Claims Have Become an Significant 1H12 Tailwind to Bank Credit Quality and Loan Growth

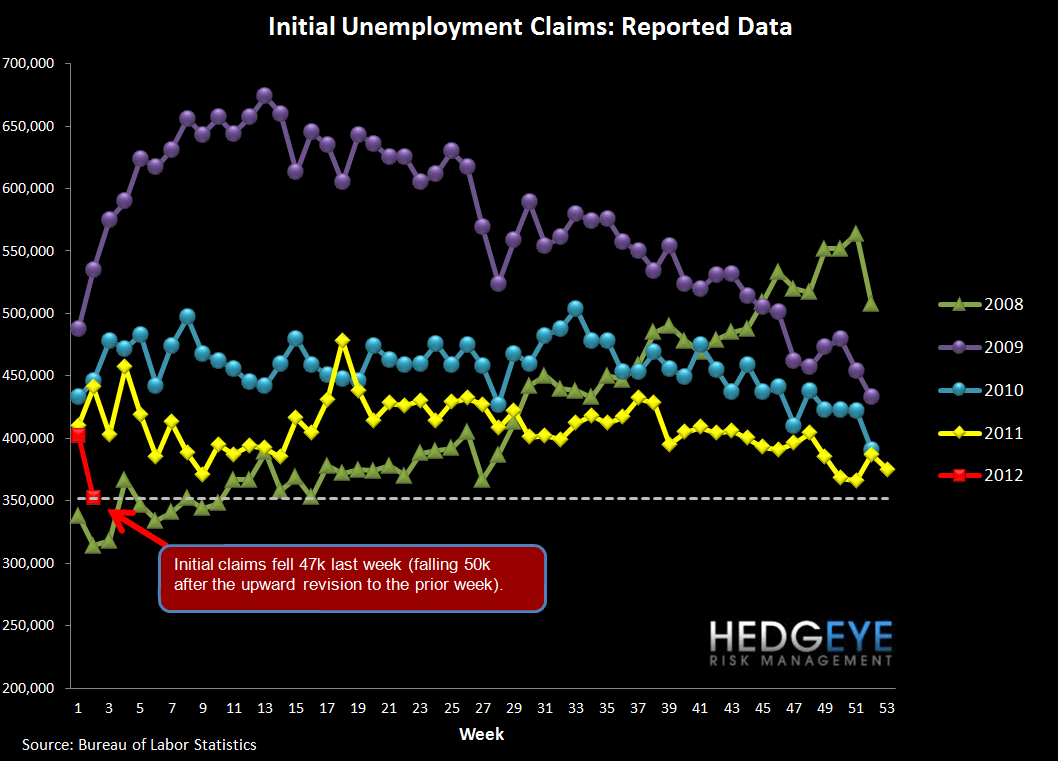

The headline initial claims number fell 47k WoW to 352k (down 50k after a 3k upward revision to last week’s data). Rolling claims fell 3.5k to 379k. On a non-seasonally-adjusted basis, reported claims fell 125k WoW to 522k. For those unfamiliar with why we publish on claims every week, it's because they're the best indicator for how credit quality and loan growth trends are likely to fare over the next six months.

This morning's claims print is obviously strong. It also flies in the face of what we've seen in the last few years: claims tend to be weak in the start of the year. After the prior week's disappointing print, this week's print seems to lay to rest concern about an imminent back up in claims. We've pointed out that claims that are sustainably below the 385-400k range foster unemployment declines. While the unemployment rate is as much about the participation rate as the number of folks with jobs, the reason we think it matters is as a signal to broader confidence. As the unemployment rate falls it signals to the average American that things are improving, and that they should feel more confident about spending. In other words, it becomes an autocorrelated virtuous cycle.

We've also pointed out that an cointegrated relationship exists between claims and the S&P500. They don't stay diverged for long. It would seem that, just like last Fall, this time around the mean-reverting instrument is again the market. Full mean reversion from the market side would imply an index level around ~1360. Alternatively, claims would need to rise to ~410k to meet the market where the market is.

2-10 Spread

The 2-10 spread tightened less than 1 bp versus last week to 167 bps as of yesterday. The ten-year bond yield also fell less than 1 bp to 190 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.