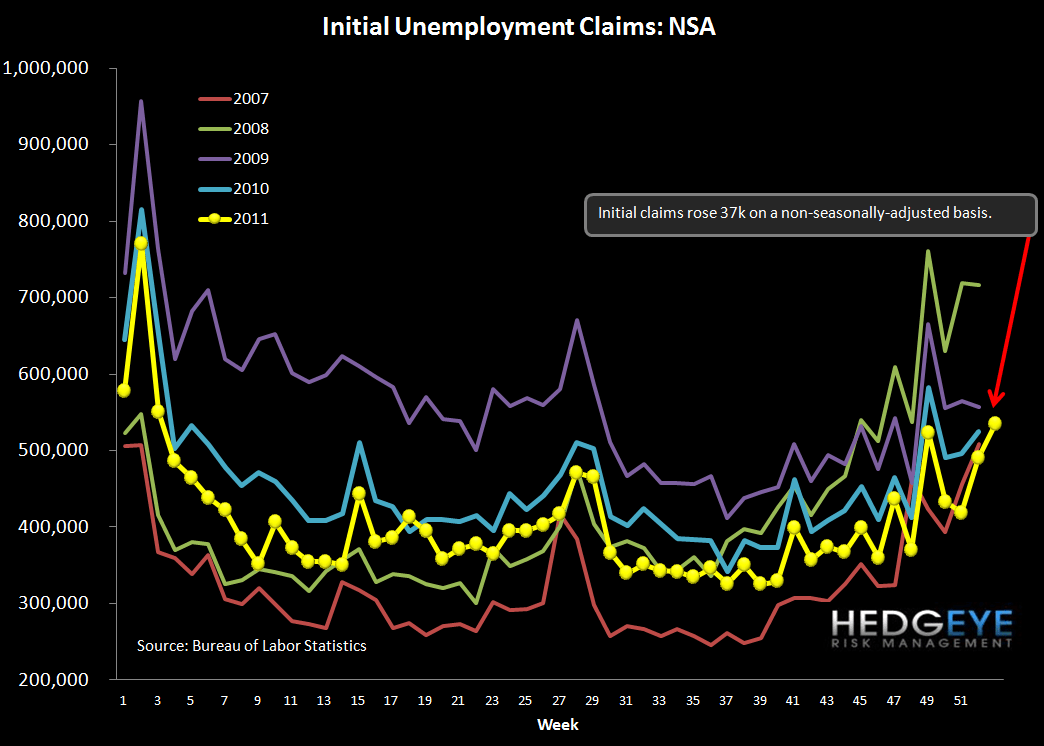

Initial Claims: Closing Out the Year on a Positive Note

The headline initial claims number fell 9k WoW to 372k (down 15k after a 6k upward revision to last week’s data). Rolling claims fell 3.25k to 373k. On a non-seasonally-adjusted basis, reported claims rose 37k WoW to 535k.

We've pointed out for the last several weeks that in the last two years claims have shown a tailwind from week 36 through year-end, and then tend to reverse that trend in the opening 1-2 months of the new year. This morning's print is consistent with that trend as this was the last print of 2011 (it reflects claims through 12/31/11). That said, the larger, secular trend in place at the moment is ongoing improvement in claims. This is obviously a tailwind for lenders from a delinquency standpoint. That said, it will be dwarfed by the elimination of reserve release that will rear its head in 4Q earnings when companies start reporting in two weeks. We often look at Discover as a leading indicator on this front as they're an off-cycle reporter (November fiscal year-end). Discover's quarter told the tale quite clearly. Although they beat estimates and generally reported solid metrics, the optical sequential slowdown driven by the absence of reserve release led the stock to get sold. Don't be surprised when the impact is far greater at the big banks.

We'd also highlight the sizeable divergence that has emerged between claims and the S&P. Historically these divergences have not persisted. Right now the divergence is suggesting that either claims back up to ~425k or the S&P 500 puts on a move to ~1390. Last time a comparable divergence emerged it was in the Fall of 2011. The mean reversion instrument at that time was the market, as claims showed resilience, and, ultimately, improvement.

As a final point, for those astute observers who notice a 53rd week in our charts below, we're not crazy. There are, in fact, 52.14 weeks per year (365/7) which means that every 7 years there is an extra week in the year. We've selected this year (2011) to be that 53-week year simply because it ended on 12/31/11.

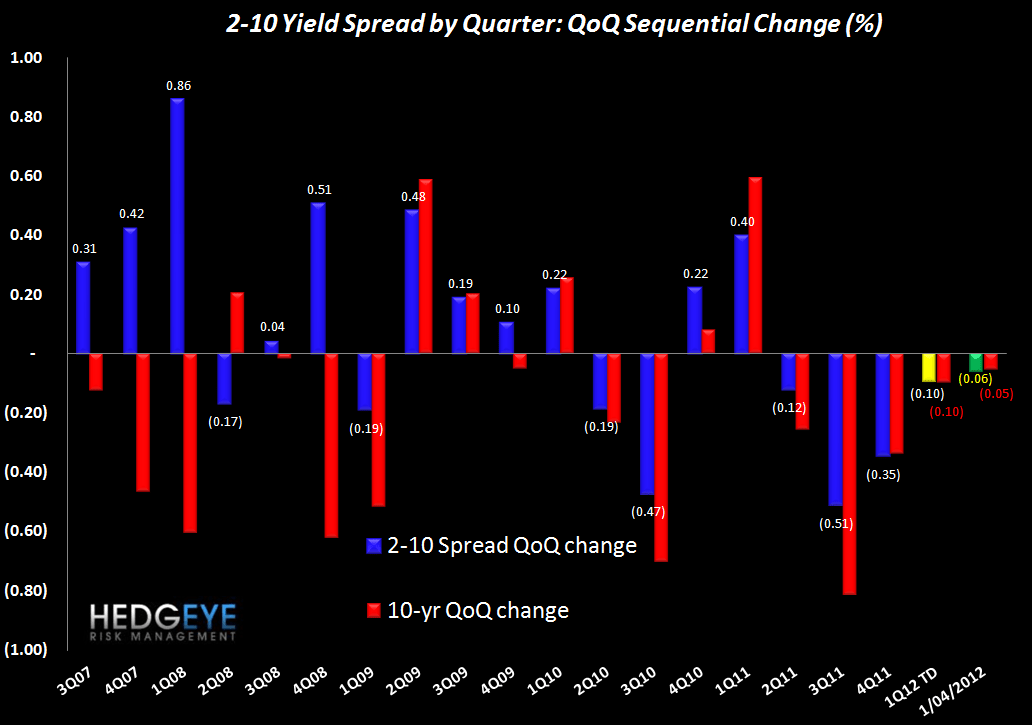

2-10 Spread

The 2-10 spread widened 7 bps versus last week to 172 bps as of yesterday. The ten-year bond yield increased 6 bps to 198 bps.

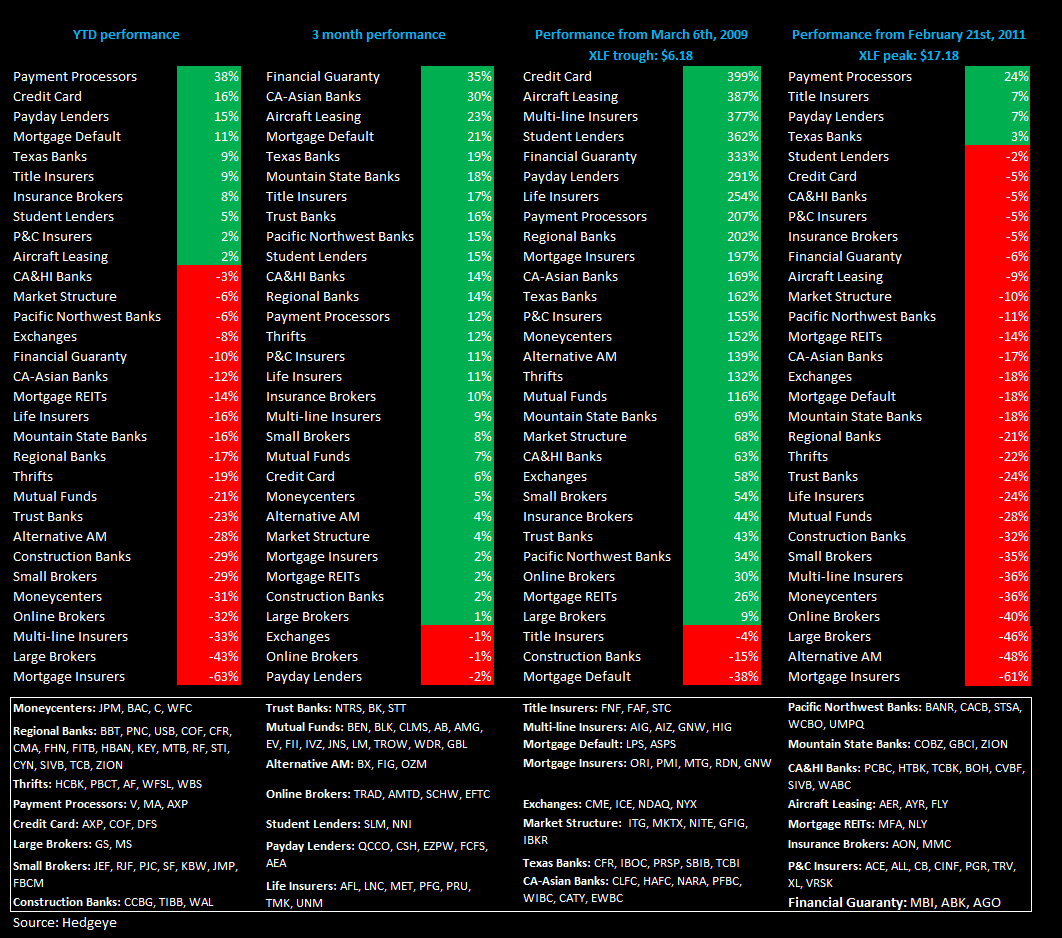

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.