This note was originally published at 8am on January 05, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The market has its own logic and contains its own natural remedy.”

-Nicholas Wapshott

That was an excellent paraphrasing of Hayekian thought by Nicholas Wapshott in his recently published “Keynes Hayek.” But who is Hayek and what does Hayekian thought mean?

I’m going to make a concerted effort to educate our audience throughout the US Presidential Election on the answers to those very simple questions. Keynesian Dogma is pervasive in our Western education. It has also brought Japanese, European, and US governments to their knees in the last 10 years…

Good news: the young people in American who are allowed to Re-think, Re-work, and Re-build this country get that. That’s why you’re seeing a groundswell of a “young” vote for Ron Paul. It may not be as big as Obama’s was – but it’s based on the same American principle of progress – change.

To be crystal clear, this doesn’t mean I am some brainwashed disciple of Hayekian economics. It simply means that I have been educated in its alternative and have concluded (like Milton Friedman and Margaret Thatcher did) that it doesn’t work.

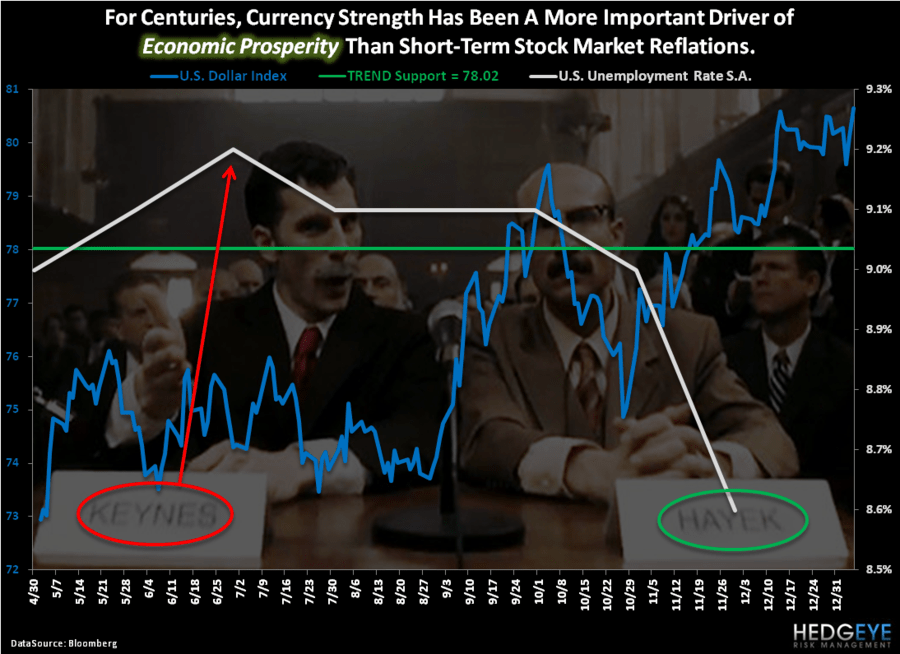

After the Keynesian experiments of the late 1920s and early 1970s ultimately failed in America, Hayekian thought became a very popular alternatives in both 1931 and 1974.

Ultimately, this is why Hayek won (shared) the Nobel Prize in Economics in 1974 and why Milton Friedman went on to become so popular in the 1970s and 1980s (Friedman won the Nobel in 1976).

Timing Matters.

Hayek: “When I was a young man, only the very old men believed in the free market system. When I was in my middle ages, I myself and nobody else believe in it. And now I have the pleasure of having lived long enough to see that the young people believe in it again.” (Keynes Hayek, pg 258)

This time, will not be different.

Back to the Global Macro Grind…

What I have enjoyed most about this stabilization of both volatility (VIX) and US stock market performance in the last few weeks is that it has been driven by the Top Natural Remedy for a country and her economy – the strength and stabilization of her currency.

With the US Dollar Index up +0.6% on the day yesterday (up +9.5% since Bernanke signaled the end of Quantitative Easing), the SP500 held flat and Consumer Discretionary stocks (we’re long XLY) closed up +0.8% on the day.

Strong Dollar = Strong Consumption. Period.

As a reminder, my solution to this mess is to get both the fiscal and monetary central planners out of the way. Big Government Spending (fiscal) will come down via The People’s vote and Easy Money Policy (monetary) that starves conservative US Savers of their hard earned fixed income will come under fire for what it’s been – a short-term policy to inflate.

Strong Dollar = Deflates The Inflation. Period.

That’s a functional reality in the Post-Keynesian economy, primarily because it’s globally interconnected. Most liquid commodity markets trade/settle on some underpinning of a US Dollar. It’s still the world’s reserve currency.

More Good News: the Correlation Risk born out of Congress and Bernanke devaluing the US Dollar to all-time lows twice (2008 and 2011) is NOT perpetual. In other words, get big fiscal and monetary “stimulus” plans out of the way and the correlations in the big stuff that matters start to burn off.

What does that mean in English? Let’s use numbers…

After having 80-90% inverse correlations to the US Dollar throughout the May-November period of 2011 (Dollar UP = Everything DOWN), here are the latest immediate-term TRADE correlations as of last night:

- Gold = -0.93

- Copper = -0.69

- CRB Commodities Index = -0.69

- EuroStoxx Index = -0.57

- US Equity Volatility = -0.57

- SP500 = -0.02

In other words, the Natural Remedy that convinces the world that we are no longer implicitly trying to devalue our currency lends credibility to the US Dollar and a lower valuations for competing currencies like the Euro and Gold.

Additionally, as the US Dollar stabilizes and strengthens:

- Commodity Inflation continues to deflate

- US Stock Market Volatility starts to fall!

- US Stocks that aren’t levered to easy money and/or debt go u

Keynesian Quacks can quibble with me about this all they want – but they’re most likely to do it behind closed doors. Like Keynes vs. Hayek in 1931 or Arthur Burns (Fed Chief) vs. Friedman in 1976, these people are very afraid of the debate – as they should be.

As the facts change, America does. Lead, follow, or get out of our way.

My immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, VIX, and the SP500 are now $1590-1639, $111.61-113.37, $1.28-1.30, 20.35-24.11, and 1267-1283, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer