TODAY’S S&P 500 SET-UP – January 11, 2012

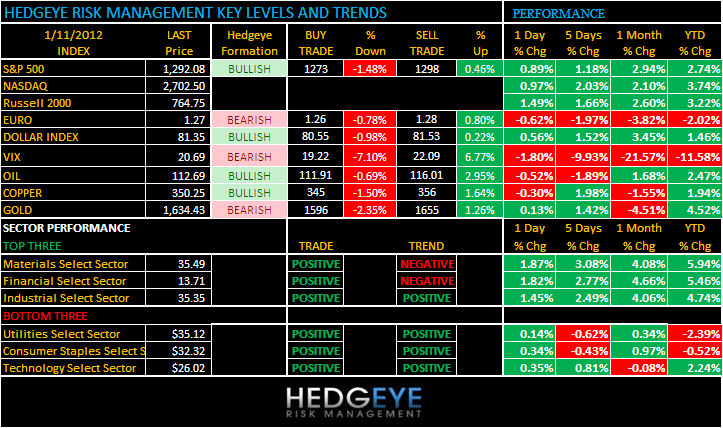

As we look at today’s set up for the S&P 500, the range is 25 points or -1.48% downside to 1273 and 0.46% upside to 1298.

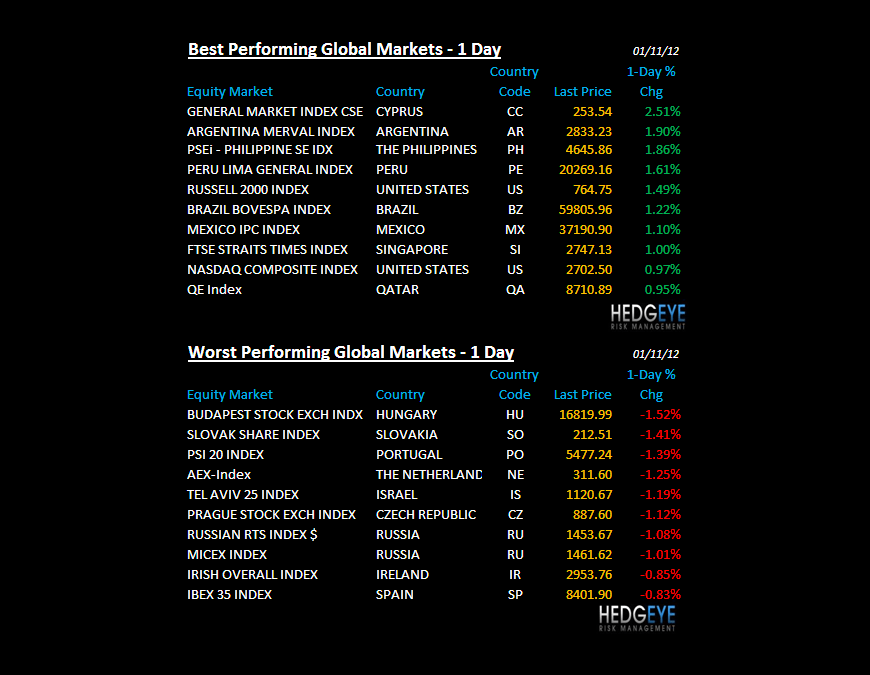

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

TREASURIES – literally the only major leading indicator in our macro model that has not yet confirmed bullish immediate-to-intermediate-term slopes of growth and inflation readings. TRADE line support for 10yr yields = 1.96% (so we’re above that), but the TREND up at 2.03% is the biggest line in the sand that has not yet been traversed. Stay tuned.

- ADVANCE/DECLINE LINE: 1633 (+821)

- VOLUME: NYSE 840.83 (16.48%)

- VIX: 20.69 -1.80% YTD PERFORMANCE: -11.58%

- SPX PUT/CALL RATIO: 1.40 from 2.03 (-31.03%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 57.44

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 1.95 from 1.98

- YIELD CURVE: 1.71 from 1.74

MACRO DATA POINTS (Bloomberg Estimates):

- 7:00am: MBA Mortgage Applications, Jan. 6 (prior -4.1%)

- 8:40am: Fed’s Evans speaks on U.S. economy in Illinois

- 9:00am: Fed’s Lockhart to speak on economy in Atlanta

- 10:30am: DoE inventories

- 12:30pm: Fed’s Plosser speaks on economy in Rochester, NY

- 1:00pm: U.S. to sell $21b 10-yr notes (reopen)

- 2:00pm: Fed’s Beige Book

WHAT TO WATCH:

- Mitt Romney wins New Hampshire primary, Ron Paul finishes second; South Carolina primary next

- Microsoft said 4Q industry PC sales will probably be lower than analyst est. on Thailand flooding

- Geithner meets with Chinese officials, encouraged by comments on growth; due to meet Japanese PM Yoshihiko Noda

- MetLife to shut its home mortgage-origination operation, costing at least $90m; most of 4,300 units employees to lose jobs

- CFTC may vote on Dodd-Frank Act proposal that would limit proprietary trading by banks, limit hedge fund investments

- CEOs of Deutsche Boerse AG, NYSE Euronext meet in NY today as they seek to overcome opposition to exchange combination

- MF Managing Director Christine Lagarde to meet with French President Sarkozy after meeting with German Chancellor Merkel yday. Merkel, Italian Prime Minister Monti give news conference ~7am ET

- Supervalu releases earnings at 8am; watch gross margin, forecast

- Lennar releases earnings at 6am; watch orders, traffic, mortgage availability

- No IPOs planned

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

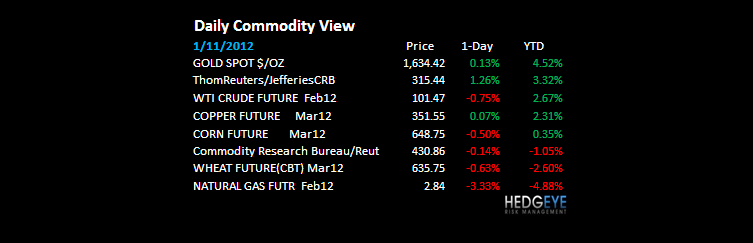

COPPER – the Doctor is in the Global Macro house this morning! Ringing the alarm clocks on the bears early (and loudly), up +1.1% isn’t the point as much as an intermediate-term TREND breakout > $3.45/lb – we’ll see if that holds (still below TAIL resist of $3.98), but Copper likes what it sees out of China all of a sudden.

- U.S. Wheat Expanding From Century Low as Glut Looms: Commodities

- Coal Set to Rebound After Worst Year Since 2005: Energy Markets

- Oil Falls From Near One-Week High After German Economy Shrinks

- China’s Gold Imports From Hong Kong Reach Record on Demand

- Soybeans Fall as Cooler Weather in South America May Help Crops

- Cocoa Retreats by 3.1% on NYSE Liffe, Erasing Earlier Gains

- Copper Trades Unchanged at $7,740 a Ton in London, Erasing Gain

- Thailand to Buy Rubber at Above-Market Rates After Protests

- Red Kite Evangelicals Reap 47% Sowing Bet on China Copper Market

- Rio, Fortescue Halt Ore Loading, Ports Shut as Cyclone Nears

- Exxon, Vitol Said to Sell Nigeria Oil Supply to Bharat Petroleum

- Russia Resumes Crude Oil Deliveries to China Via Kazakh Pipeline

- Iranian Nuclear Scientist Killed in New Attack Against Program

- COMMODITIES DAYBOOK: U.S. Wheat Acreage Expands Most in 3 Years

- Gold Climbs to 4-Week High on China Demand, Europe Debt Concerns

- Rapeseed May Advance 5.9% in Retracement: Technical Analysis

- Australian Ports Shut for Cyclone Export 41% of Global Ore Trade

CURRENCIES

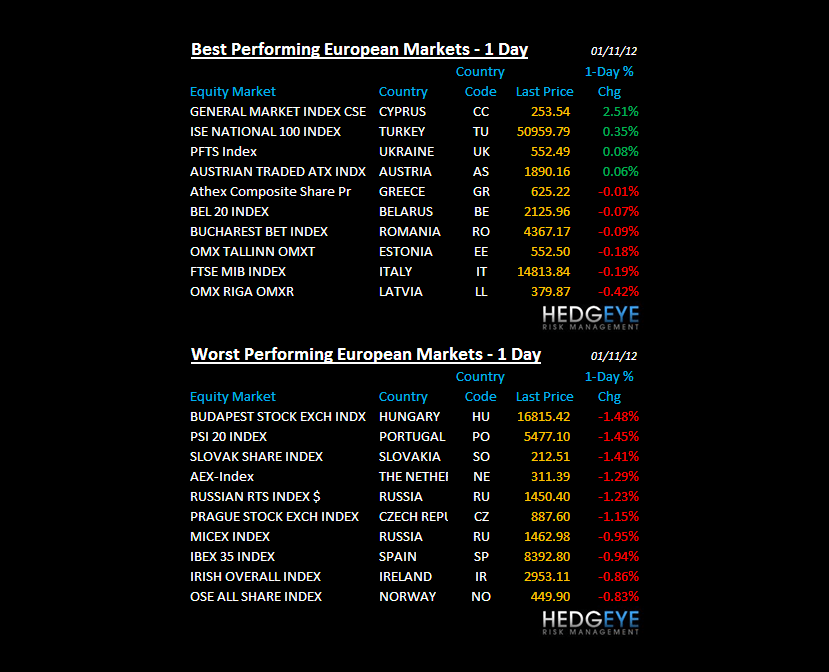

EUROPEAN MARKETS

ASIAN MARKETS

HANG SENG – in our core multi-factor model, this index carries a heavy-weight as a leading indicator – so seeing last night’s follow through buying (on volume, ahead of more Chinese data this week) is just bullish. Hang Seng +0.8% to 19,151 matters because it’s an explicit confirmation of an intermediate-term TREDN breakout > 18,616 support. China Growth Slowing at a slower pace.

MIDDLE EAST

The Hedgeye Macro Team