WMT continues to be one of our favorites on the long side as the Hedgeye Macro team maintains a bullish outlook on the US dollar and consumer discretionary into 2012.

Though it is near-term TRADE overbought, we continue to like WMT over the TREND and TAIL durations for the following reasons…

1) US business is inflecting after years of investing to turn the cruise ship. This is partially apparent in WMT outperforming peers this holiday -- in part due to layaway plan, but also due to better alignment outside of consumables.

2) Great play on stronger dollar heading into 2012.

3) Street estimates are low next year by 3-4%. Not huge, but meaningful for WMT.

4) Though not really 'new' is share repo is a part of many investors' thesis, the fact is that the Walton Family is slowly but surely taking the company private.

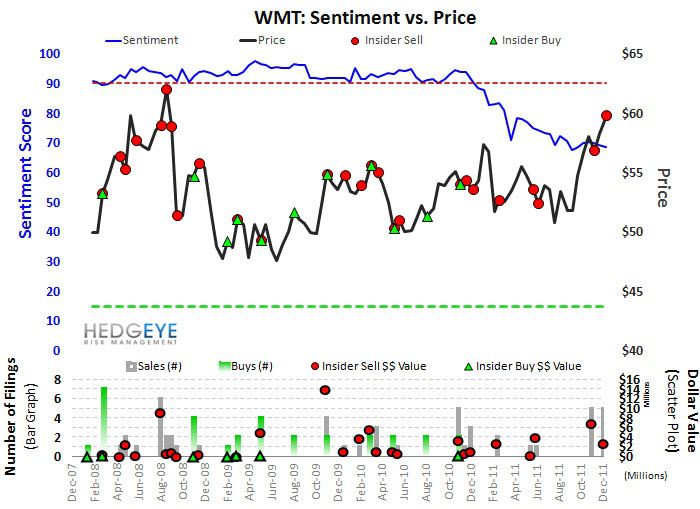

5) Sentiment (per our backtested indicator) has never been worse.