Positions in Europe: Short France (EWQ)

Asset Class Performance:

- Equities: country indices were largely up w/w. Top performers: Ireland 5.1%; Austria 5.0%; Czech Republic 4.9%; Finland 4.8%; Sweden 4.7%. Bottom performers: Ukraine -2.3%; Russia (MICEX) -20bps

- FX: The EUR/USD flat w/w. Divergences: RUB/EUR +2.6%, PLN/EUR +1.3%; CZK/EUR -1.7%

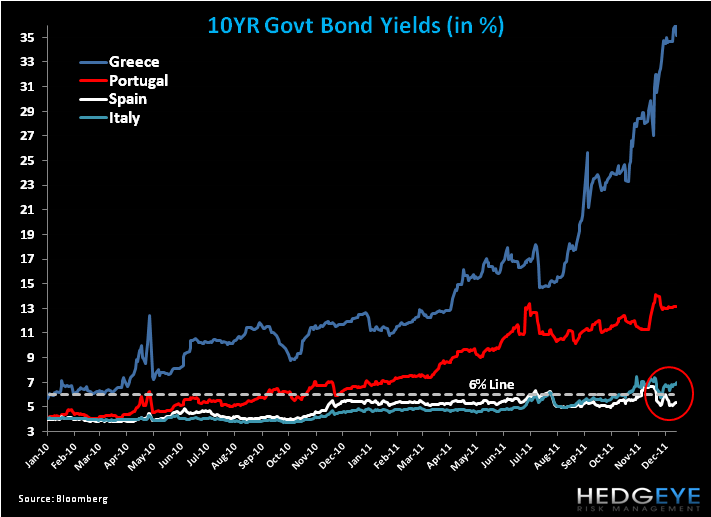

- Fixed Income: 10YR sovereign yields broadly increased w/w, led by Italy +64bps; Greece +48bpsbps; and Spain +26bps. Italy’s 10YR is now up to 6.98%! Last week saw the ECB’s SMP buy 3.36 Billion EUR of secondary sovereign bond issuance, vs two weeks prior of a mere 635MM EUR. We think the continued elevated level of peripheral yields demonstrates that the SMP facility alone cannot arrest yields.

Call Outs:

The European week was dominated by one major theme: the ECB’s LTRO

While on Tuesday European equity markets ripped ahead of Wednesday’s opening of the ECB’s first 3YR Long Term Refinancing Operation (LTRO) facility, with 523 banks taking up €489 billion in loans at 1% (vs initial estimates of €293B from Bloomberg and €310B from Reuters), European equities turned down on Wednesday and sovereign yields actually increased day-over-day, an indication to us that the LTRO will not be the panacea that the market had hope for. What a difference a day makes! (For more see our note on 12/21 titled “Optimism Is Over Ski Tips On LTRO”). Key points include:

- We’d caution against an absolutist view that banks will be buying all European sovereign paper issuance going forward as they’ll stand to benefit from the carry trade, or spread.

- These same banks have taken significant measures to sell their Europig debt holdings in the last 6-12 months. Why would they jump back in now?

- A more likely scenario is one in which banks look to take care of their own houses first before looking to participate in sovereign bond buying.

- In the face of the inability to lever up the EFSF and no change on the ECB’s position to print money, we do think the opening of ECB’s LTRO facility is bullish, yet we don’t think we’re going to cross some magic bridge that will firewall the major issues.

Interest Rate Decisions:

(12/20) Riksbank Interest Rate CUT 25bps to 1.75%

(12/20) Hungary Base Rate HIKE 50bps to 7.00%

(12/21) Czech Republic Repo Rate UNCH at 0.75%

(12/22) Turkey Benchmark Interest Rate UNCH at 5.75%

(12/23) Russia Refinancing Rate CUT 25bps to 8.00%

Chart of the Week:

-Below we show Consumer Confidence from the countries reporting data this week. Of note is that while we are getting some slowing in the declines month-over-month (Germany here shows positive divergence), we’d expect confidence to continue to wane alongside the uncertainty on Eurocrat actions to reduce sovereign and banking risk.

CDS Risk Monitor:

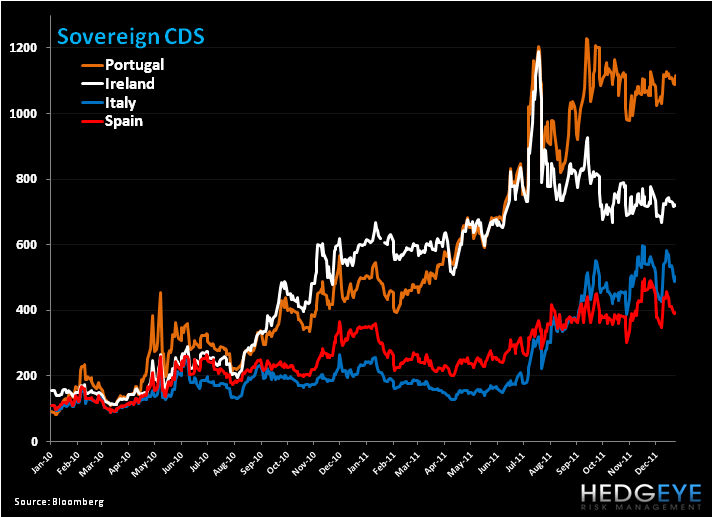

-On a w/w basis, CDS was largely down across the periphery. Italy saw the largest pullback at -32bps, followed by Spain (-18bps) and Ireland (-11bps). On a m/m basis, Spanish CDS is down -95bps and Italian CDS is down -57bps.

EUR-USD

-Our position remains unchanged week-over-week: we’d short the cross at $1.33 for an immediate term TRADE. The EUR/USD remains broken long term TAIL ($1.40) and intermediate term TREND ($1.42) in our models and we think the lack of resolve from the newest proposals for a fiscal union will encourage greater downside.

The European Week Ahead:

Sunday: European Bank capital raising “plans” due for meeting 106 Billion EUR target

Monday: Nov. France Total Jobseekers and Net Change

Tuesday: Dec. Finland and Czech Republic Consumer/Business Confidence

Wednesday: Dec. UK Nationwide House Prices (Dec 28-30th); Q3 Russian Current Account (Dec 28-31st)

Thursday: Nov. Eurozone Money Supply; Dec. German Consumer Price Index – Preliminary; Dec. Italian Consumer Confidence; Q3 Hungarian Current Account; Q3 Ukraine’s GDP – Final

Friday: Nov. German Retail Sales; Q3 BoE Housing Equity Withdrawal; Nov. Italian PPI; Dec. Spain’s Consumer Price Index – Preliminary

Matthew Hedrick

Senior Analyst