"Alcohol is the anesthesia by which we endure the operation of life."

-George Bernard Shaw

Keith is New York today for meetings and to co-host Squawk on the Street at 10am eastern, so I’ve been handed the keyboard on the Early Look. I actually have the pleasure of writing this missive from my vacation in Mexico (Cancun to be exact), so unlike many of you stock market operators who have had to endure the manic volatility over the last couple of days, I´ve been enjoying the sun, beach, and, dare I say, a few nips of that old magic agave elixir . . . tequila!

To be sure, this has been a year in which the consumption of alcohol has gone up in proximity to many of the world´s financial districts. Although I certainly would not condone overconsumption, to Shaw´s point above, a few drinks does, at times, provide an appropriate release and if there was ever a year in which a suspension of reality was needed, it may be 2011.

Yesterday, the SP500 closed up almost 3% at 1,241. Interestingly, that is about 5 S&P points below the price at which November closed, 1,246. So, despite the massive squeeze the SP500 is still down roughly 40 basis points on the month. So far, at least, Santa Claus has not delivered.

Although the stock market will likely not end the end the year with a meaningful decline, at least not in the U.S., underperformance has been rampant at many mutual funds and hedge funds. To those that have generated positive performance and alpha this year, Hedgeye salutes you as it has not been easy.

Roughly a year ago, Fortune asked us for our perspective on 2011, so I wrote an article on December 31stwhich outlined our key thoughts with the following summary:

“When contemplating the outlook for the upcoming year, the best place to start is consensus expectations. Currently, according to a Bloomberg survey of the strategists from 11 of the largest brokerage firms in the United States, the mean consensus target for the S&P 500 by year end 2011 is roughly 10% above current levels. Further, every single strategist is expecting a positive performance out of the index in 2011.

Suffice it to say, Hedgeye is decidedly non-consensus heading into 2011.

As it stands, we see a trinity of negative fundamental macro clouds on the horizon that have yet to be properly discounted by the market, and which are poised to cast a potentially long shadow over domestic equities heading into next year. The three key risks we see to these lofty consensus expectations heading into 2011 are: global growth slowing, inflation accelerating, and interconnected risk heightening.”

(The article in its entirety can be found here: http://finance.fortune.cnn.com/2010/12/31/a-new-year-brings-new-economic-headwinds/ )

Interestingly, interconnected risk has become the most noteworthy of the three risks we flagged at the end of last year. The most relevant evidence of this is probably a recent statistic emphasized by Jim Grant. According to his analysis, in the entire history of the SP500, going back to 1957, there has never been a day when all 500 stocks rose or fell. There have, though, been 11 days when over 490 stocks moved in the same direction and 6 of those have occurred since July 2011. Still think government intervention has no impact on your portfolios?

At times, our outlook for 2011 looked really wrong. In fact, by April 29th2011 the SP500 was up 8.4% for the year and on track for a 25%+ gain on an annualized basis, which, of course, would have made our outlook not just wrong, but dead wrong. As for those of you who have followed us closely for the past few years, we are anything if not convicted in our research. In 2011, it paid to have conviction on that macro process.

Related to the game in front of us, the short term question is what to do with yesterday's massive squeeze. The key drivers of the squeeze were both a better than expected new housing data point in the U.S. and the newest panacea from Europe (or is it the newest acronym?), the ECB’s LTRO facility. On the first point, housing starts were up 9.3% sequentially to 685K on an annualized basis, but this was driven by a 25% growth in multifamily starts (single family starts have been flat since the expiration of the second tax credit in April 2010 and remain well off prior cycle peaks of 2.27MM on an annualized basis). As it relates to Europe, Italian 10-year yields are up at 6.85% this morning, which suggests we may be shortly awaiting the next European panacea to keep the equity rally going. (Incidentally, Greek 10-year yields are north of 35%.)

Unlike Taiwan equities which posted a 4.56% gain overnight, that market’s biggest gain in 2.5 years, on the back of the government saying it will let its National Stabilization Fund buy equities to support domestic markets, China closed down 1.2% and is now down 22% on the year. The Chinese, it seems, are less excited by the continued path of structurally impaired growth as insinuated by the 498 billion Euros to be lent from the ECB to the European banking system.

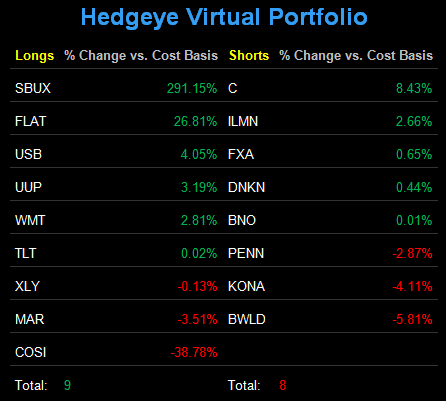

As for our moves yesterday, Keith bought back long term Treasuries (TLT) and shorted oil (BNO) as the SP500 remains Bearish from a TAIL perspective with a range of 1,207 and 1,270. As for me, I’m headed back to the beach to enjoy a few more margaritas before my vacation ends, but rest assured I will be risk managing my consumption. For as Seneca once said:

“Drunkness is nothing but voluntary madness.”

Indeed.

Happy holidays to you and your loved ones,

Daryl G. Jones

Director of Research