Positions in Europe: Short FXE

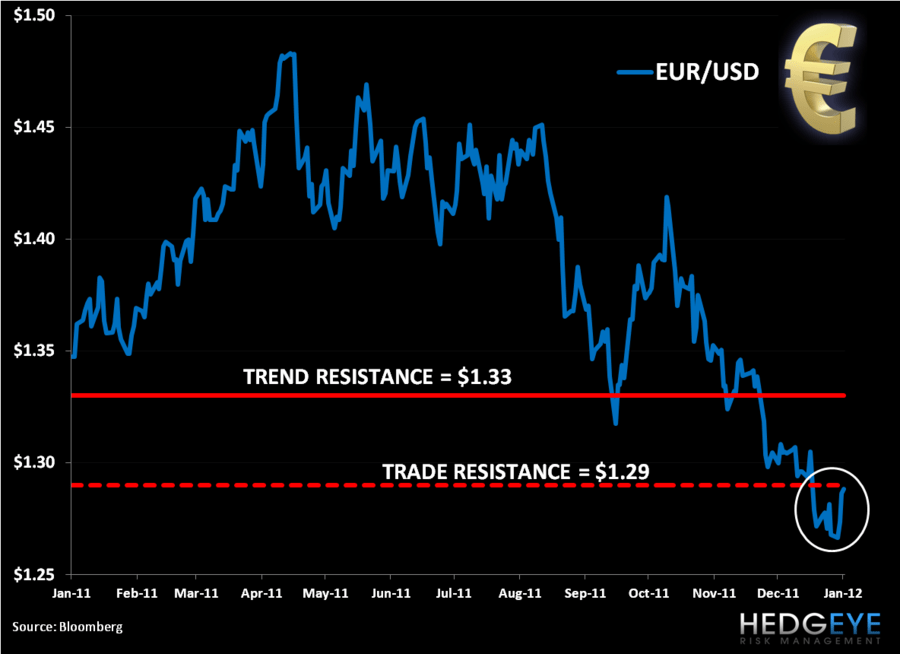

Keith shorted the EUR/USD via the eft FXE today in the Hedgeye Virtual Portfolio with the price bumping up against our immediate term TRADE resistance level of $1.29. Our bearish view on the EUR and bullish view on the USD haven’t changed, but the price did. Keith took the opportunity to short FXE at $128.28. Our intermediate term TREND resistance level remains broken at $1.33 (see chart below).

Matthew Hedrick

Senior Analyst