Conclusion: Despite a strengthening U.S. dollar, the price of oil has not corrected. This is a function of heightened geo-political risk, maxed-out Saudi Arabian production, and the U.S. insistence on using oil as a foreign policy tool against Iran.

Many of our key investment themes, and really macro asset allocations, over the past couple of years have been related to the direction of the U.S. dollar. Specific to commodities, dollar up has consistently meant commodities down. Recently, that correlation has weakened with oil. In fact, both Brent crude and the U.S. dollar have broken into Bullish Formations on our quantitative models.

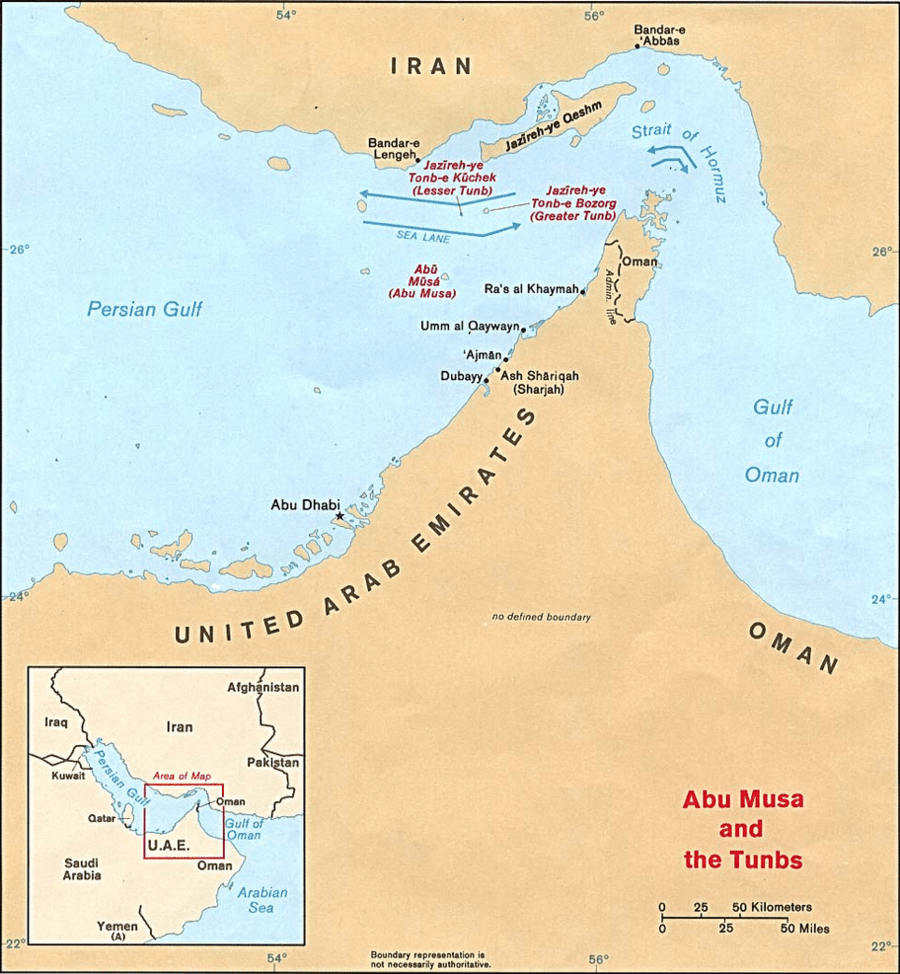

Given the recent rhetoric from Iran related to the Strait of Hormuz, the strength in the price of oil is not totally surprising. In December, Iran threatened to shut the Strait of Hormuz if sanctions were imposed on its oil exports. Subsequent to that announcement, Iran held a series of naval maneuvers over a period of ten days, ending on January 3rd, just east of the strait.

Today, the latest gauntlet was thrown down over Iranian oil. After meetings with U.S. Treasury Secretary Tim Geithner, the Japanese indicated that they intend to reduce their imports of Iranian oil, which stand at roughly 10% of their total imports. Behind China at 20%, Japan is the second largest importer of Iranian oil at approximately 17% of total Iranian exports. China, on the other hand, has been reluctant to cut its use of Iranian oil, though Premier Wen Jiabao is making his first trip to Saudi Arabia this weekend, which can be seen as an affront to Iran.

The strategic relevance of the Strait of Hormuz is that more than one-fifth of the world’s oil is transported through the strait, which is 34 miles wide at its narrowest. As oil is transported out of the Persian Gulf it passes through the Strait of Hormuz before crossing in the Arabian Sea. Every day, about 14 tankers carrying 15.5 million barrels of crude oil pass through the strait.

On “Face the Nation” this past Sunday, Joint Chiefs of Staff Chairman General Martin Dempsey was very specific in stating that the U.S. was prepared to act aggressively should Iran attempt to block the strait. General Dempsey stated:

“They’ve invested in capabilities that could, in fact, for a period of time block the Strait of Hormuz. We’ve invested in capabilities that ensure if that happens, we can defeat that.”

Defense Secretary Leon Panetta echoed these comments and also indicated that efforts by Iran to build a nuclear weapon would also constitute a “red line”, which implies potential the need for U.S. retaliation.

On the subject of nuclear weapons, according to the Iranian newspaper, Kayhan, Iran has started to enrich uranium at its Fordo production facility. The Fordo plant is built into the side of a mountain near Qom, a Muslim holy city, which is located just south of Tehran. (Ironically, the Fordo location is also believed to be the site of the largest number of fatalities in the Iran-Iraq war.) This site was disclosed in 2009 and has been at the epicenter of the debate over whether Iran is on the path to nuclear weapons, or merely using this enrichment for energy purposes. We’ve posted a satellite image of the site below.

Coincident with the strong language voice this weekend on “Meet the Press” by the Secretary of Defense and the Chairman of the Joint Chiefs of Staff, the Council on Foreign Relations publication, “Foreign Affairs”, featured an article by former Pentagon defense planner Matthew Kroenig titled, “Time to Attack Iran”. According to the article:

“But skeptics of military action fail to appreciate the true danger that a nuclear-armed Iran would pose to U.S. interests in the Middle East and beyond. And their grim forecasts assume that the cure would be worse than the disease -- that is, that the consequences of a U.S. assault on Iran would be as bad as or worse than those of Iran achieving its nuclear ambitions. But that is a faulty assumption. The truth is that a military strike intended to destroy Iran’s nuclear program, if managed carefully, could spare the region and the world a very real threat and dramatically improve the long-term national security of the United States.”

His conclusion is simply that the U.S. has little choice but to attack, and the time to do so is now.

Obviously, Kroenig’s view is more aggressive than the administration’s in terms of how to deal with Iran, and his essay shouldn’t be construed as carrying water for the administration, despite being a former advisor to the Secretary of Defense. Regardless, if the resilience of the price of oil, strong actions by the Iranians, and strong language by the Americans are telling us anything, it is that the Iranian issue is not going away in the short-term.

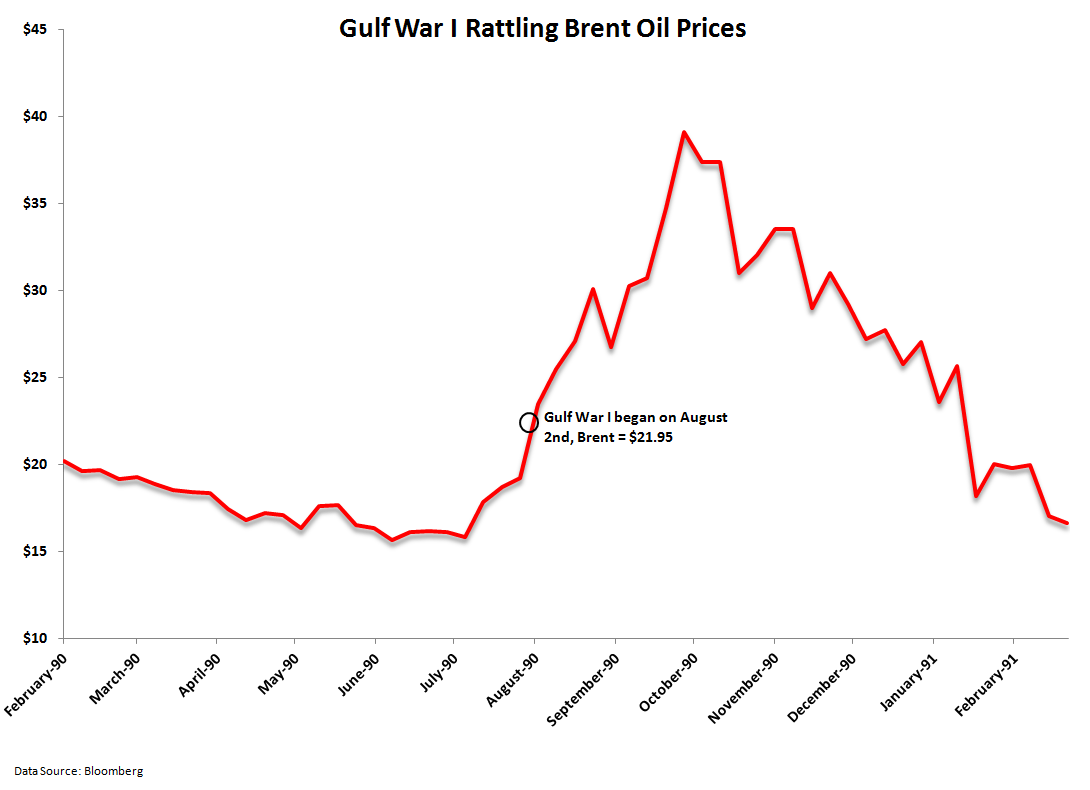

In the scenario that military action is taken against Iran, the risk management question to ponder is: what will the impact on the price of oil be? As a proxy, in the two charts below, we evaluated how the price of Brent reacted in the six months leading to Gulf Wars I and II and the six months preceding. In Gulf War I, the price of oil ran up into the event and then almost doubled as the invasion ensued, but six months later was lower than the price at the start of the war. In Gulf War II, which was slightly different given the long anticipatory period, the price of Brent actually sold off on the news and six months later was basically at the same price.

Currently, at least based on mainstream reports, an invasion of Iran is not being seriously contemplated, but rather the likely action, if any, would be a strategic strike, so it is perhaps somewhat inaccurate to compare the Gulf Wars to a potential action in Iran. Conversely, though, Iran is a much more critical player in the world oil supply. Specifically, after Saudi Arabia and Canada, Iran has the third most reserves globally, about 10% of the world’s total. As well, Iran is the third largest oil exporter after Russia and Saudi Arabia.

The heightened rhetoric relating to Iran comes at a time when Saudi Arabia is reportedly pumping close to capacity at 10 million barrels per day. This means that there is very little spare capacity in the event of either the Iranians closing, even if for a period of time, the Strait of Hormuz, or a strategic strike against Iran that shutters some of their production. Thus, we shouldn’t be surprised by the resiliency in the price of oil, particularly Brent.

Daryl G. Jones

Director of Research