THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

Being Perma-Anything in Global Macro rarely works:

- CHINA – the Shanghai Composite followed up yesterday’s +2.9% gain w/ another boomer of a +2.7% move to the upside overnight, taking Chinese stocks to +3.9% for 2012 YTD. We’re long both China and Hong Kong (CAF and EWH) as we think Growth’s Bottom (a deceleration of the slowdown) may very well be happening in Q112. Bottom’s are processes, not points.

- GERMANY – both German Equities and Bunds act very well in the face of Deutsche Bank melting down. Call the Germans whatever you want to call them, but don’t call them the bailout bankers that some Americans became during our banking crisis – these guys are letting prices clear, to a degree, which is impressive. DAX up +2.1% this morn, well above 6045 TRADE line support.

- US EQUITIES – the Pain Trade is still up and that’s why I have my highest asset allocation to US Equities in a year (18%); that probably doesn’t make me bullish enough, but it’s better than the alternative – which is staying locked in w/ my 2011 Growth Slowing view. We’ll go through our US scenario for GDP growth accelerating to 2.2-2.8% (consensus = 2.1%) on tomorrow’s Macro Theme Call.

SP500’s refreshed range = 1. A close > 1285 would be very bullish as that was the closing high of October 29th.

KM

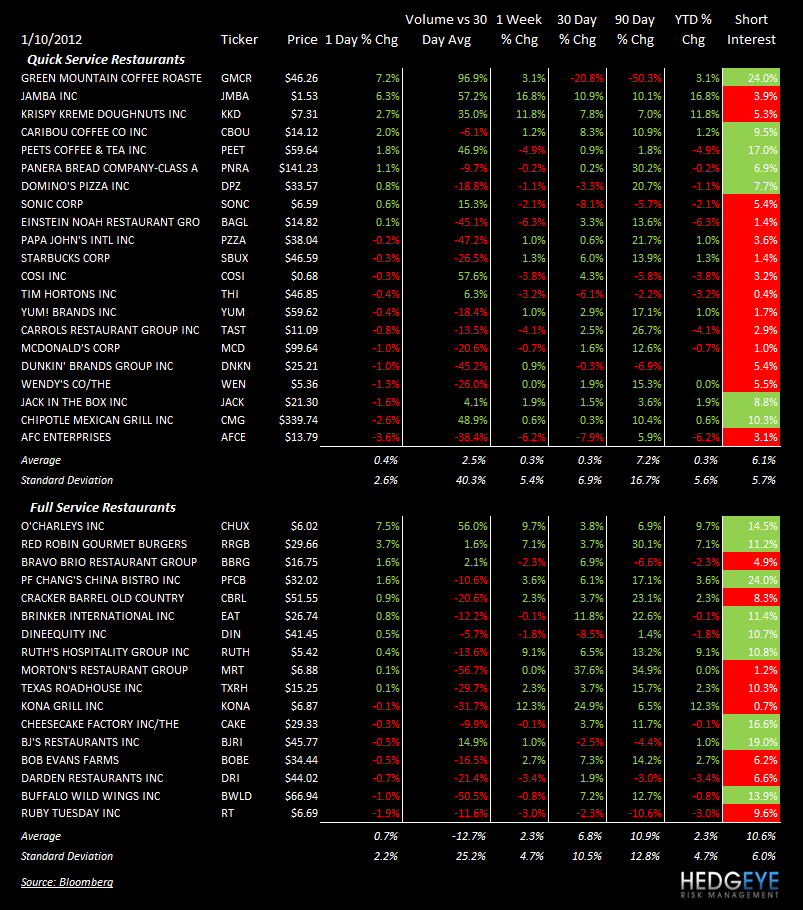

SUBSECTOR PERFORMANCE

CASUAL DINING

BJRI: BJ’s Restaurants preannounced sales ahead of this week’s ICR Xchange Conference. Comps rose +5.1% in the fourth quarter.

RT: Ruby Tuesday is looking to reverse underperforming same-store sales by increasing television advertising to drive consumers into its upgraded restaurants.

Howard Penney

Managing Director

Rory Green

Analyst