Keith just added NKE to the Hedgeye virtual portfolio on red. Both top-line and futures came in better than expected and inventories improved on the margin this quarter driving our incremental bullishness on the immediate-term TRADE and intermediate-term TREND in light of our already bullish long-term TAIL call.

The bottom-line is that sales momentum is strong, margins are on the mend, inventory is coming down, the event schedule looks great, capital intensity is moderating, and Nike is showing greater focus in returning capital to shareholders.

The biggest risk here is the ‘can things really get any better’ factor, but the reality is that we don’t have to worry about that for another year – at least.

Consider the following regarding the current TRADE and TREND setup:

- futures growth of 13% is more heavily weighted towards the back-end of the 5-month window,

- this only partially reflects pricing increases that are in the midst of going into effect. In other words, futures will accelerate simply bc of pricing in 2H (this is one of the very few times in the better part of 15 years that I can recall the company having the confidence to actually guide futures), and

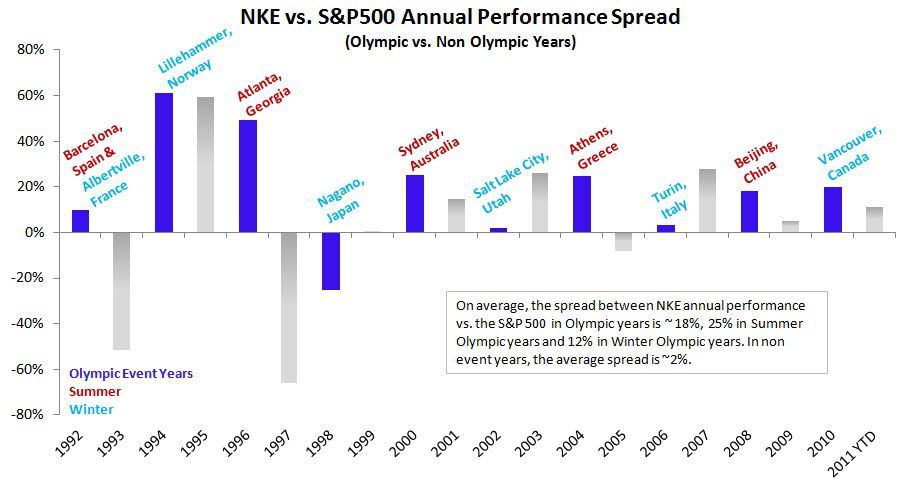

- the company is looking at an outstanding event year, with assumption of the NFL license in April, European Football Championship (Euro 2012) , and the Olympics from July 25 to Aug 12.

- rest assured, as we do, that these events will simply not come and go, leaving Nike with a tough revenue hurdle in 2013. The company will use each of them to build sustainable businesses to take share long after the games are

complete. In fact, Charlie Denson noted several times that there are a few ‘surprises’ coming down the pike later this year. This is the same kind of posturing we saw around major launches like Air 180, Free, Lunar and Nike +. Again, these are platforms, not just products.

We remain 15-20% above consensus for the next three years. For additional detail, see our post Q2 note “NKE: Too Good.”