Here is where we stand on the upcoming earnings season for the big cap US listed operators. MPEL looks like the standout.

With two months of detailed Macau data in hand, we feel pretty good about our Macau projections. Las Vegas, as always, is a wild card but aside from MGM, who really cares? Singapore is also more difficult to predict but we are fairly certain MBS will lose some share when the numbers are tallied. We’re still trying to understand the seasonality but it appears that Genting’s leisure exposure should boost its Q4 share vs MBS.

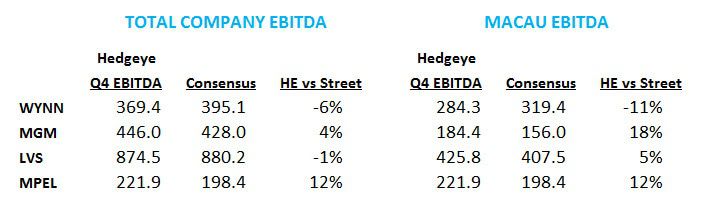

As can be seen in the following table, we are significantly above the Street for MPEL’s EBITDA, and it’s not just hold driven. Hold is trending a little above normal but below last year and below Q3. We think the biggest delta versus consensus is in the Mass segment where MPEL gained significant MoM and YoY share thus far in Q4. MPEL’s Mass margins remain below the US based operators due to player rebates in its significant premium Mass business. However, a mix shift towards Mass still benefits the company’s overall margin. Remember that MPEL’s exposure to the high-end premium Mass allowed it to emerge unscathed from the opening of Galaxy Macau and will certainly help when Sands Cotai Central – another mid-level Mass property – opens next year.

On the downside, our Q4 EBITDA estimate for WYNN is 6% below consensus, concentrated in Macau. Wynn Macau continues to lose share and growth has been a little disappointing. We are fairly in-line with the Street on LVS, although higher on Macau EBITDA due to junket-related share gains and a little below in Singapore due primarily to seasonality. MGM looks like a beat at this stage of the quarter.