“A wise man proportions his beliefs to the evidence.”

-David Hume

If there’s one thing that Hume, Hayek, and Hedgeye may have had in common, it’s that free-market pricing bears evidence of the truth. That’s my 2012 Global Macro Strategy - Believe The Evidence.

For Global Macro investors managing risk across asset classes in 2011, evidently US Treasuries outperformed mostly everything else. With Global Growth Slowing and the 10-year UST Yield dropping -43% on the year (from 3.31% to 1.88%), America’s long-bond zoomed higher as the MSCI All-World Stock Index and the 19 component CRB Commodities Index dropped -7.2% and -8.1% respectively.

In the USA, primarily due to a +9.9% rally in the US Dollar Index (from testing a 30 year low post QE2), the last 8 months of 2011 were very different from the first 4 months of 2011. While US Dollar strength may have been what Keynesians fear-mongered as a “deflationary force” on certain stock and commodity market prices, it provided the tail-wind needed for the largest part of the US Economy – Consumption.

Believe The Evidence: C + I + G (EX – IM) = GDP. And 71% of the US GDP number comes from the C, Consumption.

From a Q1 of 2011 low of 0.36% US GDP growth (and an unemployment high of 9.2%), US GDP growth recovered to 2.0% by Q3 of 2011 (and unemployment fell to 8.6%). *Note to Bernanke: stay out of the way, it’s working.

Therefore, the most contrarian bullish call we can make on US GDP Growth in 2012 is that the US Dollar continues to strengthen. Not to be confused with what the US stock market or commodity markets do, employment and economic growth is what really matters. Any sniff of a QE3 implementation will drive inflation higher and stymie whatever real (adjusted for inflation) growth Americans can look forward to.

Back to the Global Macro Grind…

With 13 consecutive booked gains in the Hedgeye Portfolio into the final day of the 2011, I’m feeling as good as I can feel about our risk management process. The goal in December was neither being bearish or bullish – it was simply to keep moving as prices did and to be right.

Rather than give you a reckless wire-to-wire “2012 Outlook” call this morning, I’ll give you our positioning (Hedgeye Asset Allocation Model):

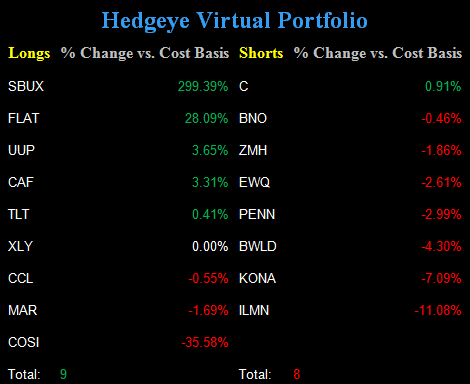

- Cash = 61% (down from 70% before last week’s Global Equity and Commodity selloff)

- Fixed Income = 18% (Long-term Treasuries and a Treasury Flattener – TLT and FLAT)

- Int’l Currency = 12% (US Dollar – UUP)

- US Equities = 6% (Consumer Discretionary – XLY)

- Int’l Equities = 3% (China – CAF)

- Commodities = 0%

FYI: I haven’t worked alongside or know one top performing Portfolio Manager from the 2008-2011 period that deals with his or her Portfolio Strategy on a trivial duration of exactly 12 months starting January 1st.

Leading Portfolio Managers of the Wall Street 2.0 era have learned to be:

- Multi-duration

- Multi-factor

As the evidence changes, they do.

Absorbing all that’s new in my trusty notebook this morning, here’s how I think about the evidence in market pricing related to our aforementioned positioning:

1. TLT and FLAT: Whether I look at the Bloomberg Consensus US GDP estimates or the 10-year trading at 1.94% this morning, it’s all signaling the same thing to me again this morning. Consensus has finally appropriately priced in the 2011 Growth Slowdown and now we can deal with Growth’s Pricing Signals day-to-day. A breakout > 2.03% on 10-year yields would have me sell TLT and FLAT.

2. UUP: Strong Dollar = Strong Consumption = Stronger Employment. Rinse and Repeat. Whoever (Obama or his Republican challenger) figures this basic economic relationship out in 2012 is going to have a good shot at becoming the next President of the United States. US Dollar Index is in a Bullish Formation with its first line of immediate-term support = $79.37.

3. XLY: There should be no confusion as to why I had a 0% asset allocation to US Equities in either July of 2008 or July of 2011. I fundamentally Believe The Evidence that debauching the dollar kills US Consumption (and confidence). Strengthen and stabilize the currency of a country and the volatility of its economic cycle (and how markets price it) will break down; equities then break-out.

4. CAF: Pardon? Yep. TimeStamp us as being long Chinese Equities as of 3:19PM on December 29th, 2011. Call us the scions of “valuation” intellect buying a legitimately “cheap” Global Equity market or just call us names, we’ll either not sell this position for a few years or we’ll sell it tomorrow and smile either way. Strong Dollar = Deflating The Inflation (bullish for Chinese Consumption).

5. COMMODITIES: Zero means zero. With the Gold price up for 11 consecutive years and Oil prices up for the last 3 in a row, I have zero problem calling a 0% asset allocation to this asset class as contrarian right here and now.

While Cyprus, Greece, and Egypt seeing their stock markets evaporate on the order of -72%, -52%, and -49%, respectively in 2011 has our eyes open to “value” opportunities outside of Chinese Equities, this morning there’s reason to believe that cheap can get cheaper. Poor Cyprus is down -4% to start 2012, and I’m going to Believe The Evidence rather than believing I’m smarter than Mr. Macro Market.

My immediate-term support and resistance ranges for Gold (covered our short position last week), Oil (Brent), and the SP500 are now $1, $107.86-110.26, and 1, respectively.

Best of luck out there this year,

KM

Keith R. McCullough

Chief Executive Officer