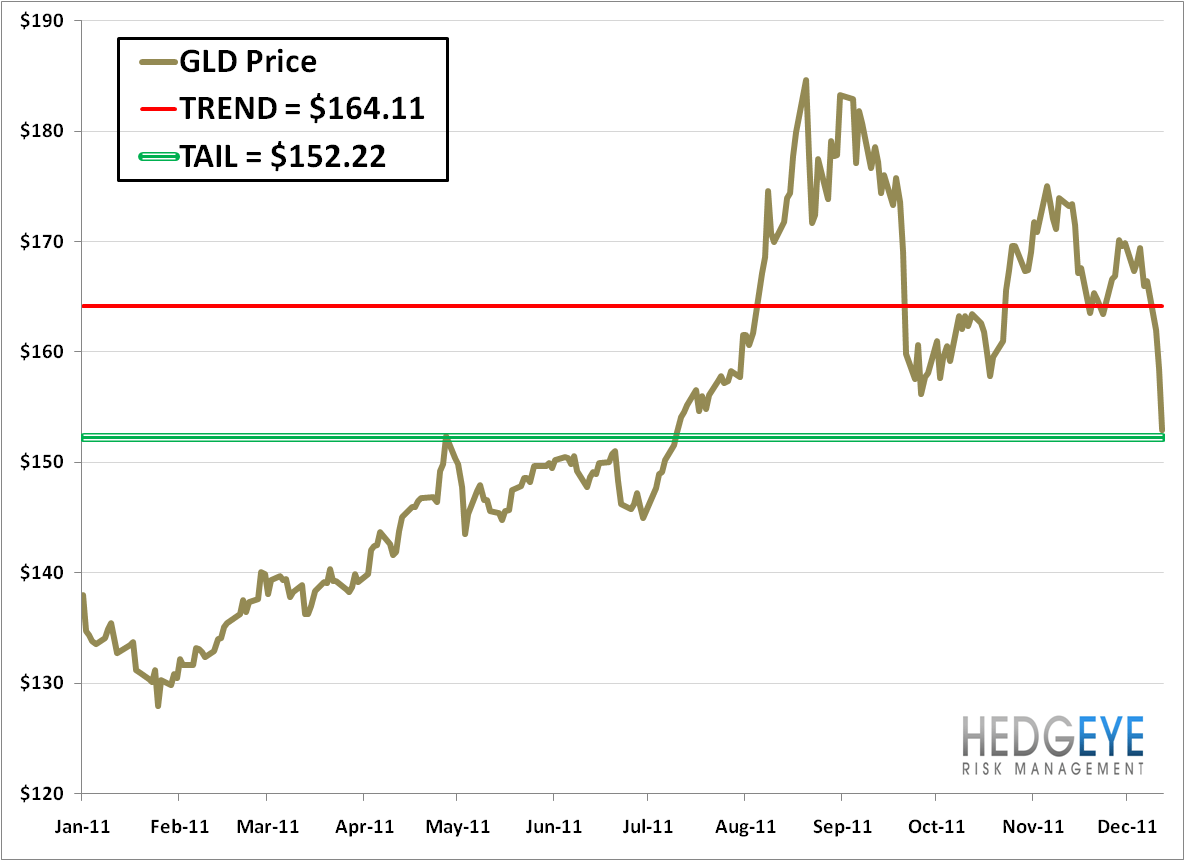

Position: Keith bought GLD for the Hedgeye Virtual Portfolio this afternoon at $152.22.

Gold had its largest one-day drawdown since September amidst a strong dollar and forced selling via margin calls; we took the opportunity to buy the blood, as the precious metal hit our long-term TAIL line of support, $152.22.

Most important, the US Dollar is immediate-term TRADE OVERBOUGHT after busting a 2.5% move higher in the last three sessions; given that the 15-day correlation between gold and the US dollar is -0.94, we believe gold will spring back when the dollar stops going up.

And as an aside, we view owning gold is a call option on government and central bank intervention is asset markets. [Gold rallied 2% on November 30, the day that the world’s major central banks cut and extended swap lines to lower short-term borrowing costs for financial institutions.] While the timing and scope of such an event is impossible to predict, the probability of further action to ease financial stress increases on the margin as asset prices fall.

Our quantitative setup for GLD is: TAIL line support at $152.22 (0.4% downside) and TREND line resistance at $164.11 (7.3% upside).

Kevin Kaiser

Analyst