This note was originally published at 8am on December 19, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Do you like learning? Do you like finding out what’s true?”

-Ray Dalio

Unless you’re long Venezuela or Pakistan (the only 2 markets in the world up double digits YTD), this was not a good year to be long stocks. Most of you know that by now. The final few weeks of 2011 might change the storytelling. Then again, they may not.

What’s True?

During what I thought was the best Global Macro Risk Management interview of the year, that’s what Bridgewater’s Ray Dalio leaned across the table and asked of Charlie Rose.

Can we, as a profession, look into the mirror and answer that question? Or are we failing to learn? Are we accepting mediocrity?

Re-think, Re-work, Re-build.

Rather than give you some completely random wire-to-wire December 31st“Outlook for 2012”, my risk management goals for the coming months, quarters, and years are:

- Don’t lose money

- Embrace Uncertainty

- Be Right

In order to achieve these goals, I have a lot of learning to do. We have an opportunity to learn something from markets every day.

Back to the Global Macro Grind…

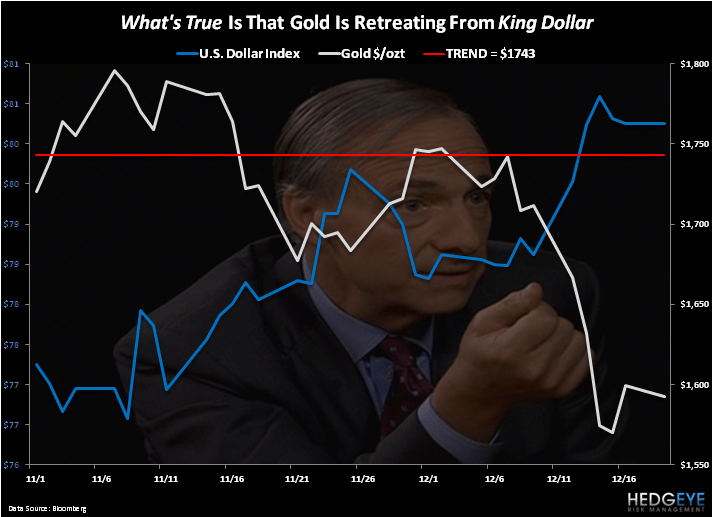

What’s True about Global Equity markets in November and December of 2011 is that they are down. This morning, after seeing Asia make fresh new lows (China and India down -21.0% and -25.2% YTD, respectively), we’re seeing another dead cat bounce from oversold levels in European Equities. Don’t forget that France, Italy, and the UK were down -5.9%-6.3% last week.

Last week’s macro moves were largely explained by our Top 3 Global Macro Themes for Q411:

- King Dollar – up another +2.1% week-over-week

- Correlation Crash – USD up = most things highly correlated (inversely) to the USD down

- Eurocrat Bazooka – no dice

What’s True about the Correlation Crash as it pertains to Commodities is that they went straight down last week:

- CRB Commodities Index = -3.6%

- Oil prices (Brent) = -4.9%

- Gold = -6.9%

- Copper = -6.2%

- Palladium = -8.9%

What’s True about Palladium is that if you dropped it on your head, it would hurt.

But, aside from consensus being paid to call precious metals “currencies” over the course of the last 4 years, What’s True about the causality embedded in that consensus assumption?

In order to attempt to answer to that question, we need to taking a step back, and Embrace The Uncertainty associated with the Ben Bernanke policy to inflate:

“Let us experiment with boldness… even though some of the schemes may turn out to be failures, which is very likely.”

-John Maynard Keynes in the 1920s (Keynes Hayek, page 33)

What’s True about the Keynes model away from what he called it himself? Well, the man did blow up his entire net worth by being long The Inflation Trade (Commodities) in 1928…

P&L doesn’t lie; Keynesian politicians talking about “price stability” do.

Ray Dalio’s thoughts on this generational debate that’s occurring on Old Wall Streets, in our offices, and on the Twitter-sphere is quite simple: “there is not a quality conversation about what is true.”

So either President Obama or the next President of the United States figures this out or there is going to continue to be a social tension amongst The People. Americans may not know the specific how or why, but they do know they are being lied to.

My first solution to this mess is simply to stop what we are doing (stop lying). Dalio’s is to have a conversation about What’s True. Somewhere in between those ideas is a beautiful American bridge that can Re-build what we broke – America’s trust.

Otherwise, as Dalio solemnly reminded Rose in October of 2011, “… the cost of being wrong is a terrible thing.”

My immediate-term support and resistance ranges for Gold, Oil (Brent), and the SP500 are now $1568-1608, $101.98-107.18, and 1207-1226, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer