TODAY’S S&P 500 SET-UP – December 15, 2011

Global Growth continues to slow and King Dollar reigns. As we look at today’s set up for the S&P 500, the range is 25 points or -0.56% downside to 1205 and 1.50% upside to 1230.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1359 (+18)

- VOLUME: NYSE 926.06 (-0.05%)

- VIX: 26.04 -2.48% YTD PERFORMANCE: +46.70%

- SPX PUT/CALL RATIO: 1.74 from 1.57 (+2.48%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 54.12

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 1.92 from 1.96

- YIELD CURVE: 1.67 from 1.72

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am, Producer Price, M/m, Nov., est. 0.2% (prior -0.3%)

- 8:30am, Current Account, 3Q, est. -$108.4b (prior -$118b)

- 8:30am, Empire Manufacturing, Dec., est. 3 from 0.61

- 8:30am, Initial Jobless Claims, week of Dec. 10, est. 390k, (prior 381k)

- 9am, Net Long-term TIC Flows, Oct., est. $62.5b (prior $68.6b)

- 9:15am, Industrial Production, Nov., est. 0.1% (prior 0.7%)

- 9:15am, Capacity Utilization, Nov., est. 77.8% (prior 77.8%)

- 9:45am, Bloomberg Consumer Comfort, week of Dec. 11 (prior -50.3)

- 10am, Philadelphia Fed., Dec., est. 5 (prior 3.6)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas storage

- 1pm, U.S. to sell $12b 5-yr TIPS (reopening)

- 3:20pm, Fed’s Lockhart to give commencement speech in Atlanta

- Eurozone December preliminary manufacturing PMI +46.9 vs consensus +46.0 prior +46.4

- Germany December preliminary manufacturing PMI +48.1 vs consensus +47.5 prior +47.9

- France December preliminary manufacturing PMI +48.7 vs consensus +47.0 prior +47.3

- Japan Q4 large manufacturer tankan (4) vs cons (2) and 2 seq.

- China HSBC December flash PMI 49.0 vs 47.7 seq.

WHAT TO WATCH:

- NFL to generate ~60% more rev. through 2022 from 9-year contract extensions with CBS, News Corp.’s Fox unit and Comcast’s NB

- 12:15pm: U.S. Transportation Secretary Ray LaHood will make “major announcement” on transportation funding

- 1pm: Jon Corzine returns for third round of testimony before Congress on collapse of MF Global

- 9pm: Republican presidential candidates debate in Iowa

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – get the USD right, you’ll get plenty of other things right; with the USD/Gold inverse correlation (on our immediate-term TRADE duration) going bezerk yesterday (went to -0.93%), KM bought it – long-term TAIL support for Gold = $1568/oz. I’ll keep this on a tight leash w/ immediate-term TRADE resistance = $1624.

- Paulson’s Bright Spot May Fade as Gold Plunges to Five-Month Low

- Victoria’s Secret Revealed in Child Picking Burkina Faso Cotton

- Sino-Forest’s Biggest Holder Asks for Bond Default Rethink

- Gold May Gain in London as Dollar Advance Pauses; Platinum Drops

- Coffee Market Braces for Record Espresso-Bean Jolt: Commodities

- China’s Manufacturing May Contract a Second Month, PMI Shows

- Saudis Triumph as Recession Concern Unifies OPEC: Energy Markets

- Record Big Vessel Deliveries to Hit Asian Lines: Freight

- Oil Rebounds After Biggest Decline Since September Spurs Buying

- ArcelorMittal, Anglo Win Case Overturning Sishen Right Award

- Credit Agricole Says Closing Equity Derivatives and Commodities

- Joy Global Falls on ‘Sluggish’ Near-Term Commodity Demand

- Wheat Gains in Chicago as Egypt’s Purchase May Mean More Demand

- Copper May Decline as China’s Manufacturing Data Dim Outlook

- UBS Lists Top 10 Miners, Commodities; Sees ‘Pain Before Gain’

- Oil Tumbles Most Since September as OPEC Raises Output Ceiling

- Commodities Fall Most in 11 Weeks in ‘Panic Selling’ on Europe

- Indonesian Exchange Delays Physical Tin Contract to January

CURRENCIES

EUROPEAN MARKETS

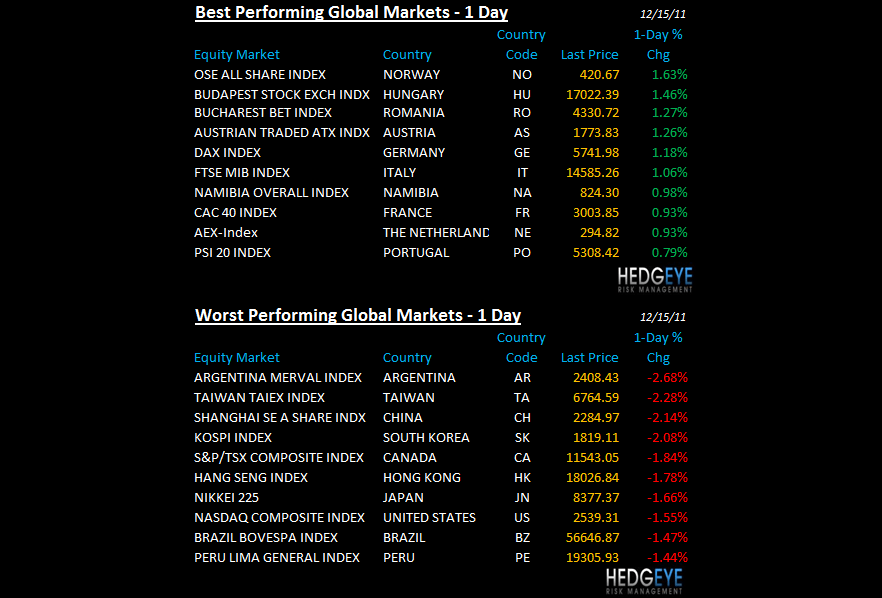

RUSSIA – this story of risk is what Asia’s slowdown was 6-8 weeks ago – not a focus of the financial media, but it will be as the Russian stock market continues to crash (leads European decliners again this morning, down -1.2% and down -36.3% from its Bernanke PetroDollar peak of Qe2 hopes (Q211). Putin not happy.

ASIAN MARKETS

CHINA – new to whoever hasn’t been paying attention; not new to you – China is crashing alongside Commodities – its all part of the same Global Macro trade we call the Correlation Crash. Shanghai Comp down another -2.1% last night (6 straight days) to -22.4% YTD. Getting interesting on the long side as we Deflate the Inflation. Have not pulled the trigger yet.

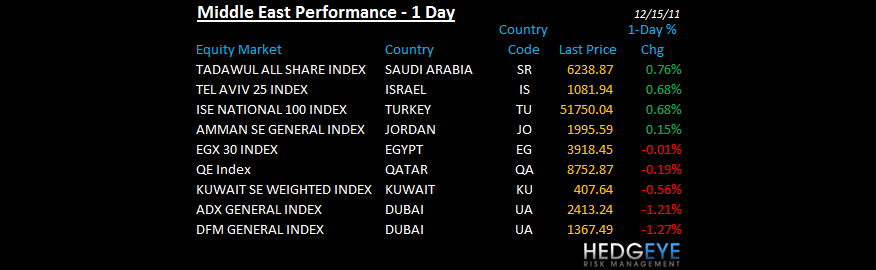

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Saudis Triumph as Recession Concern Unifies OPEC: Energy Markets

- Aldar Converts Mubadala-Held Bonds at Low End of Price Range

- U.A.E., Qatar Fail to Secure Upgrade to Emerging by MSCI

- Dubai Stocks Drop Most in 6 Weeks as MSCI Extends U.A.E. Review

- Iraqis Who Helped U.S. War Effort Must Not Be Left Behind: View

- Saudi Bank Lending Rates Rise After Cabinet Changes: Arab Credit

- OPEC Agrees to Higher Oil Target to Accommodate Libya, Iraq

- PLUS Sukuk May Lure Insurers as Yields Top 5%: Islamic Finance

- Iran Says Saudis Won’t Make Up For Its Oil If Sanctions Tighten

- Iraq Draws U.S. Hotel Operators Banking on Business Travelers

- Casino in Hypermarket Accord With Groupe Al Meera of Qatar

- European Banks Trim Loans to MENA Firms, Standard Chartered Says

- First Gulf Bank Drops Most in Four Months After MSCI Decision

- S&P Applies New Criteria to 25 Gulf Banks and Two Subsidiaries

- Obama Calls End of Iraq War ‘an Extraordinary Achievement’

- U.S. Net Oil Imports to Slump 60% in Nine Years, Citigroup Says

- Six Themes for Oil & Gas Equities in 2012: Citigroup

The Hedgeye Macro Team

Howard Penney

Managing Director