Positions in Europe: Short France (EWQ)

Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor".

If you'd like to receive the work of the Financials team or request a trial please email .

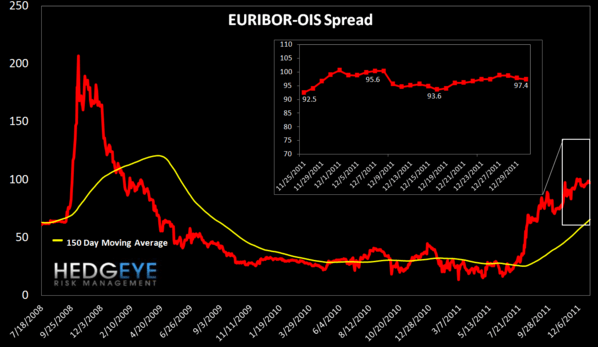

We’d note that the TED spread declined by one basis point (57.1 bps) vs. last week's value of 58.1 bps, however we're hesitant to read much into this as it is essentially unchanged and reflected a quiet week. Euribor/OIS showed similar trends with that metric coming in at 97.4 bps this week vs. 97.3 bps last week.

The most current data from the ECB’s SMP shows €19 MM in secondary sovereign bond buying in the week ended 12/23, the smallest amount in nearly five months since the ECB resumed buying in early August. In the week ended 12/16, the ECB bought €3.361B. We continue to maintain that while the SMP and the extension of the LTROs should be additive to capital market gains, we don’t see the programs carrying sustained gains over the intermediate term for European capital markets. Italian 10YR yields, which reached 6.95% today, are but one indicator of this opinion.

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by less than 1 bp to 97 bps.

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. The ECB pays lower rates than the market, so an increase in this metric demonstrates increased perceived counterparty risk and liquidity hoarding. The Liquidity Recourse hit a new all time high on Tuesday but has since fallen.

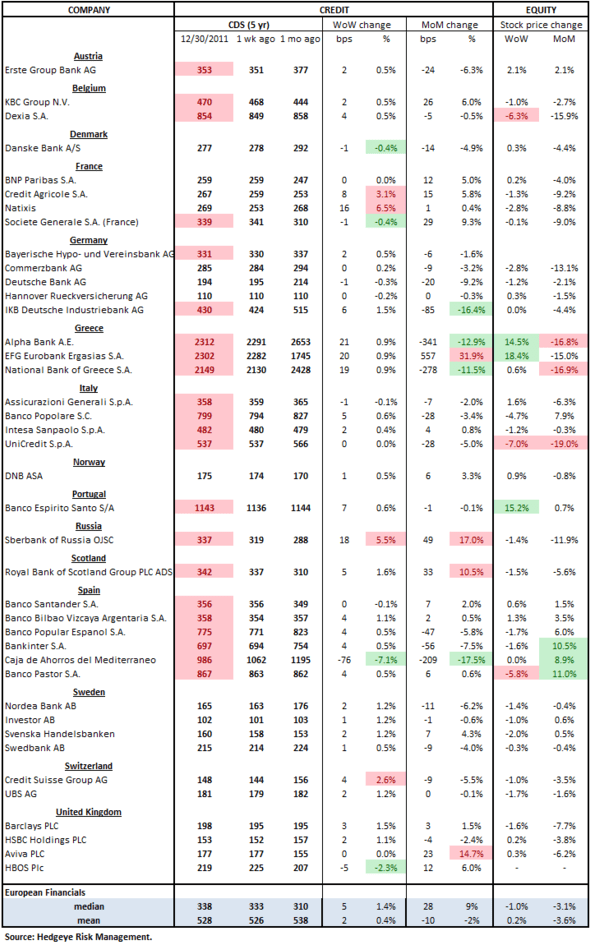

European Financials CDS Monitor – Bank swaps were wider in Europe last week for 30 of the 40 reference entities. The average widening was 0.4% and the median widening was 1.4%.

Security Market Program – The ECB's secondary sovereign bond purchasing program bought €19 MM in the week ended 12/23 vs €3.361 Billion in the week prior to take the total program to €211.0 Billion. No data has been released for the week ended 12/30.

Matthew Hedrick

Senior Analyst