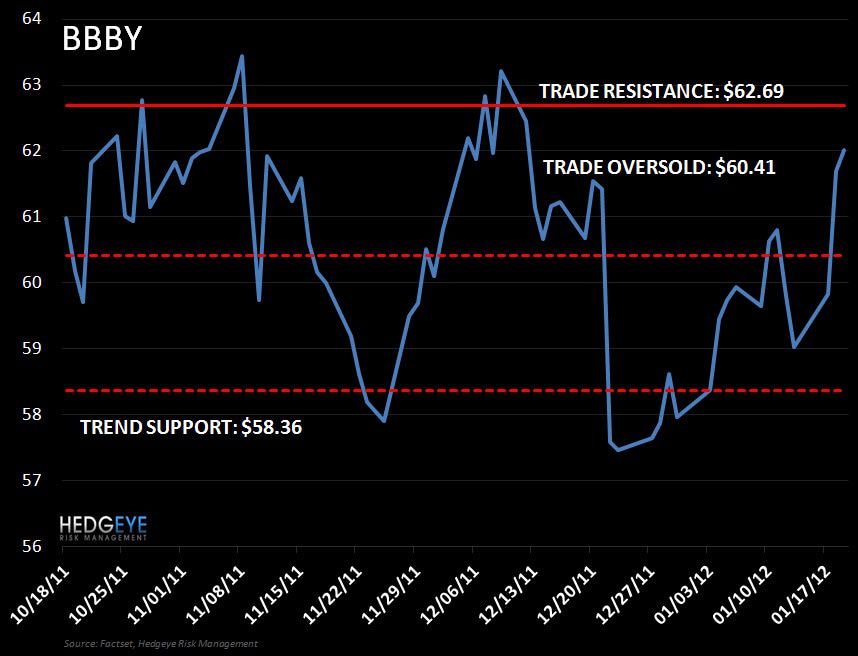

Keith just added to our BBBY short position. Lower long-term highs in one of our favorite names on the short side, Bed Bath & Beyond. After being big bulls, we’re starting to question the sustainability of longer-term market share opportunity.

Keith just added to our BBBY short position. Lower long-term highs in one of our favorite names on the short side, Bed Bath & Beyond. After being big bulls, we’re starting to question the sustainability of longer-term market share opportunity.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.