TODAY’S S&P 500 SET-UP – January 20, 2012

As we look at today’s set up for the S&P 500, the range is 22 points or -1.64% downside to 1293 and 0.04% upside to 1315.

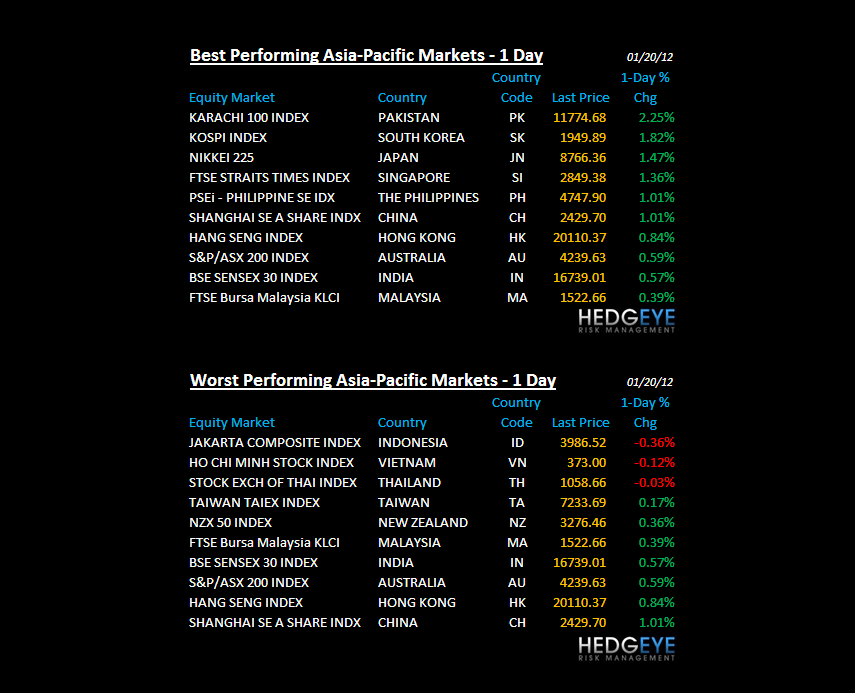

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

OVERBOUGHT – from the Hang Seng (+9.1% YTD) to the DAX (+8.2% YTD) and back again to the SP500 (+4.5% YTD), this season is not even 3 weeks old and we’ve already realized what we think is an outstanding YTD return on equity given the Bernank calls risk free 0%. Immediate-term overbought lines for HK, DAX, and SPX are 20,113, 6424, and 1315, respectively.

DEFLATING THE INFLATION – this is Global Macro Theme #2 for us here in Q1 and it really matters – across the board we’re seeing the impact of a Strong Dollar on DEC CPI and PPI prints across the world (US CPI dropped to 3.0% DEC vs 3.4% NOV, German PPI drops this morn to 4.0% DEC vs 5.2% NOV, New Zealand CPI falls hard to 1.8% in Q4 vs 4.6% Q3).

- ADVANCE/DECLINE LINE: 922 (-851)

- VOLUME: NYSE 806.03 (+1.04%)

- VIX: 19.87 -4.88% YTD PERFORMANCE: -15.09%

- SPX PUT/CALL RATIO: 1.11 from 1.67 (-33.53%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – it took all week for the bond market to give The Fed something to think about (as Growth expectations rise, interest rates should), but this breakout above my immediate-term TRADE line of 1.95% support for 10s matters. Seeing the 10yr consistently close > 2.03% would be very bearish for the long-bond, bullish for stocks (especially Financials).

- TED SPREAD: 52.05

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 1.99 from 1.98

- YIELD CURVE: 1.76 from 1.74

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: Existing home sales, Dec., est. 4.65m, up 5.2% (prior 4.42m)

- 10am: API monthly report

- 1pm: Baker Hughes rig count

WHAT TO WATCH:

- Sales of previously owned U.S. homes probably rose 5.2% in Dec. to 4.65m annual rate, highest level in more than a year, economists est.

- General Electric reports pre-mkt; has outperformed since Dec. investor meeting

- JPMorgan, State Street and Ameriprise Financial among final bidders for asset management division of Deutsche Bank: Reuters

- U.K. Dec. retail sales rose 0.6%, matching median forecast

- IMF cuts global growth forecast for 2012, Telegraph says, citing leaked memo

- Eastman Kodak got approval to borrow as much as $650m to support ops as it pursues patent sales

- European banks have until end of today to tell national regulators how they plan to meet capital targets, to then be discussed by European Banking Authority

- NYSE Euronext head says exchange may appeal if Europe blocks merger with Deutsche Boerse: WSJ

- Samsung Electronics lost patent infringement suit against Apple at court in Mannheim, Germany; first decision in group of patent cases cos. filed against each other in the country

- Carnival Corp. suspended broadcast, digital and direct-mail marketing for its namesake line

- Senate Minority Leader Mitch McConnell urged Democratic leaders to shelve anti-piracy bill; faces procedural vote Jan. 24

EARNINGS:

- Schlumberger (SLB) 6 a.m., $1.09

- SunTrust Banks (STI) 6 a.m., $0.27

- Prosperity Bancshares (PB) 6:03 a.m., $0.76

- Fifth Third (FITB) 6:30 a.m., $0.35

- General Electric (GE) 6:30 a.m., $0.38

- Comerica (CMA) 6:40 a.m., $0.51

- First Horizon National (FHN) 7 a.m., $0.14

- Parker Hannifin (PH) 7:30 a.m., $1.63

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Trims Weekly Gain as Greek Risk Offsets U.S. Rebound Hopes

- Gold Falls as Dollar’s Advance, Asian Holidays May Curb Demand

- Copper Falls as Chinese Manufacturing May Shrink for Third Month

- Copper Bears Retreat as Prices Rally Most Since ‘87: Commodities

- Sugar Rises on Limited Supply Before Brazil’s Crop; Coffee Gains

- Corn Declines as Council Forecasts Record Global Production

- Coffee Output in India May Miss Estimate on Rains, Group Says

- Pemex’s Offering Spurs Busiest Week Since August: Mexico Credit

- Korean Shipyards to Buy 12% Less Steel as Slump Hits Posco

- Gold May Gain 8.7% to Near Fibonacci Level: Technical Analysis

- Wildcatter Finds $10 Billion Drilling in North Dakota: Energy

- Batista’s MMX Not Interested in Deal With Falcone-Backed Ferrous

- North Korea Sees Chinese Storming in as Mineral Wealth Attracts

- COMMODITIES DAYBOOK: Gold Set for Best Weekly Run in Two Months

- Kinross in Play After Paying Too Much in African Gold: Real M&A

- U.S. Steel Bonds Rebound to Par on Auto Sales: Corporate Finance

- Copper Traders Probably Closed Out Bets on Declining Prices

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team