No Current Positions in Europe

European capital markets and the EUR-USD turned sharply this morning on rumors that Standard & Poor’s would downgrade numerous Eurozone countries today, including France. We authored a note on 10/18/11 titled “France is Going to Get Downgraded”, so today’s action by S&P to cut France’s AAA sovereign credit rating one notch to AA+ didn’t come as a huge surprise, and was well anticipated by the market over the last weeks. S&P stated, "we believe that there is at least a one-in-three chance that we could lower the rating further in 2012 or 2013."

However, as Moody’s and Fitch join the downgrading club, Eurocrats will have to answer to the AAA-rating of the EFSF, a facility built on the collateral of its largest contributors, Germany and France, at 27% and 20%, respectively. This portends that yields should rise on EFSF bond issuance going forward, which of course runs squarely counter to the purpose of this funding facility issuing “cheap” debt to ailing sovereigns. In essence, the EFSF should be downgraded to AA as well. The French Finance Minister said today’s downgrade is not a catastrophe, yet stated plainly, downgrades will increase the debt servicing costs which will put pressure on already bloated deficit and debt levels of France, and many European sovereigns like them. France in particular is running against a 90% debt to GDP ratio. Further, expect France’s downgrade to increase the already loud calls that the size and strength of the EFSF is insufficient to handle sovereign and banking bailout needs.

Announced today at 4:30pm EST, S&P placed the ratings on all but 2 of the 16 Eurozone sovereigns of negative and all 16 have been removed from creditwatch.

Summary of downgrades:

Austria to AA+/Negative from AAA/Watch Negative

Cyprus to BB+/Negative from BBB/Watch Negative (now junk)

France to AA+/Negative from AAA/Watch Negative

Italy to BBB+/Negative from A/Watch Negative

Malta to A-/Negative from A/Watch Negative

Portugal to BB/Negative from BBB-/Watch Negative (now junk)

Slovak Republic to A/Stable from A+/Watch Negative

Slovenia Republic to A+/Negative from AA-/Watch Negative

Spain to A-/Negative from AA/Watch Negative

Summary of affirmations:

Belgium AA/Negative

Estonia Republic AA-/Negative

Finland AAA/Negative

Germany AAA/Stable

Ireland BBB+/Negative

Luxembourg AAA/Negative

Netherlands AAA/Negative

Asset Class Performance:

- Equities: European indices had a mixed week largely within a tight +/- range. Top performers: Hungary 7.7%; Italy 2.5%; Cyprus 2.2%; Spain 1.9%; France 1.9%. Bottom performers: Portugal -2.1%; Slovakia -1.0%; Ukraine -1.0%; Netherlands -0.6%; Greece -0.4%

- FX: The EUR/USD -0.27% week-over-week. Divergences: PLN/EUR +1.9%, Hungarian Forint/EUR +1.31%%, Iceland Krona /EUR -0.72%

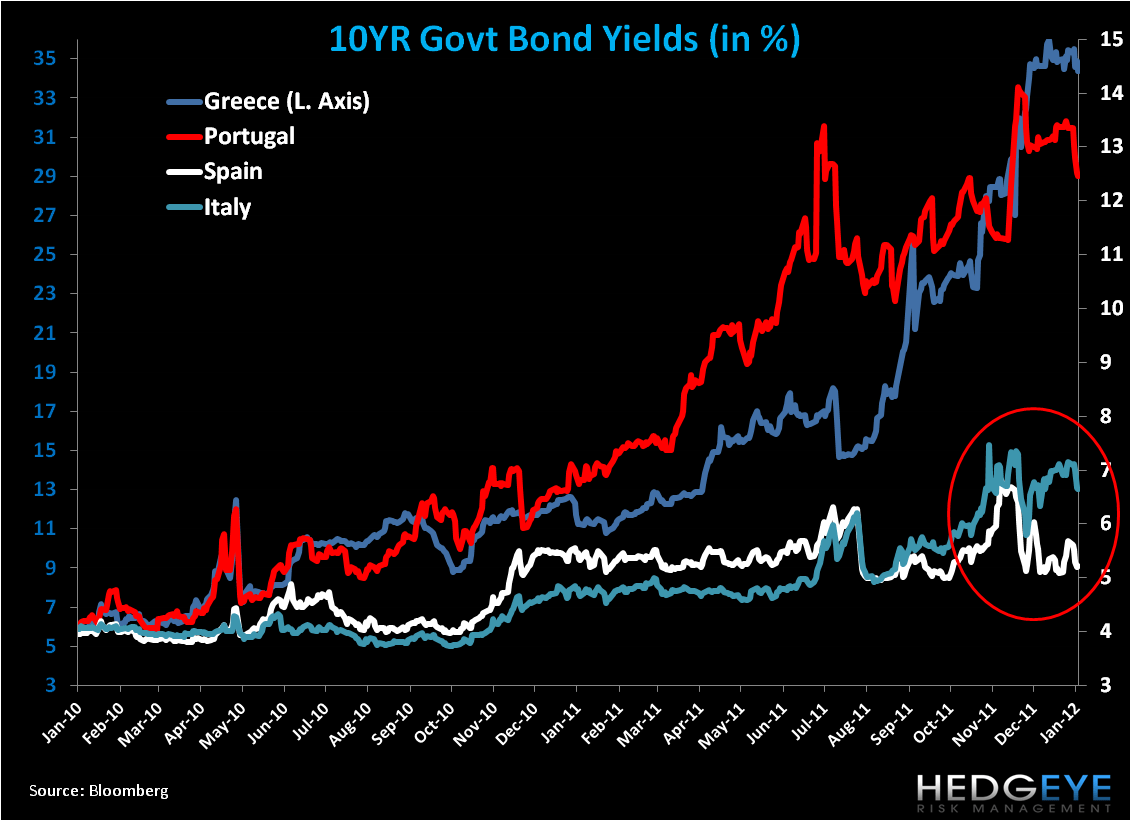

- Fixed Income: 10YR sovereign yields broadly decreased w/w, led by Greece -107bps to 34.36%; Portugal -90bps to 12.46%; Italy -50bps to 6.64%; Spain -47bps to 5.22%. In context, Italy’s 10YR was as high as 7.14% (on 1/10) this week.

Contextualizing Europe’s Standing:

What’s additive to this week’s discussion of Europe is Draghi’s positioning of the LTRO as a facility that’s helping banks buy time to improve their liquidity standing and his optimism that the credit markets are beginning to loosen on the margin. To the latter point and the naysayers, it’s suggested that the funds borrowed from the LTRO at 1.00% are simply being deposited at the ECB’s overnight facility at 0.25%, indicative of the defensive outlook of banks [to actually take a 75bps hit on the spread] and therefore the continuation of a frozen credit market. Draghi, however, stressed in the press conference following Thursday’s decision to leave main rates unchanged that the banks participating in the LTRO were not [all] the same banks that are re-depositing with the overnight facility. (For more on Draghi’s positioning see our note on 1/12 titled “ECB Press Conference Notes: Draghi Stands Strong Behind LTRO”). And in so many words he concluded that we’re beginning to see the initial signs of credit flowing.

The key risks for European markets, however, remain in two channels: the banks and sovereigns. In the Q&A of the ECB’s press conference, Draghi made some important comments on both fronts. While the ECB is not the sole leader in sorting out Europe’s fiscal imbalances (we’d argue that German Chancellor Merkel plays one of the key roles), the ability of the ECB to take leverage/debt on its balance sheet is of critical concern, and again Draghi reiterated that the EFSF is its own independent facility. In essence, the ECB will not contribute to the facility in any form, or directly aid sovereign or banks, outside of its “temporary” SMP facility to buy secondary sovereign bond issuance. [Since May 2010, the SMP has purchased 213B EUR].

While sovereigns may have some relief from the SMP program, there’s no facility to directly aid/address Europe’s banks. A good preview of potential dark clouds for banks that need to raise capital is Italy’s Unicredit. Its equity shares fell -36% last week after the bank announced a €7.5B rights offer on January 4th, equating to a market cap drop of €8B, as new equity shares were deeply discounted. Along these lines, we want to highlight that Commerzbank has a January 20thdeadline to present a credible plan to fill €5.3B capital gap. For anyone who says that risk is fully priced in on European bank stocks, we’d reference Unicredit.

As we look out over the next weeks, we think the yield and demand of new sovereign debt issuance will continue to be held under a spotlight and markets will run off headline risk. Markets may well find comfort in the LTRO to provide the needed liquidity to banks, which has been reflected in decreases in the Euribor-OIS spread over the last 10 days. While the LTRO may prevent insolvency issues in the near term by boosting liquidity, it may only mask the issues, and surely does not offer insurance that equity holders don’t get wiped in the process. Between now and the mid-year, which is the deadline for banks to meet the 9% Tier 1 capital ratio, we may see dark clouds for banks that need to raise capital. From a policy perspective, it appears Draghi may well hold interest rates unchanged until at least March to gauge the progress of the LTRO program, and the second instalment on 2/29.

Call Outs:

- Overnight deposits at the ECB continue to make higher highs (€489.9 billion).

- Fitch says that 60% PSI won’t lead to sharp reduction of debt burden. Talks resume next week.

- Germany to lower GDP outlook to 0.75% from 1.0% for 2012, according to Handelsblatt.

- Commerzbank says it does not need more government money and will present its capital plan next Friday.

- Italy sold €4.75B of debt today (€3B of 2014 bonds with an average yield of 4.83% vs 5.62% on Dec 29, but bid-to-cover was not good at 1.20 vs 1.36 prior).

- Switzerland - Thomas Jordan, 48, emerges as the frontrunner to replace Philipp Hildebrand at the SNB following a currency trading scandal with Hildebrand’s wife. Jordan must show that he can defend the 1.20 floor in the EUR-CHF, which intraday stood at 1.2081 CHF, or -0.6% w/w.

Germany (EWG)

We’re getting more constructive on Germany on recent data, however are very aware that despite Germany’s strong fiscal position (budget deficit = 1% in 2011 vs -4.3% in 2010) and employment base (Unemployment Rate = 6.8%), the country’s capital markets are not immune to the region’s sovereign and banking contagion risk. After all, German equities were down last year -20% despite a similar strong fiscal and employment position.

The DAX, like the FTSE MIB, IBEX, and CAC, looks good from an immediate term TRADE perspective. We’d buy the DAX on a pullback.

Key Regional Data This Week:

Positives (+)

Eurozone Sentix Investor Confidence -21.1 JAN vs -24.0 DEC

Germany Exports 2.5% NOV M/M (exp. 0.5%) vs -2.9% OCT

Germany Trade Balance 16.2B EUR NOV (exp. 12B EUR) vs 11.5B EUR OCT

Germany Budget Deficit (as % GDP) for 2011 = -1% versus -4.3% in 2010

Russia Trade Balance $17.4B NOV vs $16.6B OCT

UK PPI Input 8.7% DEC Y/Y vs 13.6% NOV

UK PPI Output 4.8% DEC Y/Y vs 5.4% NOV

Negatives (-)

Russia CPI 6.1% DEC Y/Y vs 5.6% NOV

Greece Unemployment Rate 18.2% OCT vs 17.5%

Interest Rate Decisions:

(1/11) Poland Base Rate Announcement UNCH at 4.50% (expected UNCH)

(1/12) BoE UNCH at 0.50%; Asset Purchase Target UNCH at 275B GBP

(1/12) ECB UNCH at 1.00%

CDS Risk Monitor:

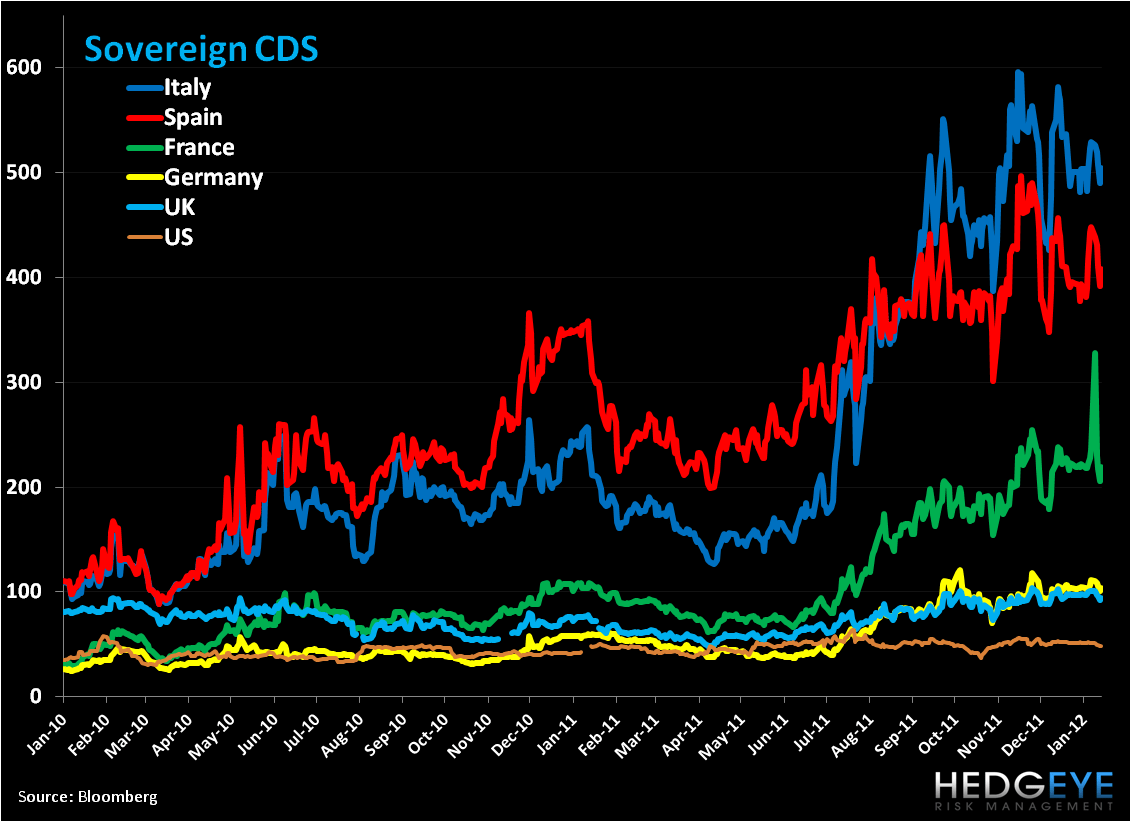

On a w/w basis, CDS was down across Europe, with a positive divergence from the periphery. Spain saw the largest decline at -40bps to 408bps; followed by Ireland -36bps to 675bps, and Portugal and Italy both down -25bps to 1088bps and 504bps, respectively.

EUR-USD

We’d short the cross at $1.28 for an immediate term TRADE. The EUR/USD remains broken long term TAIL ($1.40) and intermediate term TREND ($1.42) in our models and we think the lack of resolve from the newest proposals for a fiscal union will encourage greater downside.

The European Week Ahead:

Monday: Dec. Germany Whole Sale Price Index; Dec. UK Nationwide Consumer Confidence (Jan 16-20); Dec. Italy CPI – Final; Nov. Italy General Government Debt

Tuesday: Jan. Eurozone ZEW Survey Economic Sentiment; Dec. Eurozone CPI; Dec. UK CPI and Retail Price Index

Wednesday: Nov. Eurozone Construction Output; Dec. UK Jobless Claims Change and Claimant Count Rate; Nov. Italy Trade Balance and Current Account

Thursday: Eurozone Publishes Monthly Report; Nov. Eurozone Current Account

Friday: Germany Deadline for Commerzbank to Present Credible Plan to fill 5.3B EUR Capital Gap; Dec. Germany Producer Prices; Dec. UK Retail Sales; Nov. Italy Industrial Orders and Sales

Matthew Hedrick

Senior Analyst