TODAY’S S&P 500 SET-UP – January 3, 2012

SQUEEZE – in both Asian and European Equity squeezage (yesterday + today) there actually was some economic data supporting it; China (which I bought on last day of 2011) printed a 50.3 on its PMI for DEC and Germany’s unemployment rate dropped in DEC to 6.8% vs 6.9% last month, with both economies proving you don’t need Keynesian fear-mongering to generate a solid employment base - KM

As we look at today’s set up for the S&P 500, the range is 21 points or -0.68% downside to 1249 and 0.99% upside to 1270.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -154 (-1893)

- VOLUME: NYSE 588.05 (10%)

- VIX: 22.40 +3.31% YTD PERFORMANCE: N/M

- SPX PUT/CALL RATIO: 1.49 from 2.80 (-46.77%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 57.80

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.03 from 1.97

- YIELD CURVE: 1.89 from 1.91

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- 10:00am, Construction Spending, Nov., est. 0.5% (prior 0.8%)

- 10:00am, ISM Manufacturing, Dec., est. 53.2 (prior 52.7)

- 11:30am: U.S. selling $29b 3-month bills, $27b 6-month bills

- 2:00pm, FOMC Minutes

- UK Dec Manufacturing PMI 49.6 vs consensus 47.4 and prior revised to 47.7 from 47.6

- Germany Dec Unemployment Rate sa +6.8% vs consensus +6.9% prior +6.9%

- Germany Dec Unemployment Change sa (22K) vs consensus (10k) prior (20k)

- China December PMI 50.3 vs 49.0 seq.

WHAT TO WATCH:

- Mitt Romney vying with Rick Santorum, Ron Paul for top spot in Iowa caucuses; other rivals may see campaigns end

- French President Nicolas Sarkozy to meet with German Chancellor Angela Merkel in Berlin Jan. 9

- EU says no decision has been made yet on financial assistance to Hungary -- wires

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COMMODITIES – as important to watch as European equities as they test their TAIL lines of resistance in early 2012 will be Copper and Oil testing their TAIL lines of resistance of $111.61 (brent) and $3.99/lb, respectively.

- Global Growth Slows to 3.9% as O’Neill Sees Aging Labor in BRICs

- BP Seeks Recovery of All Gulf Spill Costs From Halliburton

- Hedge Funds Raise Bullish Bets by Most in 16 Months: Commodities

- Biggest Hedge Fund in Ships Sees Frozen Gas Beating Oil: Freight

- Crude Advances Amid Manufacturing Expansion, Tension Over Iran

- Gas Bears Trim Short Bets as Prices Dip Below $3: Energy Markets

- Gold Advances as Iranian Nuclear Concern Increases Haven Demand

- Chile’s Codelco Exercises Buy Option on Anglo Copper Unit

- Copper Paces Advance in Metals as China’s Output Boosts Outlook

- Iron Ore Prices May Average 11% Lower in 2012, IG Markets Says

- Australian Manufacturing Shows First Expansion in Six Months

- Caterpillar, Rio Lock Out Canada Workers as Contract Talks Fail

- Mewah Invests in Indonesia Refinery to Diversify, CFO Says

- Polyus Leads Gain as Oil Rises for Third Year: Russia Overnight

- Sugar Mills in India Seek Time to Export as Surplus Cools Demand

- Copper Rises as Manufacturing Gauges May Signal Stronger Demand

- Lee Says ‘New Era’ Possible After N. Korea Calls Him Traitor

- S. Korean Agency to Boost Metals Buying 47% to $461 Million

- CDS Dealers to Judge If Sino-Forest in ‘Credit Event,’ ISDA Says

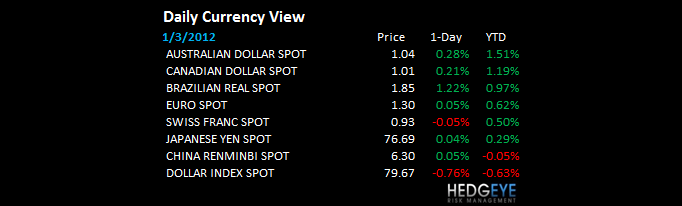

CURRENCIES

EUR/USD – get the US Dollar’s daily direction right and you’ll get most things beta right; that’s not a perpetual correlation, but it certainly still matters this morning. Euro’s new TRADE range = 1.28-1.31, so we’re dead cat bouncing this thing right back up to the top end of the range and Gold (which has a stunning -0.91% inverse cor to USD right now) pops for a +1.5% gain (covered our GLD short at $1538/oz)

EUROPEAN MARKETS

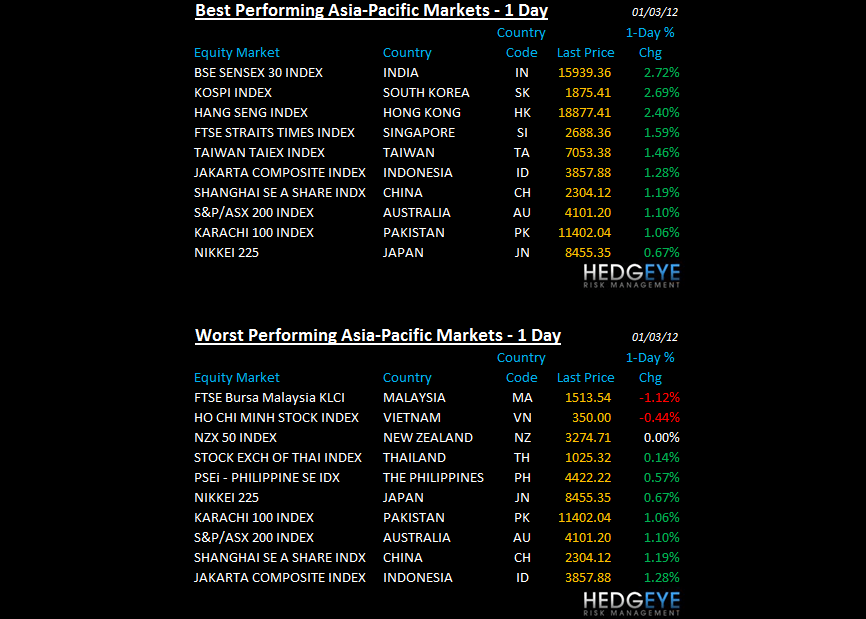

ASIAN MARKETS

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Global Growth Slows to 3.9% as O’Neill Sees Aging Labor in BRICs

- Biggest Hedge Fund in Ships Sees Frozen Gas Beating Oil: Freight

- Crude Advances Amid Manufacturing Expansion, Tension Over Iran

- Aldar Soars on $4.6 Billion Abu Dhabi Bailout: Islamic Finance

- Iran Warns U.S. Against Sending Aircraft Carrier Back to Gulf

- Gold Advances as Iranian Nuclear Concern Increases Haven Demand

- Egypt Holds Final Round of Vote as Mubarak Faces Prosecutors

- Dana Gas Bond Yield Jumps Most in Two Weeks Ahead of Meeting

- Blackwater Is Back as U.S. Spending to Hit $8 Billion in Iraq

- Gold Climbs to One-Week High as Iran Makes Nuclear Rod

- Crude Advances Amid Manufacturing Expansion, Tension Over Iran

- Banque Saudi Fransi Seeks to Raise Capital 25% Via Bonus Shares

- U.A.E. Interbank Rate Reaches 5-Month High as Loans Top Deposits

- Dubai Plan to Halve 2012 Deficit Urges Bond Upturn: Arab Credit

- Dana Board to Discuss Egypt, U.A.E. Project Financing on Jan. 4

- Iran Military Warns US Aircraft Carrier to Stay Away From Persian Gulf

- Iran military warns US aircraft carrier away from Gulf

- Greece Looking For Alternatives to Iranian Oil, Kathimerini Says

The Hedgeye Macro Team

Howard Penney

Managing Director