its new fiscal treaty in response to ECB objections, however we remain of the opinion that a fiscal union in and of itself will do little to appease investors looking for a quick fix to European issues and the EFSF is far undercapitalize to deal with sovereign and banking defaults. The very back and forth and uncertainty around Greek PSI is evidence of perilous state of current Eurozone fabric – all week we saw a lack of decision on the issue. Truth be told, we may never see the exact agreement, but be sure, there will be numerous exceptions and loopholes in it, so that ultimately Greece may remain in default without defaulting. Perhaps we’ll learn more specifics on PSI at the Eurogroup and FinMin meetings beginning this coming Monday and Tuesday, respectively.

We’ll reiterate that the markets may turn based on headline risks, with Portugal perhaps the country waiting next in the wings (see yield and CDS breakouts below). We agree that markets may well find comfort in the LTRO to provide the needed liquidity to banks, which has been reflected in decreases in the Euribor-OIS spread over the last 15 days. And while the LTRO may prevent insolvency issues in the near term by boosting liquidity, it may only mask deeper risks. Between now and the mid-year, which is the deadline for banks to meet the 9% Tier 1 capital ratio, we may see dark clouds for banks in particular that need to raise capital. From a policy perspective, it appears Draghi may well hold interest rates unchanged until at least until March to gauge the progress of the LTRO program, and the second instalment on February 29.

Chart of the Week—Germany:

We’ve been getting more constructive on Germany in recent weeks on improving data. This week Germany’s ZEW investor confidence survey showed a major inflection on the 6M outlook, jumping to -21.6 in January vs -53.8 in December. We are very aware that despite Germany’s strong fiscal position (budget deficit = 1% in 2011 vs -4.3% in 2010) and employment base (unemployment rate = 6.8%), the country’s capital markets are not immune to the region’s sovereign and banking contagion risk. However, the broader equity market (DAX) has shown a great start to 2012, up +8.6% YTD, after falling -20% last year with a similar strong fiscal and employment profile.

Key Regional Data This Week:

Positives (+)

Germany Wholesale Price Index 3.0% DEC Y/Y vs 4.9% NOV

Turkey Consumer Confidence 92 DEC vs 91 NOV

UK CPI 4.2% DEC Y/Y vs 4.8% NOV

UK RPI 4.8% DEC Y/Y vs 5.2% NOV

Switzerland Credit Suisse ZEW Survey of Economic Expectations -50.1 JAN vs -72 DEC

UK Nationwide Consumer Confidence 38 DEC vs 40 NOV

Germany PPI 4.0% DEC Y/Y vs 5.2% NOV

UK Retail Sales w Auto Fuel 2.6% DEC Y/Y vs 0.4% NOV [+0.6% DEC M/M vs -0.5% NOV]

Negatives (-)

UK ILO Unemployment Rate 8.4% NOV (highest in almost 16 years) vs 8.3% OCT

UK Jobless Claim Change 1.2K DEC vs 0.2K NOV

CDS Risk Monitor:

-On a w/w basis, CDS was largely down across European sovereigns, with Portugal the exception. Italy and France saw the biggest declines at -33bps to 471bps and 186bps, respectively, followed by Spain -27bps to 381bps. Portugal popped, jumping +169bps w/w to 1,257bps.

EUR-USD

Keith shorted the EUR/USD via the eft FXE on Thursday (1/19) in the Hedgeye Virtual Portfolio with the price bumping up against our immediate term TRADE resistance level of $1.29. Our bearish view on the EUR and bullish view on the USD haven’t changed, but the price did. Keith took the opportunity to short FXE at $128.28. Our intermediate term TREND resistance level remains broken at $1.33 (see chart below). We think the lack of resolve from the newest proposals for a fiscal union will encourage greater downside.

The European Week Ahead:

Sunday: Finland Presidential Election

Monday: Eurogroup meeting in Brussels; Jan. Eurozone Consumer Confidence Indicator – Advance; Jan. France Production Outlook and Business Confidence Indicators

Tuesday: ECOfin Meeting; Jan. Eurozone PMI Manufacturing, Services, and Composite – Advances; Nov. Eurozone Industrial Orders; Jan. Germany PMI Manufacturing and Services – Advances; Jan. France PMI Manufacturing and Services – Preliminary

Wednesday: Jan. Germany IFO Business Climate, Current Assessment, and Expectations; UK Bank of England Minutes; Q4 UK GDP – Advance; Jan. UK Business Optimism

Thursday: ECB Policy Meeting; Feb. Germany GfK Consumer Confidence Survey; Jan. UK CNI Reported Sales and (Jan 26-31) House Prices; Jan. France Consumer Confidence Indicator and Business Survey Overall Demand; Dec. Russia and Sweden Unemployment Rates

Friday: Dec. Eurozone Money Supply; Q4 Unemployment Rate

Matthew Hedrick

Senior Analyst