Positions in Europe: Short France (EWQ)

Asset Class Performance:

- Equities: European indices were up with a negative divergence from the periphery week-over-week. Top performers: Finland 4.1%; Austria 5.0%; Russia (MICEX) 3.8%; Germany 2.7%; Sweden 2.5%. Bottom performers: Cyprus -10.4%; Hungary -5.1%; Spain -3.2%; Greece -3%; Italy -2.9%

- FX: The EUR/USD fell -1.87% week-over-week. Divergences: RUB/EUR +2.36%; CZK/EUR -1.20%, Romanian LEU/EUR -0.66%

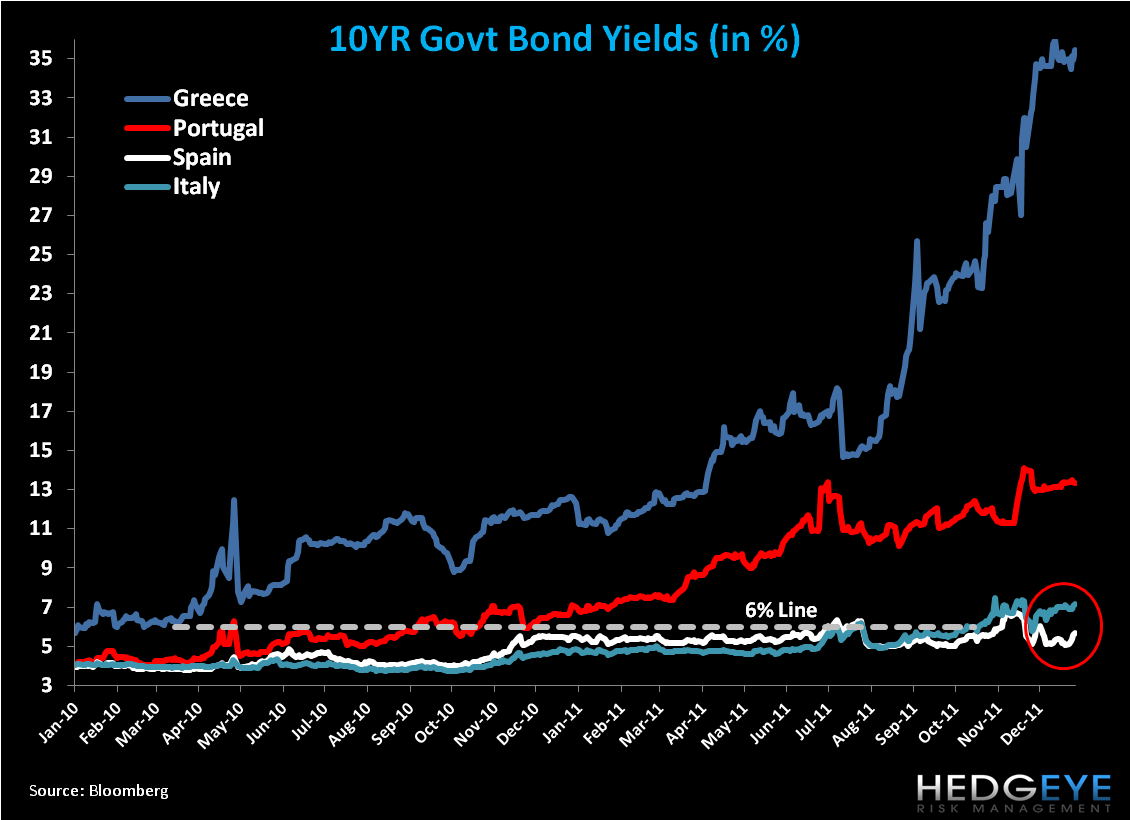

- Fixed Income: 10YR sovereign yields broadly increased w/w, led by Spain +66bps to 5.69%; Belgium +51bps to 4.60%; and Greece +47bps to 35.43%. Italy’s 10YR is now up to 7.14%!

Call Outs:

- Overnight deposits at the ECB continue to make higher highs (€455.3 Billion).

- Unicredit fell -38% this week, and its market cap has now dropped by €8 billion since the announcement of a €7.5 billion capital increase.

- Major bond auctions from Germany and France proved successful. Germany issued €4B of 10YR bonds at 1.93%, with strong demand, and France issued €8B of 10-30 year maturities with the 10YR average yield at 3.29% vs 3.18% on December 1. Yet, Italian 10YR yields closed Friday at 7.14%!

- A downgrade of France’s AAA credit rating should be priced in at this point. That said, a downgrade will force Eurocrats to answer questions on the EFSF as a AAA rated facility, and push up yields on further EFSF issuance.

- France re-engages in Financial Transaction Tax talks. Expected to make a decision by the end of January, France does not have the backing of the EU but some support from Germany and Italy, while Britain is vehemently against it. We think approval could be a huge headwind for France’s already ailing banking industry.

Charts of the Week:

-Below we show the charts of Eurozone confidence and Manufacturing and Services PMIs for the month of December. As forward looking indicators they present a mixed outlook for the region. Eurozone Confidence was largely flat to negative and the PMIs, despite a notable positive inflection month-over-month, have yet to confirm a trend. We think the shortcomings of a “fiscal union” and the lack of an adequate bazooka to ring fence sovereign and banking issues should weigh on confidence to the downside in the coming months and mute any improvements we may see in the employment and inflation picture.

Germany (EWG) - We’re getting more constructive on Germany on recent data, however are very aware that despite Germany’s strong fiscal position and employment base, the country’s capital markets are not immune to the region’s sovereign and banking contagion risk. After all, German equities were down last year -20% despite a similar strong fiscal and employment position. DAX is holding TRADE and TREND lines of support.

Key Regional Data This Week:

Positives (+)

Eurozone CPI 2.8% DEC Y/Y vs 2.9% NOV

Eurozone PPI 5.3% NOV Y/Y vs 5.5% OCT

Germany Retail Sales 0.8% NOV Y/Y (exp. 0.7%) vs -0.6% OCT

Eurozone Unemployment Rate 10.3% NOV (inline) vs 10.3% OCT

Negatives (-)

Germany Factory Orders -4.3% NOV Y/Y (exp. -1.2%) vs 5.2% OCT [-4.8% NOV M/M (exp. -1.8%) vs 5.0% OCT]

Eurozone Retail Sales -2.5% NOV Y/Y (exp. -0.9%) vs -0.7% OCT [-0.8% NOV M/M (exp. -0.4%) vs 0.1% OCT]

ECB Meeting Preview: On Hold

On Thursday January 12th the ECB convenes to announce its main interest rates. We expect the ECB to be on pause given the actions it took at the last meeting in December, namely the 25bps cut to the main interest rate to 1.00%, issuance of the 36 month LTRO, and reduction in the required reserve ratio from 2% to 1%.

We do expect macro fundamentals to deteriorate in 2012, which will warrant further cuts, however we expect the committee to give pause to review the impact of the measures taken in December. Headline inflation has moderated, which is favorable to the committee’s 2% target in 2012. We expect the ECB’s SMP facility to remain critical to fill sovereign demand and dampen yields and funding conditions to remain tight across banks.

Interest Rate Decisions:

(1/5) Romania Interest Rate CUT 25bps to 5.75%

CDS Risk Monitor:

-On a w/w basis, CDS was largely up across the Europe, with a positive divergence from the periphery. Spain saw the largest gain at +55bps to 448bps, followed by Italy +26bps to 529bps, and Portugal +23bps to 1,113bps.

EUR-USD

-We’d short the cross at $1.31 for an immediate term TRADE. The EUR/USD remains broken long term TAIL ($1.40) and intermediate term TREND ($1.42) in our models and we think the lack of resolve from the newest proposals for a fiscal union will encourage greater downside.

The European Week Ahead:

Monday: Franco-German Summit in Berlin. Jan. Eurozone Sentix Investor Confidence; Nov. Germany Current Account, Trade Balance and Industrial Production; Dec. UK House Prices (Jan 9-13)

Tuesday: Dec. UK BRC Shop Price Index; Dec. France Business Sentiment; Nov. France Manufacturing and Industrial Production; Q4 Russia Consumer Confidence (Jan 10-13)

Wednesday: Hungarian President meets with the IMF in Washington to discuss loans. 2011 Germany Budget and GDP; Dec. Germany Consumer Price Index; Q3 Italy Deficit to GDP; Jan. Russia Weekly CPI; Nov. UK Trade Balance

Thursday: Eurozone Announces Rates; Nov. Eurozone Industrial Production; Dec. Germany Consumer Price Index – Final; UK Announces Rates; Dec. UK NIESR GDP Estimate; Nov. UK Industrial and Manufacturing Production; Dec. France Consumer Price Index

Friday: Nov. Eurozone Trade Balance; Dec. UK PPI Input and Output; Dec. Spain Consumer Price Index – Final; Jan. Russia Money Supply

Matthew Hedrick

Senior Analyst