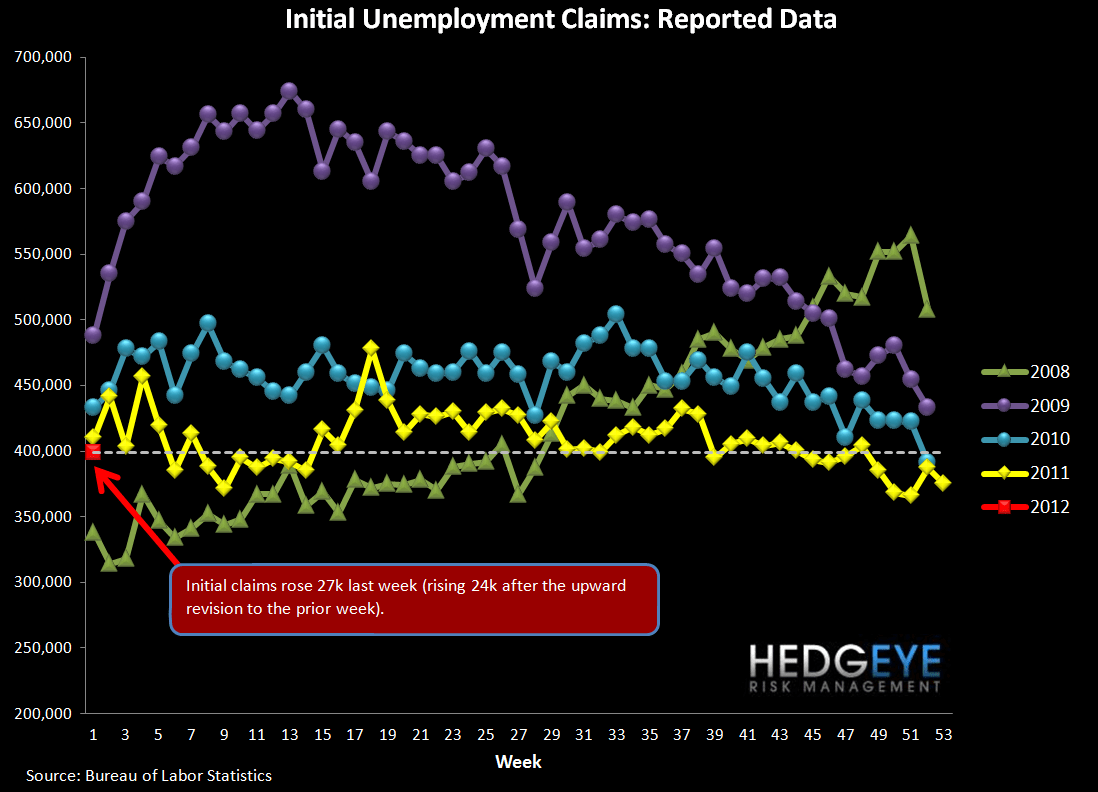

Initial Claims Rise

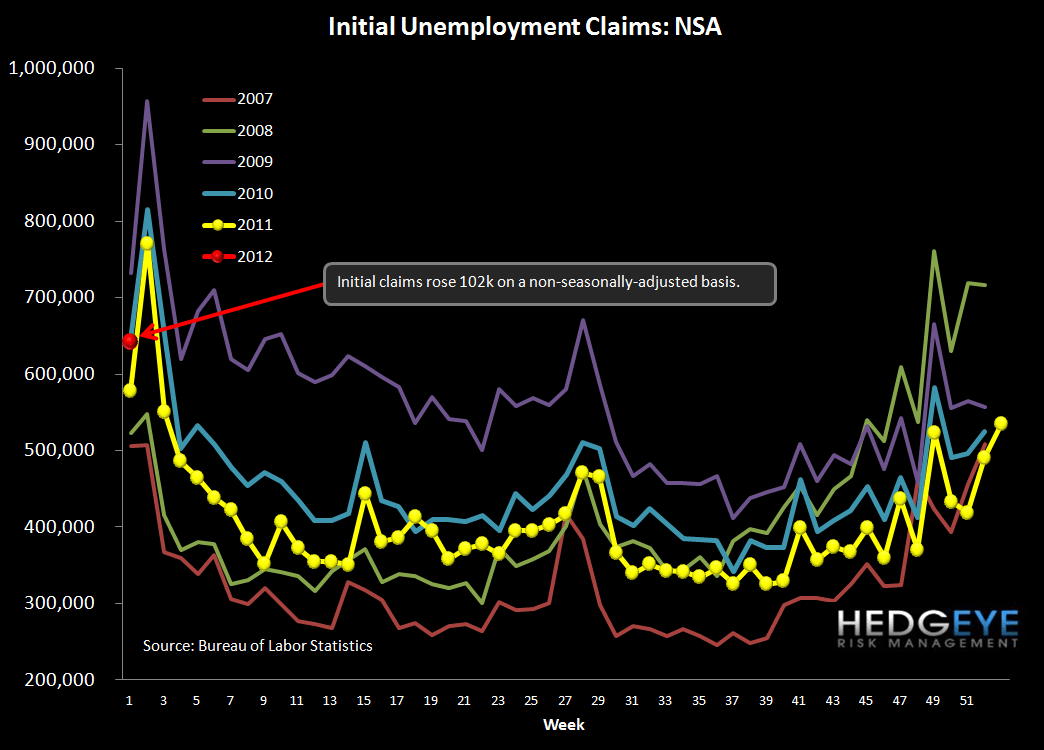

The headline initial claims number rose 27k WoW to 399k (up 24k after a 3k upward revision to last week’s data). Rolling claims rose 7.75k to 382k. On a non-seasonally-adjusted basis, reported claims rose 102k WoW to 642k.

We've pointed out that there are two very important relationships to be cognizant of when looking at claims. The first stems from the observation that claims tend to begin falling from week 36 through year-end and then reverse in the first 1-2 months of the new year. This morning's print is consistent with that trend as this was the first print of 2012. The second relationship to watch is the relationship between the the S&P and claims, as shown in our chart below. Over the last two years we've noted that these two series move in tandem and that any divergence between the two is short lived.

Full mean reversion from the claims side implies a level around 410k. Conversely, should claims stay flat and the S&P revert, our model implies that the index would need to go to ~1350 to close the gap.

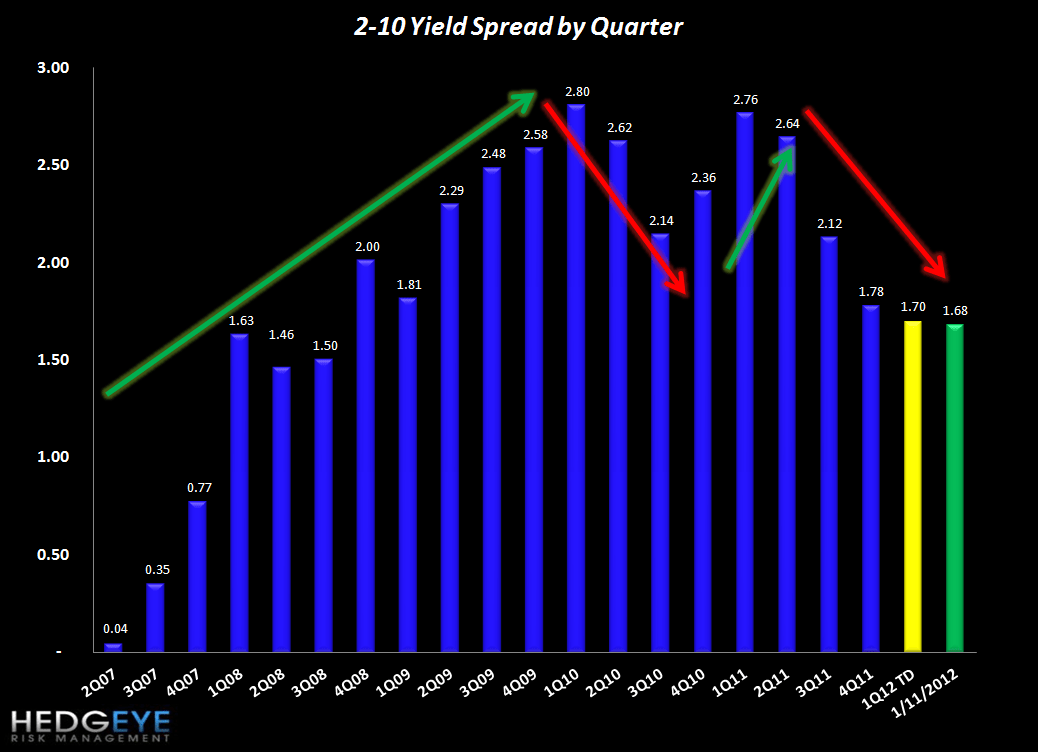

2-10 Spread

The 2-10 spread tightened 4 bps versus last week to 168 bps as of yesterday. The ten-year bond yield decreased 7 bps to 191 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.