This note was originally published at 8am on January 11, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

"America should be lifted up by our desire to succeed, not dragged down by the resentment of our success."

-Mitt Romney

In what I thought was the most progressive Strong Dollar, Strong America speech I’ve heard in the last 3 years last night, Mitt Romney hammered that Red, White, and Blue point home like maybe only Obama could. Strong.

Romney was alluding to crushing the “Most Popular” (most read) story on Bloomberg yesterday titled “Gingrich Attack Film Shows Romney As Ruthless Rich.” I don’t know one person (whose financial industry expertise I respect) who considered that Bain commercial anything short of a Michael Moore production. Apparently the State that says “Live Free, Or Die” agrees.

To be clear, I’m not a Republican or a Democrat. I simply want to get this country’s economics right. Clinton should have provided as much inspiration to President Obama to balance a budget as Reagan may have inspired Romney’s great hair. When it comes to the economic policy in America, Keynesian Academic Dogma failed both Bush and Obama. It’s time for change.

Can Obama be the change that Ron Paul is with the Youth/Change Vote in this country? Yes He Can. Will he? I have no idea. He’s certainly not going to get any non-groupthink ideas on economics from Tim Geithner. As of this Romney win in New Hampshire last night, this ½ Clinton ½ Reagan race to the US Presidency is officially on.

Back to the Global Macro Grind…

Game on. I love this. I really do. I’m going to light up our 11AM EST conference call line like a Christmas tree this morning as Big Alberta and I officially roll out our Q1 Global Macro Themes for 2012.

Our clients already know what our Q1 Themes are, but if you’re new to this Canadian-American tire pumping game, here they are:

1. Strong Dollar = Strong Consumption

2. Deflating The Inflation, Part Deux

3. Growth Slowing’s Bottom

Yesterday’s breakout in US Equities confirmed a lot of what we have been signaling for the last 3-4 weeks. We’ll go through this in depth (45 slides) on our call this morning, but the data doesn’t lie – perma-bulls forced to perma-change their bullish theses do. A Sustainably Strong and Stable US Dollar provides a coincident benefit to Employment, Confidence and Consumption.

That’s the fundamental research view – our quantitative risk management view supports this fundamental shift:

- SP500 closing above its October 29th, 2011 closing high of 1285 yesterday (1292 close) puts 1363 in play

- US Equity Volatility (VIX) is already down -11.6% for 2012 YTD (bearish TRADE and TREND)

- US Equity Volume studies are starting to change (up +31% day/day on yesterday’s up move, down on down moves)

Backcheck, Forecheck, Paycheck – that’s a PRICE, VOLATILITY, and VOLUME win in my model – and my model has not changed.

People who didn’t see our team make the shift from bearish to bullish on US Equities in early 2009 are still insecurely scrambling to put me on their Top 10 People Not To Listen To List of 2012 (some journalist from the Old Wall yesterday at Marketwatch). Why? They want to (or should I say need to) put me in the perma-bear box in which they need to think.

Thinking inside of a box is no way to live. Being perma bullish or bearish doesn’t work. What works is having a repeatable process that allows you to make money in both up and down markets.

What would make me go back to bearish on US Equities?

- President Obama not engaging in the ½ Clinton ½ Reagan strategy and imposing more of what didn’t work in 2011

- Ben Bernanke implementing a QE3, stoking inflation

- Geithner convincing his cronies of some socialized “mega refi” idea for US Housing (blowing up the MBS market)

Our desire to succeed in this country is based on having prior successes. If you’ve won a few games in your life, but have not yet won a Championship, you’re not thinking about the standard of success I am. America has an opportunity to be great again.

My economic strategy message should resonate as much with Democrats as it does Republicans. Both the US Currency and Equity markets are getting fired up about change in this country. That’s what real winners in real-life do. They don’t Resent Success.

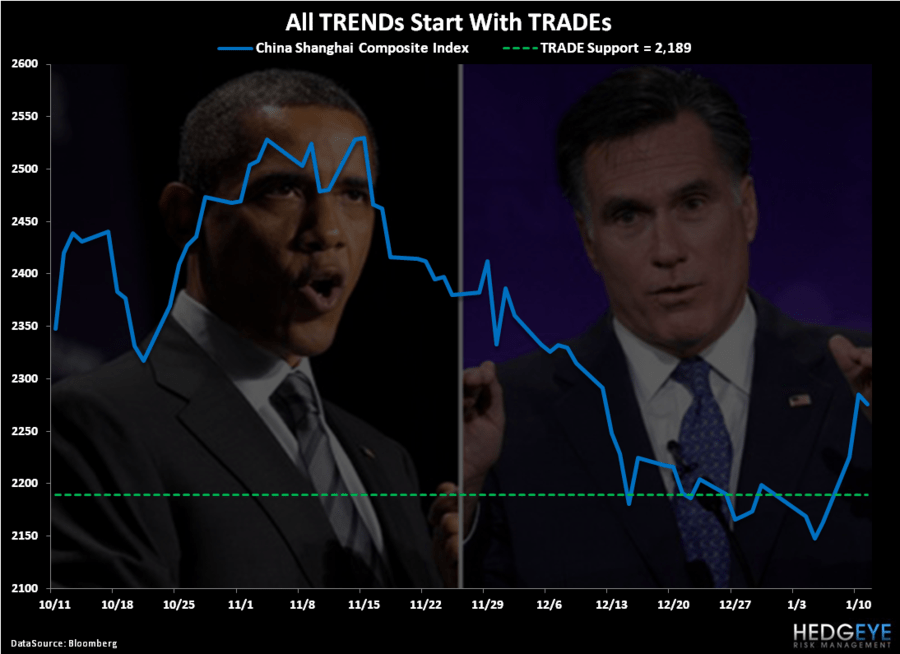

My immediate-term support and resistance lines for Gold, Oil (Brent), EUR/USD, US Dollar Index, Shanghai Composite, and the SP500 are now $1596-1655, $111.91-116.01, $1.26-1.29, $80.55-81.53, 2239-2297, and 1273-1298, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer