Commodities are generating a lot of attention in the capital markets at the moment as the dollar gains. Corn and wheat gained on the week even as the dollar strengthened. Chicken wing prices continue to head higher.

STOCK THOUGHTS

Chicken Wings – BWLD

We have been highlighting our short thesis on BWLD for some time. Based on our analysis, we think the stock could go to $45. Chicken Wing prices broke through $1.40 this past week for the first time since 2Q10. Now up almost 20% year-over-year, the increase in wing prices is having an impact on price action in the stock and – we believe – our thesis is gaining credibility as investors realize that a selling food cheaply in an inflationary environment is not a sustainable strategy for restaurant companies. Olive Garden’s recent results proved to be the catalyst for BWLD but we believe that sentiment has further to fall and some difficult quarters, particularly 1Q12, lay ahead.

SUPPLY: Supply continues to contract in the chicken industry. For the week ended December 3, commercial hatcheries represented in the 19 state weekly USDA data saw egg sets decline ~6% on a trailing six-week basis. Production in the industry will continue to contract, year-over-year, for some time as the industry seeks to find its feet after a disastrous year.

DEMAND: As demand from food service companies for chicken strengthens (high beef costs), we expect prices to continue higher.

Below we are including a long term chart of chicken wing prices. The current spike in wing prices may correct at some point, but the overall trend could continue much higher given the right fundamentals.

BEEF – WEN, TXRH, JACK, CMG

Beef prices remain elevated despite the decline over the last week. Much of the recent correction in beef prices, it seems, has been related to concerns around the economic crisis in Europe. For WEN, TXRH, JACK, CMG and others, high beef prices represent a concern for business trends today and in 2012. While some substitution is likely to bolster chicken prices and slow the increase in beef prices, we believe that beef prices are likely to remain elevated for at least the first half of 2012 absent a massive economic slowdown.

SUPPLY: The supply picture is bullish for prices as the number of cattle sent to feedlots for fattening fell for the second consecutive months month during November as corn prices continue to pose a hurdle for processors’ profitability. The impact of the drought in Texas and some surrounding states will also have an impact on supply as farmers try to increase the size of their now-depleted herds.

DEMAND: October was another excellent month for domestic pork and beef exports, according to the USDA. With two months to spare, pork and beef exports for 2011 hit a new record of $4.93 billion and $4.49 billion, respectively. Beef exports are increasing to all regions of the world. Over the longer term, The United Nations’ Food and Agriculture Organization said that it expects global meat consumption to jump almost 73% by 2050 as populations and incomes grow.

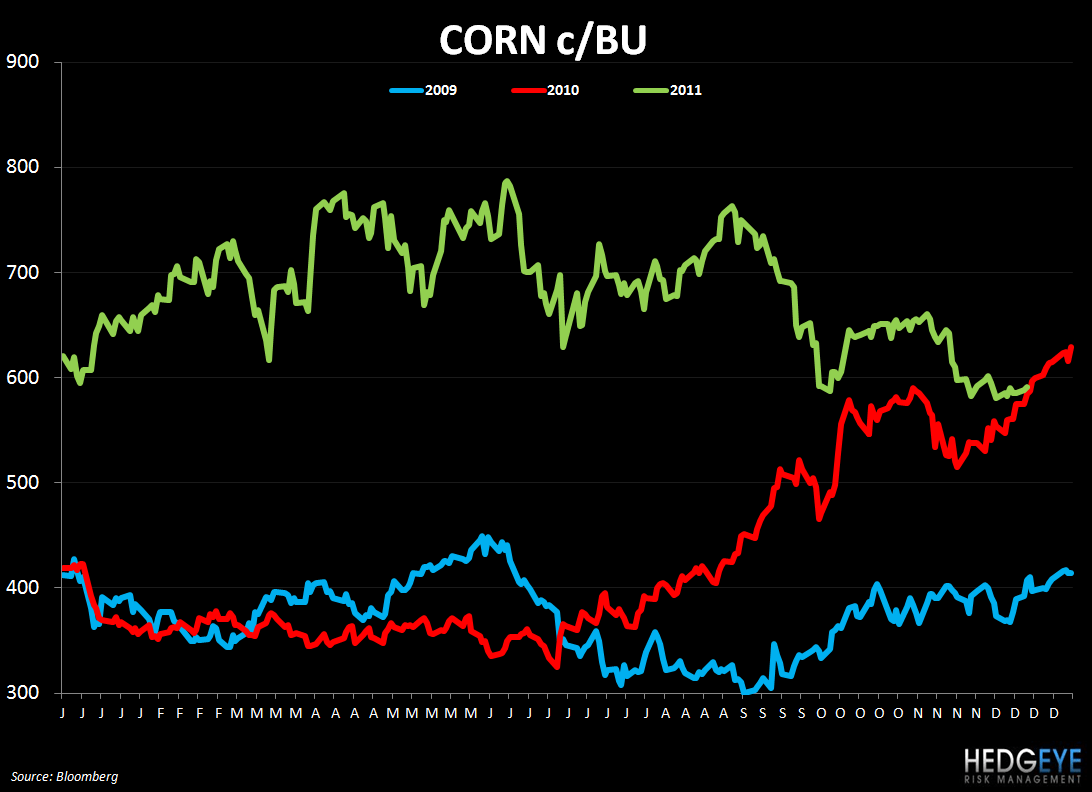

GRAINS

Corn and wheat prices moved lower on the week as concerns around the European crisis persist. For the restaurant industry, and the broader food industry, corn prices are a key factor in driving input costs.

SUPPLY: Last Friday, the USDA World Agriculture Supply and Demand Estimates led grain prices lower on higher global inventories before the 2012 harvest. Wheat stockpiles are expected to rise to the highest level since 2000 before next year’s harvest and China’s corn harvest is also expected to be a record crop.

DEMAND: Slowing exports are persuading some that there is further ground to give up. Corn seems to be the primary target of the grain bears as feed wheat has become far cheaper than feed corn. In October, corn exports decreased 9% versus the year prior. In addition, some analysts are anticipating that hog and chicken producers may use more soybean meal in feed rations due to its relative price versus corn being at its cheapest in more than five years. This strategy’s effectiveness may fade, however, as weather in South America could bring soybean prices higher in 2012.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

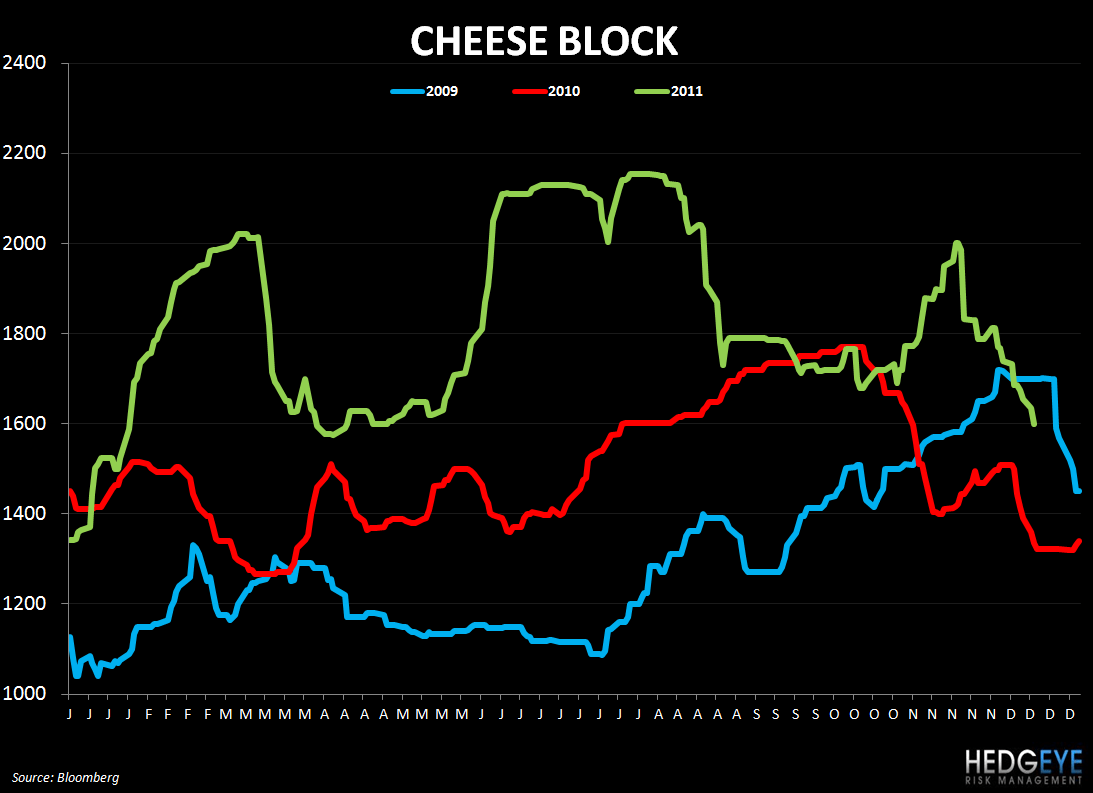

Cheese

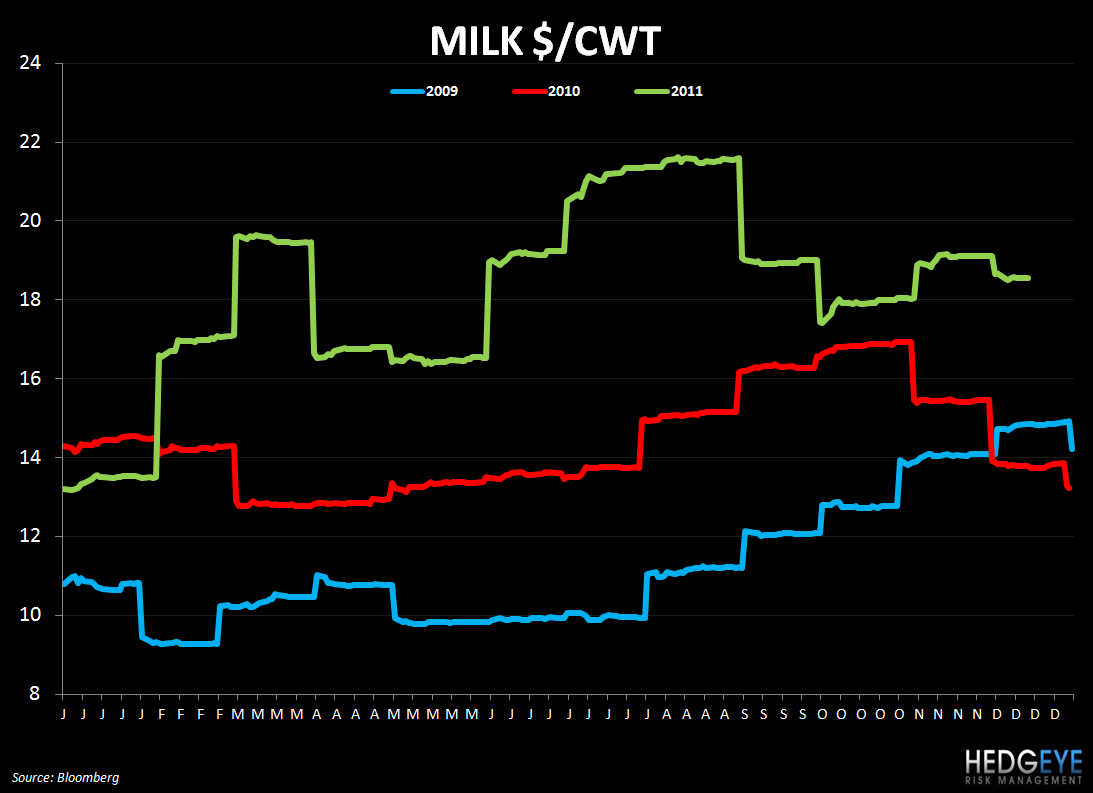

Milk

Howard Penney

Managing Director

Rory Green

Analyst