If Nike trades down on a sentiment shift, we like it. Numbers are too low. The Street likes it, but for the wrong reasons, and will miss both the depth and duration of this stock move.

We think that we’ll see subtle changes in Nike’s posture towards the Street when it reports its F2Q12 after the bell tomorrow. Though Nike should beat handily (we’re at $1.04E vs the Street at $0.97E) and its backlog should remain in the vicinity of 10%, we think that near-term perception will turn from this being a sheer top line acceleration story, to being one of margin improvement.

The trade-off between top line and margin would ordinarily be a major yellow flag for us – especially given that Nike’s sentiment is the highest out of any name in retail (as outlined in our sentiment indicator below). It’s well loved by the sell-side (14 buys and 0 Sells) and buy-side (1% of the float short) alike. Revenue slowdown into positive sentiment is never a recipe for stocks to go up.

But few people I talk to are playing Nike for a TRADE. I don’t blame them. This is when slicing and dicing a story by duration matters most.

TAIL (3-Years or Less): We think that people like Nike, but for the wrong reasons. They under appreciate the earnings power of the company over the next 2-3 years, as well as the disproportionately smaller capital commitment Nike will need in order to incur in order to grow the P&L. Nike has already invested in the infrastructure needed to more than double the size of its direct business (which is an embarrassingly low sub-15% given that this is one of the most powerful brands in the world), as well as gain share in both Women and Apparel (these two, along with Retail, are not mutually exclusive).

That means more cash, which Nike is using increasingly to return to shareholders where it cannot invest internally or externally at 30% or better. One of the knocks we’ve had with this story has been the widening gap between ROIC and ROE. That’s finally narrowing (and it’s not bc ROIC is falling). Multiply the X axis times the Y axis on the chart below. The product is RNOA. Clearly, when both metrics head to the upper right, there is a dramatic impact on returns.

TREND: (3-Months or More): In looking at our TREND duration, it’s extremely important to keep in mind what’s changed since management updated us on its business 13 weeks ago.

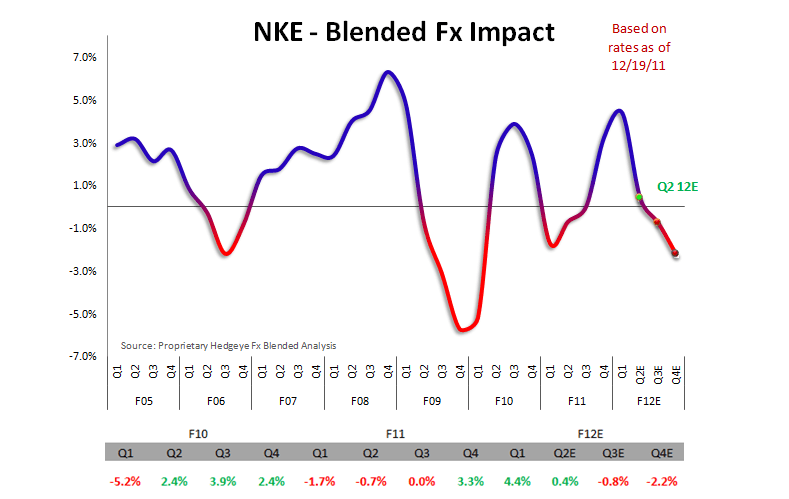

1) FX: to many, it might seems like FX is the biggest factor of change here. But the reality is that it’s not. When Nike last discussed its results in September, the Euro had just crashed by 9% over twenty weeks to $1.35. Then it climbed steadily, only to crash again over the last seven weeks. When all is said and done, FX today is only about 4% off of where it was when Don Blair gave his last update. It is still a tailwind that Nike loses heading into Calendar 2012 and is a concern for us, but not as much as some might initially think.

2) Europe melted down: Nearly every brand selling across Europe is seeing a broad-based slowdown. This is Macro, and it’s big. The behavior of Draghi as new head of the ECB probably trumps any hype around near-term sell-in around the Olympics in London in ’12.

3) China continues to slow. This is no secret. But as recently as last night, Chinese officials made it clear it was willing to let economic activity moderate.

4) Generally Speaking, the sales environment for footwear and athletic apparel in the US is quite good. During the quarter, Foot Locker, Dick’s and Hibbett comped +7.4%, +4.1%, and +7.0% respectively. Inventories remain in check.

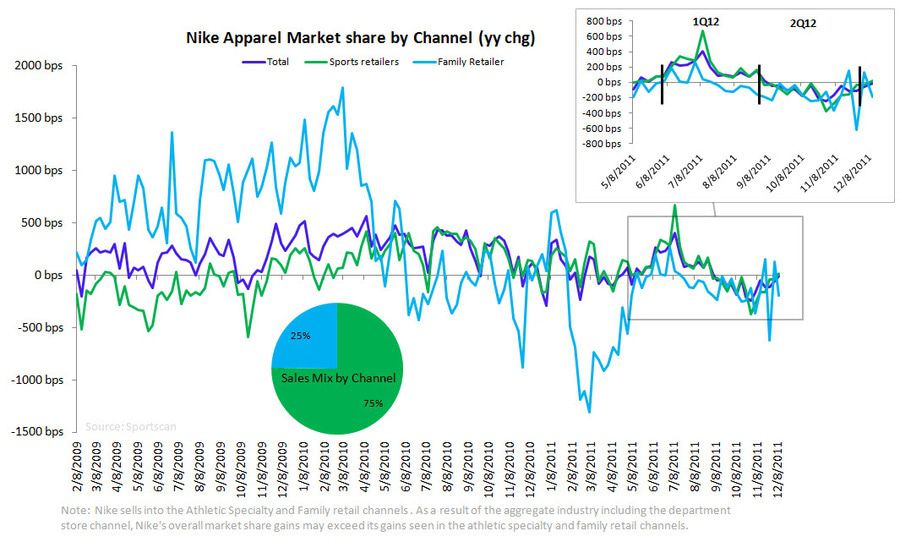

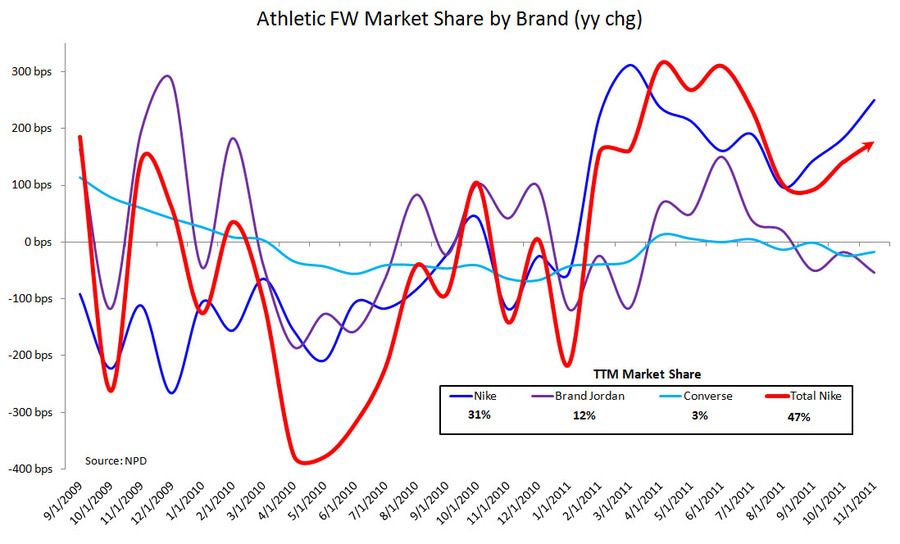

5) Nike market share in footwear continues to dominate as it relates to gains vs. last year. Apparel, on the other hand, still has some of the hottest items in the space (Nike Women’s Tempo Track Short), but has yet to meaningfully close the gap with footwear as it relates to share gain. Keep in mind that this is in the context of a space that is up solid DD so we’re less concerned about market share. But this is a key part of our broader investment theme, and we’re watching it like a hawk to see how it evolves.

It’s nice to see Nike’s US business doing so well. Because as shaky as the US Consumer might be, this is probably the most stable environment as we see it today. On the margin, we’re liking quality brands and franchises that are levered to the US consumer (think Wal-Mart), and less reliant on other economies (P&G). Nike fits somewhere in between. It comes as a surprise to many, but 55% of Nike’s sales originate OUTSIDE the US. And Yes, the vaunted US Footwear business accounts for only 24% of sales.

But when I think about the ‘where could I be wrong’ factor in 2012, it is that the dollar continues to inflate, and takes dollar-denominated commodities with it. Nike has an extremely strong hedging program, and the best relative positioning in the industry. But margins would get hit, and sentiment would get hit harder.

But the bottom line is that – with many of these factors considered -- our estimates are still ahead of the consensus for each of the next 3-years, as outlined by the chart below. That’s tough not to like. Same goes for the return profile.

TRADE: (3-Weeks or Less):

The thing that matters over the super near-term is tomorrow’s print. As noted, it will be a positive headline. But it HAS TO BE a positive headline. Our sentiment indicator below shows how little room there is for error.

Sentiment Index (Part of TRADE framework). This is the product of weighting sell-side vs buy-side sentiment. A sentiment score above 90 (overly bullish) has proven to be a good historical ‘sell’ signal, while a signal below 30 has proven to be better to Buy. Some stocks will never break out of their band, but marginal directional changes matter.

Brian P. McGough

Managing Director