TODAY’S S&P 500 SET-UP – December 22, 2011

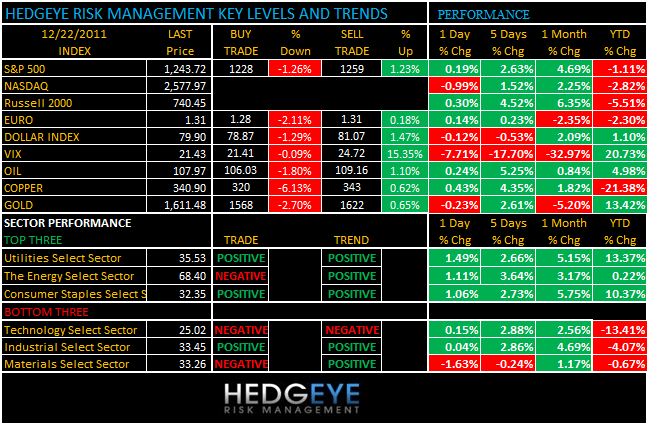

Storytelling may very well make the US stock market world go round, but the globally interconnected facts embedded in last price remain. As we look at today’s set up for the S&P 500, the range is 31 points or -1.26% downside to 1228 and 1.23% upside to 1259.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 695 (-1620)

- VOLUME: NYSE 824.30 (-12.96%)

- VIX: 21.43 -7.71% YTD PERFORMANCE: +20.73%

- SPX PUT/CALL RATIO: 2.53 from 1.25 (+102.78%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – not getting the memo from Ed Hyman on GDP being 4%? in Q4 either; we all know that the Keynesian sell-side GDP models failed Old Wall St in both 2008 and 2011, so I don’t get why someone would use them right here when the long-end of the Treasury market has front-run every Growth Slowdown from Dupont to Oracle this year. 10yr trading 1.96%, only up 11bps on the wk and well below all lines of resistance.

- TED SPREAD: 57.12

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 1.98 from 1.94

- YIELD CURVE: 1.70 from 1.68

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- Japan Gov forecasts FY11-12 real GDP (0.1%), FY12-13 real GDP +2.2%.

- UK final Q3 GDP +0.5% y/y vs consensus +0.5% and prior +0.5%

- UK final Q3 GDP +0.6% q/q vs consensus +0.5% and prior revised to +0.00% from +0.5%

- 8:30am: Chicago Fed, Nov., est. -0.17 (prior -0.13)

- 8:30am: GDP QoQ (Annualized) 3Q, est. 2.0% (prior 2.0%)

- 8:30am: Initial Jobless Claims, Dec. 17, est. 380k (prior 366k)

- 9:45am: Bloomberg Consumer Comfort, Dec. 18, (prior -49.9)

- 9:55am: UMich Confidence, Dec. F, est. 68.0, (prior 67.7)

- 10am: Leading Indicators, Nov., 0.3% (prior 0.9%)

- 10am: House Price Index, Oct. est. 0.2% (prior 0.9%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas storage

WHAT TO WATCH:

- Yahoo! said to consider cutting its 40% stake in Alibaba to ~15%

- Greece creditors said to resist IMF pressure to accept bigger losses on Greek govt bond holdings

- U.K. GDP climbed 0.6% in 3Q, more than estimated

- 10:25am: NRC meets to discuss Toshiba design, permits for what would be first nuclear reactors built in U.S. in 30 years

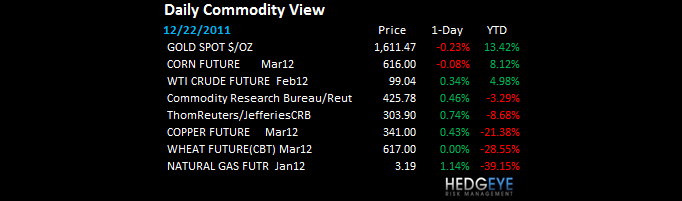

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Herpes Virus Makes Oysters Rare Treat in French Holiday Season

- ‘Medieval’ Economy Is Kim Jong Il’s Legacy as Minerals Untapped

- Hong Kong Solstice Banquets Threatened by Bird Cull, Sales Ban

- Hamburg Loses to Trieste as Southern Ports Exploit Rail: Freight

- Nothing Predicted Happened as Men Conspired With Nature in 2011

- Oil to Set Record in 2012 as U.S. Dodges Slump: Energy Markets

- More Bankers Predict Policy Easing as Economy Cools, PBOC Says

- Gold May Decline in London as ETF Holdings Drop to 1-Month Low

- Oil Rises for Fourth Day as U.S. Supplies Drop Most in a Decade

- Komatsu Sees Record Year for Mining Equipment Sales on China

- Corn Crop Heading for Record to Feed 1 Billion Cows: Commodities

- U.S. Stocks Rise for 2nd Day as Oil Climbs, Treasuries Retreat

- Gloucester Coal Suspends Share Trading Pending Merger Proposal

- Copper Gains for Third Day on Stockpiles, U.S. Data Speculation

- Uralkali Cuts Output Target for Next Year to Buoy Prices

- Ex-Dow Scientist Who Stole Secrets Gets 7 Years, 3 Months Prison

- India Should Allow Banks, Funds Trade in Commodities, Panel Says

- Palm Oil Climbs to Two-Week High as Rains Threaten Production

CURRENCIES

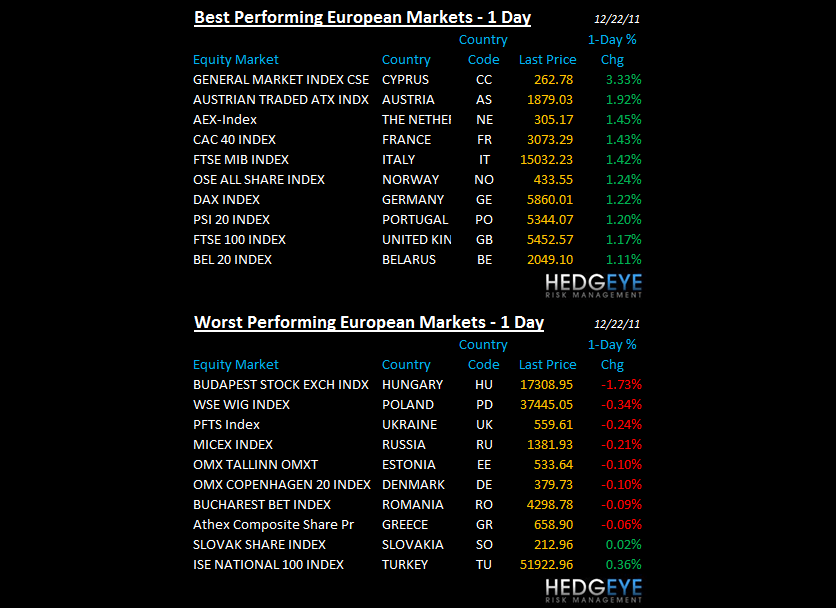

EUROPEAN MARKETS

ITALY – you’d think the Italian stock and bond markets could at least recover my 1st lines of support (immediate-term TRADE lines) and hold them for more than 48 hours – after 24hrs, and 489B euros of life support, nope – MIB’s first TRADE line of resistance = 15,391; watching that like a hawk alongside Euro 1.31 as I have no European short exposure and need to put it back on once resistance is confirmed.

ASIAN MARKETS

ASIA – still not getting the memo that the LTRO gets the world free and clear of the #1 factor that’s pummeling Global Equity valuations in 2011 – Growth Slowing. Yesterday’s export print in Japan (down -4.5%) knocked the Nikkei down another -0.8% overnight (down -18% YTD) and Chinese stocks have been down every day this week. Emerging Markets MSCI Index down -23% YTD – EM outflows $41.2B YTD are = 2nd worst ever.

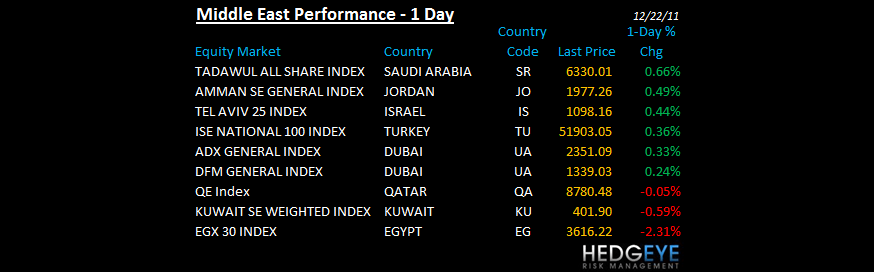

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Baghdad Bombings Kill 57 as Political Tensions Escalate

- Oil to Set Record in 2012 as U.S. Dodges Slump: Energy Markets

- Putin Must Beat Own Economic Record as ‘Golden Decade’ Ends

- EU Banks’ Retreat Creates Gap for Gulf Borrowers: Arab Credit

- Malaysia, Emirates Consider Sukuk for Aircraft: Islamic Finance

- Dana Gas Slumps to Lowest on Record on Egypt Delay Report

- Egypt May Delay $148 Million Payment to Dana Gas, Al Bayan Says

- U.S. Joins EU Push to Embargo Iran Oil Over Nuclear Effort

- Rosneft Overtakes Exxon Mobil in Crude Output, Vedomosti Reports

- BankMuscat Plans Stock Sale at 20% Discount; Shares Advance

- MIDEAST DAYBOOK: Egypt Bond Rating Cut at Moody’s; Barwa Sale

- Dubai’s Nakheel Says It Made 10% Profit Payment on Sukuk

- Qatar’s Barwa Sells Financial District for $3 Billion

- Aldar Won’t Delist Shares From Abu Dhabi, Deputy CEO Says

- Iran to Hold Navy Exercises East of Strait of Hormuz, Fars Says

- U.A.E. Shares Retreat on Aldar Delisting Concern, Margin Calls

- Iraq Halts Oil Exports Via Turkey on ‘Operational Requirements’

- Goldman Sachs Sukuk Row May Dent Industry Lure: Islamic Finance

The Hedgeye Macro Team

Howard Penney

Managing Director